In Nanshan, the Shenzhen district where Tencent, DJI and other technology giants are headquartered, a growing fleet of driverless robotaxis now run alongside other vehicles. A twenty-minute ride can cost passengers as little as 13 yuan ($1.86).

Inside the robotaxis, the sprightly voice of the virtual driver, Popo, reminds passengers to fasten their seatbelts. The steering wheel turns by itself as the robotaxi cruises through the traffic, stopping at traffic lights and bypassing obstacles and signaling before switching lanes.

The robotaxi is operated by Pony.ai, which is expanding its domain in Shenzhen as well as other cities across China.

Elsewhere in the city, WeRide runs an hourly bus service that takes passengers between the Luohu border crossing with Hong Kong and several tourist attractions for just one yuan. The autonomous bus ride also feels like a journey into the future.

Wide glass panels offer unblocked views of the streets. Passengers can vocally command Xiaoyun, a digital avatar, to adjust the air conditioner. “If the government has approved it, surely its safety is guaranteed,” says a mother who declined to give her name and had brought her 5-year-old daughter along for the ride.

But the safety operator who sits behind the wheel doubts if the autonomous bus can operate commercially in the next five to ten years. In heavy traffic he has to take over. The vehicle also only seats eight passengers but its cost is multiples that of a regular bus.

The standby driver still considers it a worthy investment. The bus service has drawn investors and foreign tourists from all over the world. “The purpose is to showcase Luohu as a tech hub,” he says. “Many visitors are very envious of the technology we have.”

Not every new service has been as smooth. Hello’s robotaxi business had barely got rolling in China when it hit its first pedestrians.

The Shanghai bike-sharing company had veered into autonomous driving only last June, raising 3 billion yuan ($422 million) from batterymaker CATL and Ant Group to build its fleet. At a conference in September, it unveiled a partnership with Alibaba and its first robotaxi model. Hello plans to deploy as many as 50,000 units by 2027.

Passersby help lift a Hello robotaxi off a pedestrian, Zhuzhou, December 6, 2025. Video via social media.

But in early December, just weeks into a trial operation in Zhuzhou, a city in Hunan province, one of its units ran over two pedestrians at a crosswalk. Online footage of the accident shows police officers and several passersby trying to lift the vehicle to free a victim trapped underneath. Both pedestrians were treated in an intensive care unit, a hospital confirmed to local media.

The cause of the accident is still unclear. “The road was wet and slick from cleaning operations and the vehicle couldn’t stop in time,” a person familiar with the matter told The Wire China.

Hello’s hasty rollout is also partly to blame, the person added, saying that the company acquired vehicles from Baidu’s Apollo Go, a leading player in the robotaxi industry but lacks the data, operating experience and supporting infrastructure to ensure the safety of its cars. “It tried to accomplish in months what took others years and that’s very difficult.”

Hello did not respond to requests for comments. The company has not publicly addressed the accident.

The crash is just one among a string of incidents involving Chinese robotaxis in recent years. Last August, a robotaxi operated by Apollo Go drove into a construction pit in Chongqing. The passenger was unharmed. A year before that, another Apollo Go vehicle hit a jaywalker in Wuhan, leaving him with minor injuries.

The latest Hello accident in Zhuzhou is the most serious. It has been compared to an accident in San Francisco in 2023 that eventually led General Motors to pull the plug on its robotaxi project, called Cruise. Chinese authorities have suspended Hello’s operations in Zhuzhou.

The incident highlights the difficult balance China must strike as it seeks to outpace the U.S. in driverless vehicle technology.

China identified autonomous driving in 2015 as one of the key technologies in its Made in China 2025 blueprint. Last year, China was neck-to-neck with the U.S. in deployment of robotaxis, and Chinese players such as WeRide and Pony.ai have emerged as serious contenders to Google’s Waymo and other pioneers. However, the Chinese government must weigh safety, job displacement and a potential backlash as it unleashes a technology whose impact goes well beyond transportation.

“The [Chinese] government is seeking a balance between maintaining people’s livelihoods and encouraging emerging industries and innovation, all while developing a flexible regulatory framework that can ensure the orderly rollout of these vehicles,” says Yang Yongping, an executive director at the Chinese research firm EqualOcean.

“Robotaxis are a good example of how physical AI could improve labor productivity and enhance the overall efficiency of society,” says Paul Gong, head of China Autos Research at UBS. “At the same time, there are also concerns that robotaxis are being deployed too quickly. There might be pushback from the chauffeur community, especially as the mobility industry provides flexible job opportunities.

“The policy,” he adds, “is always swinging between these two two key considerations.”

THE TURNING POINT

Despite the accident in Zhuzhou, last year was a momentous one for robotaxi companies in China. Similar to the U.S., where Waymo is taking off in San Francisco and a handful of other cities, Chinese executives say the industry has reached an inflection point.

Although Waymo still leads in terms of driving performance and design, Pony.ai and WeRide are at “near-parity” in most categories, according to German consultancy P3. Ricco Kampfer, head of P3’s autonomous driving team, says Baidu showed “more variability” in the tests, including more interventions by safety drivers.

Until last year, says Leo Haojun Wang, Pony.ai’s chief financial officer, the industry had been moving “from zero to one,” proving its technology and safety by putting cars on the road and cultivating early adopters. Now, he adds, companies are ready to expand their fleets.

By the end of last year Pony.ai had deployed some 1,160 robotaxis, mainly across Shenzhen, Shanghai and other first-tier Chinese cities. It raised HK$6.7 billion ($860 million) in a secondary listing in Hong Kong in November to bankroll further expansion. Its competitor WeRide — also dual-listed on Nasdaq and Hong Kong’s stock exchange — has a similar number of cars in service and aims to double or triple its global fleet this year.

There is no tolerance for faults because if the system does not work correctly, people may get injured or killed. That’s different from just about every other application of artificial intelligence that people have been working on.

Steven Shladover, a research engineer at the University of California, Berkeley

On an earnings call in November, Baidu chief executive Robin Li said robotaxis are at “a tipping point.” The number of rides the company delivered increased exponentially last year, reaching more than 3 million in the third quarter. It expects the figure to keep soaring as rider interest spreads and more cities loosen regulations.

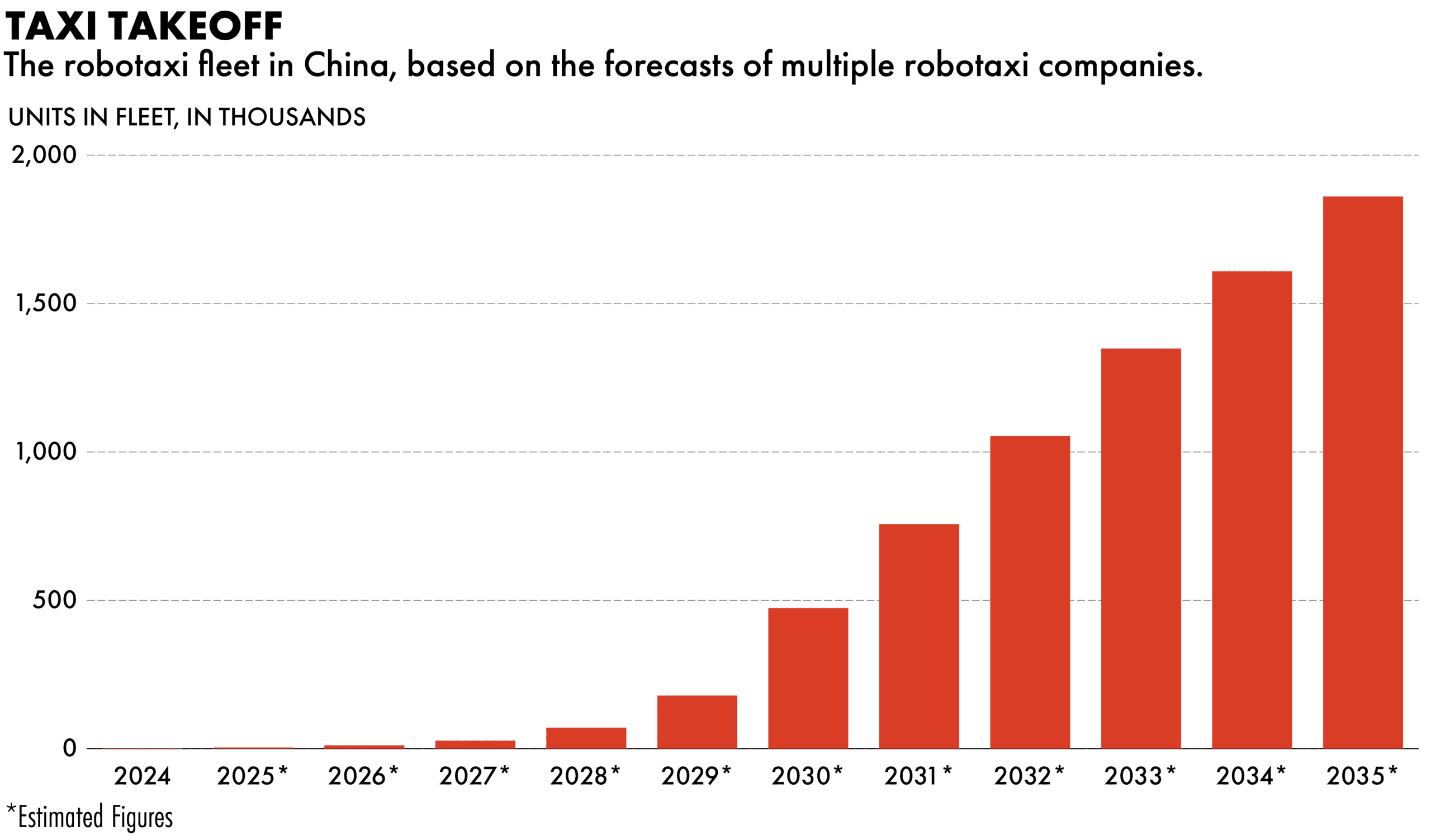

Even with moderate rollouts, Goldman Sachs estimates China’s robotaxi market could be worth $47 billion by 2035, compared to just $54 million this year. Such prospects have drawn new entrants to the industry. Last month EV manufacturer Xpeng announced it is set to begin public road tests of its robotaxis, which are powered by proprietary autonomous driving software and self-developed chips. Huawei has also joined the race, targeting commercial deployment by 2028. Last week, Caocao Chuxing, a top ride-hailing platform backed by carmaker Geely, said it aims to deploy 100,000 robotaxis globally by 2030.

It is not the first time companies have proclaimed the arrival of self-driving cars. But many have underestimated the challenge of creating a system that is more reliable than human drivers. “It’s been a very long and expensive process to get to the point of having a system that can actually drive reasonably safely in public traffic,” says Steven Shladover, a research engineer at the University of California, Berkeley, who has studied autonomous driving for decades.

“There is no tolerance for faults because if the system does not work correctly, people may get injured or killed,” he adds. “That’s different from just about every other application of artificial intelligence that people have been working on.”

Robotaxis operate at level four (L4) autonomy, where the system is fully responsible for navigation within limited areas and a human driver does not have to be present. In some Chinese districts, robotaxis are fully driverless and no longer have safety drivers physically in the car, but they are monitored remotely by personnel who can take over when necessary.

Levels of Vehicle Automation

| Level | Automation Label | Description |

|---|---|---|

| L0 | Momentary Driver Assistance | Driver is fully responsible for driving the vehicle while system provides momentary driving assistance, like warnings and alerts, or emergency safety interventions. |

| L1 | Driver Assistance | Driver is fully responsible for driving the vehicle while system provides continuous assistance with either acceleration/braking OR steering. |

| L2 | Additional Driver Assistance | Driver is fully responsible for driving the vehicle while system provides continuous assistance with both acceleration/braking AND steering. |

| L3 | Conditional Automation | System handles all aspects of driving while driver remains available to take over driving if system can no longer operate. |

| L4 | High Automation | When engaged, system is fully responsible for driving tasks within limited service areas. A human driver is not needed to operate the vehicle. |

| L5 | Full Automation | When engaged, system is fully responsible for driving tasks under all conditions and on all roadways. A human driver is not needed to operate the vehicle. |

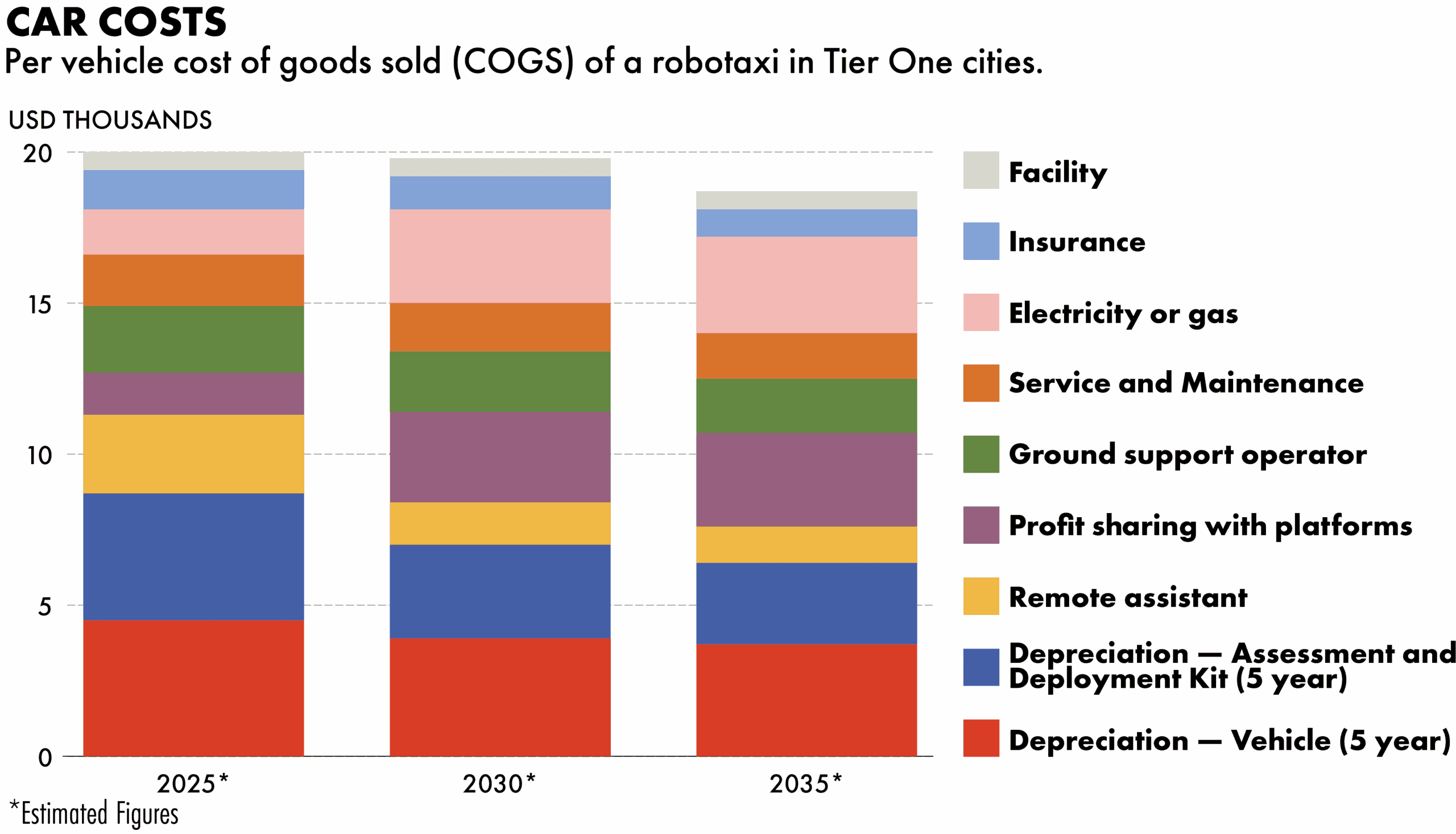

Several factors have enabled the robotaxi industry to hit the gas. For one, hardware costs — including the sensors and cameras that form the autonomous driving kit and the vehicle itself — have been coming down.

“A big obstacle to commercialization in the past was that robotaxis were too expensive,” says Wang at Pony.ai. With previous models costing more than one million yuan each, “the more cars we deployed, the more money we’d lose — as a startup, we couldn’t do that”.

Pony.ai’s seventh-generation robotaxi, launched in November, is 70 percent cheaper than its sixth-generation predecessor. The company says this dramatic cost reduction, along with an increase in daily rides, has enabled it to break even per unit in Guangzhou, meaning a vehicle’s daily revenue is sufficient to cover costs including maintenance, insurance and the salaries of remote safety operators. Wang calls this “a major milestone”.

Advances in artificial intelligence are another important factor. Older autonomous driving technology relies on rule-based systems, where human-coded rules dictate how vehicles behave. But researchers have come to realize that no amount of rules written by humans can cover the infinite number of real-world scenarios on the open road. No matter how much distance and data vehicles have accumulated, they may still encounter so-called “corner cases” — situations that their systems have not been trained to handle.

Generative AI, which learns patterns from existing data and produces original output, has enabled the emergence of smarter systems in recent years that can potentially help the industry address safety and scalability challenges. Some newer AI models, called “end-to-end” systems, are fed massive amounts of data and learn how to navigate even previously unimagined scenarios. “It allows the companies to expand at a faster rate, because they don’t have to write millions of codes again and again,” says Mohit Sharma, an analyst at Counterpoint Technology, a market research firm.

In addition to real-world data, the models can also be trained on “synthetic” data generated by AI, which makes it easier for companies to adapt their software and algorithms to a new region. WeRide, for instance, has a simulation engine that “builds highly realistic virtual cities within minutes”, says founder and chief executive officer Tony Han. “This accelerates iteration cycles, reduces time and cost, and enhances our system’s ability to handle complex situations.”

End-to-end systems have been hailed as a promising solution — and boosted investor sentiment. But they are still in an early phase. Studies have found that they are not yet foolproof.

[Chinese robotaxi players] also compete with an extremely efficient and low cost human ride-hailing and taxi system. That sets a very high bar for pricing, utilization and service reliability.

Poe Zhao, an analyst and author of the newsletter Hello China Tech

“It is now clear what’s the right path,” says Zhang Fan, vice president of AI technology at Nullmax, a company that develops autonomous driving software and is moving into physical AI, the integration of AI in other physical objects. “But from a technological perspective, it will take at least a few more years to reach maturity.”

A Pony.ai autonomous vehicle navigates snowy conditions in Yizhuang, Beijing. Credit: Pony.ai

The industry, Zhang adds, is subject to three constraints: algorithms, computing power and data. All companies are racing to develop better algorithms, but access to the latter two determines the speed of their progress. Acquiring computing power is expensive, especially for startups. And given America’s restrictions on the sale of powerful semiconductors to China, Zhang says “it is difficult to acquire the chips for training models and their prices are soaring”.

The shift to end-to-end systems may accelerate the speed at which car manufacturers and those working on lower levels of automated driving catch up with robotaxis companies. The likes of Tesla, which has millions of cars on the road, can collect data more efficiently. “The OEMs now have an edge in the game compared to the L4 companies,” says Shaoshan Liu, a director at the Shenzhen Institute of Artificial Intelligence and Robotics for Society. “The winner is whoever has the most data.”

NO ROOM FOR ERROR

For now, robotaxis’ biggest rivals are still human drivers; China has nearly 1.4 million cabs (many with more than one driver for different daily shifts) and more than 7 million ride-hailing drivers. Search for a ride in Shenzhen, for instance, and you can easily find over a dozen Uber-like platforms and get matched to a driver in seconds. A 45-minute, 30-kilometer ride can cost as little as 63 yuan ($9). Such a huge number of gig workers have rushed into the sector amid China’s economic downturn that many cities have warned of driver saturation in the ride-hailing industry.

“Unlike Waymo’s context, Chinese robotaxi players do not only compete with each other,” says Poe Zhao, an analyst and author of the newsletter Hello China Tech. “They also compete with an extremely efficient and low cost human ride-hailing and taxi system. That sets a very high bar for pricing, utilization and service reliability.”

The process of ordering a taxi ride with the Apollo Go app. Credit: Apollo Go

Proponents of robotaxis point to China’s shrinking workforce and argue that there will be a labor gap in the long run. By eliminating labor costs, robotaxis will eventually be cheaper than human drivers. Some four million drivers are expected to retire by 2035, Goldman Sachs estimates, and they can be partially replaced by robotaxis.

But until this demographic impact sets in, robotaxi companies must be careful not to threaten employment. Baidu learned this the hard way in 2024 when it priced its rides below those charged by human drivers in Wuhan, sparking a backlash from local cabbies. “Technology is supposed to improve human lives. In reality, it led those in the bottom of society to starve,” a Wuhan taxi company lamented in a public letter. The fallout forced the municipal government to dial back its support, slowing Apollo Go’s city-wide expansion.

“In China, there are two considerations. One is, are you going to take jobs from the drivers? The second is safety,” says Liu. “It’s more complex in China compared to the rest of the world.”

“The transition to autonomous driving will be a gradual and well-regulated process,” an Apollo Go spokesperson told The Wire China. “Our robotaxi fleet currently complements, rather than replaces, existing transport options.” The company adds that it is creating new roles within the industry, such as data annotation and monitoring of the vehicles, and prioritizing drivers for these jobs.

Accidents can also undermine consumer trust in the technology or force local governments to recalibrate.

Companies cite different data points when boasting about their safety records. WeRide reports more than 2,300 days — or about six years — of safe public operations. Pony.ai’s vehicles have traveled 60 million kilometers without a major accident and the company says its insurance fee per vehicle is half that of a typical taxi. At Baidu’s annual tech conference in November, CEO Robin Li said the company had accumulated 240 million kilometers of autonomous driving mileage, enough to “circle the earth 6,000 times”.

Some question if these numbers are sufficient proof of reliability. Shladover, at UC Berkeley, has worked with regulators in California, where a number of Chinese companies have done road tests. He recalls a demonstration ride where, in order to impress investors, a Chinese company directed its vehicle to drive aggressively without leaving much margin for safety. “Data that I’ve seen from their work in California did not inspire confidence about safety,” Shladover says. “It indicated that the companies involved did not really understand the safety implications of what they were doing.

“You’re endangering the general public if you put in systems that have not been really thoroughly tested,” he adds. “And if the companies do not have a proper safety management system… that means the corporate management puts safety at the highest priority, their commitment to safe operations should be questioned.”

Whether the latest accident in Zhuzhou proves to be a crisis just for Hello, or a setback for the wider industry, will be a litmus test for Chinese authorities.

While some cities are competing for symbolic leadership in robotaxis and autonomous driving, after the accident local governments may become more cautious and selective about which companies they partner with. This should benefit leading players with solid track records, says Yang at EqualOcean. Enthusiasm for robotaxis in lower-tier cities, he adds, has cooled as a result of the accident.

“In the near term I expect the push-and-pull between central ambition and local caution to persist,” adds Zhao, the analyst.

These concerns add uncertainty to the industry’s outlook in China. Given the high cost of expansion and research and development, WeRide and Pony.ai each recorded some 1.1 billion yuan ($150 million) in net losses in the first nine months of last year even as their revenues grew. These challenges have also been a drag on their share prices.

With profitability still distant, more robotaxi companies are turning to “asset-light models” to preserve cash. They are also trying to partner with established players that can invest in vehicles and fund expansion, instead of challenging incumbents and triggering price wars they can ill-afford.

You can do development and test pilots in China, but for a scaled operation that actually generates profit, the overseas market is the only way out.

Shaoshan Liu, a director at the Shenzhen Institute of Artificial Intelligence and Robotics for Society

“Traditional taxi companies are desperate to improve their financial conditions and are seeking solutions,” says a veteran consultant, speaking anonymously as he is not authorized to speak to the media. “But they’re cautious on spending. They are interested in this new technology but they will only buy robotaxis if the return on investment is proven.”

A CHINA-U.S. TECHNOLOGY BATTLE IN LONDON

Some see a better business case in regions such as Europe, where demand exceeds supply and fares are higher. “You can do development and test pilots in China, but for a scaled operation that actually generates profit, the overseas market is the only way out,” Liu says, adding that the global market is still pretty much “up for grabs”.

WeRide has taken the lead in going global. It has autonomous driving permits in eight countries including Singapore and France, as well as 200 robotaxis in the Middle East. The company has also recently received permits to begin driverless operations in Dubai and Switzerland.

Pony.ai is prioritizing its home market, where there is the most regulatory clarity. But the company has also set its sights on the Middle East; it has partnered with Qatar’s largest transport provider.

Another battleground is London where Waymo and Baidu, with the help of Lyft and Uber, are both set to operate. It is the first market where an American and a Chinese company, each barred from the other’s home market, will go head-to-head in a test of whose technology is superior. “It will be interesting to see how Chinese and U.S. companies compete on a neutral ground,” Sharma adds.

Chinese companies enjoy cost advantages, adds Gong at UBS, whether it is the hardware or engineering. Taking a cue from its Chinese competitors, Waymo has pivoted from the British luxury brand Jaguar to a Chinese car brand, Zeekr, for its next-generation fleet.

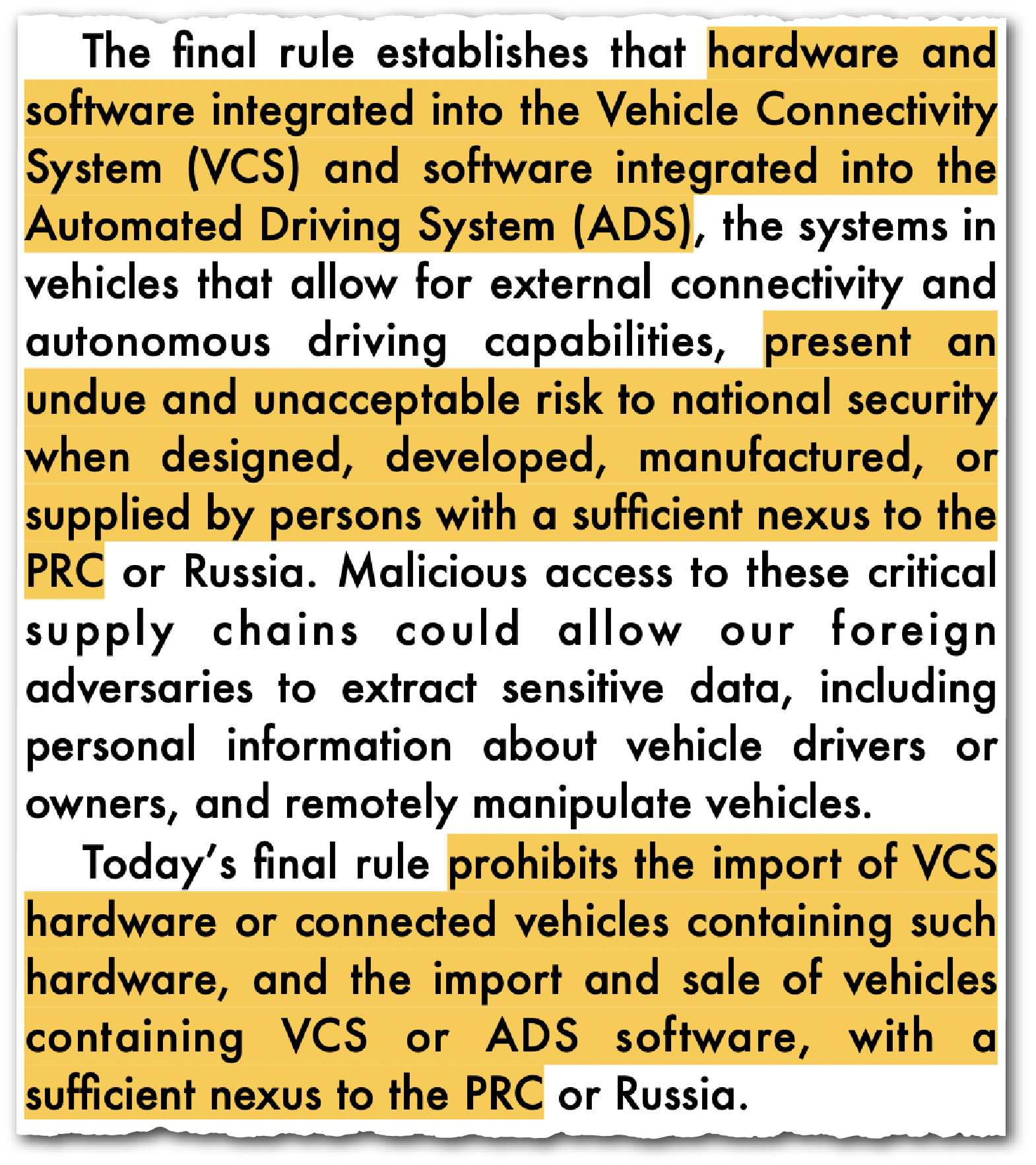

Global expansion will come with its own challenges, however. The U.S., for instance, has banned Chinese autonomous driving software and hardware on the grounds that such vehicles are “computers on wheels” that collect sensitive data, posing a national security risk. Chinese robotaxis companies will probably also face skepticism over their handling of data and compliance with privacy laws.

“Europe is highly heterogeneous, which raises deployment and stakeholder complexity,” says Kampfer at P3. There is a market, albeit smaller than that of China or the U.S., he adds, “but monetization will depend on city approvals, cost per mile and integration economics”.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.