In April 2000, just before the dot com bubble burst on Wall Street, a promising Chinese internet startup called Sina.com made its debut on the Nasdaq Stock Market, raising $68 million in an initial public offering.

The company, which had offices in Beijing and Silicon Valley, seemed primed for success. It had won financial backing from Michael S. Dell and Goldman Sachs; its auditor was PwC; and its founders included graduates of Stanford University’s elite engineering program.

It was not Sina’s strategy, however, that set it apart — since its business model bore a strong resemblance to Yahoo — but its invention of an arcane legal maneuver that over the next two decades would fuel the company’s growth and help fundamentally reshape China, the global financial markets and the secretive world of offshore finance.

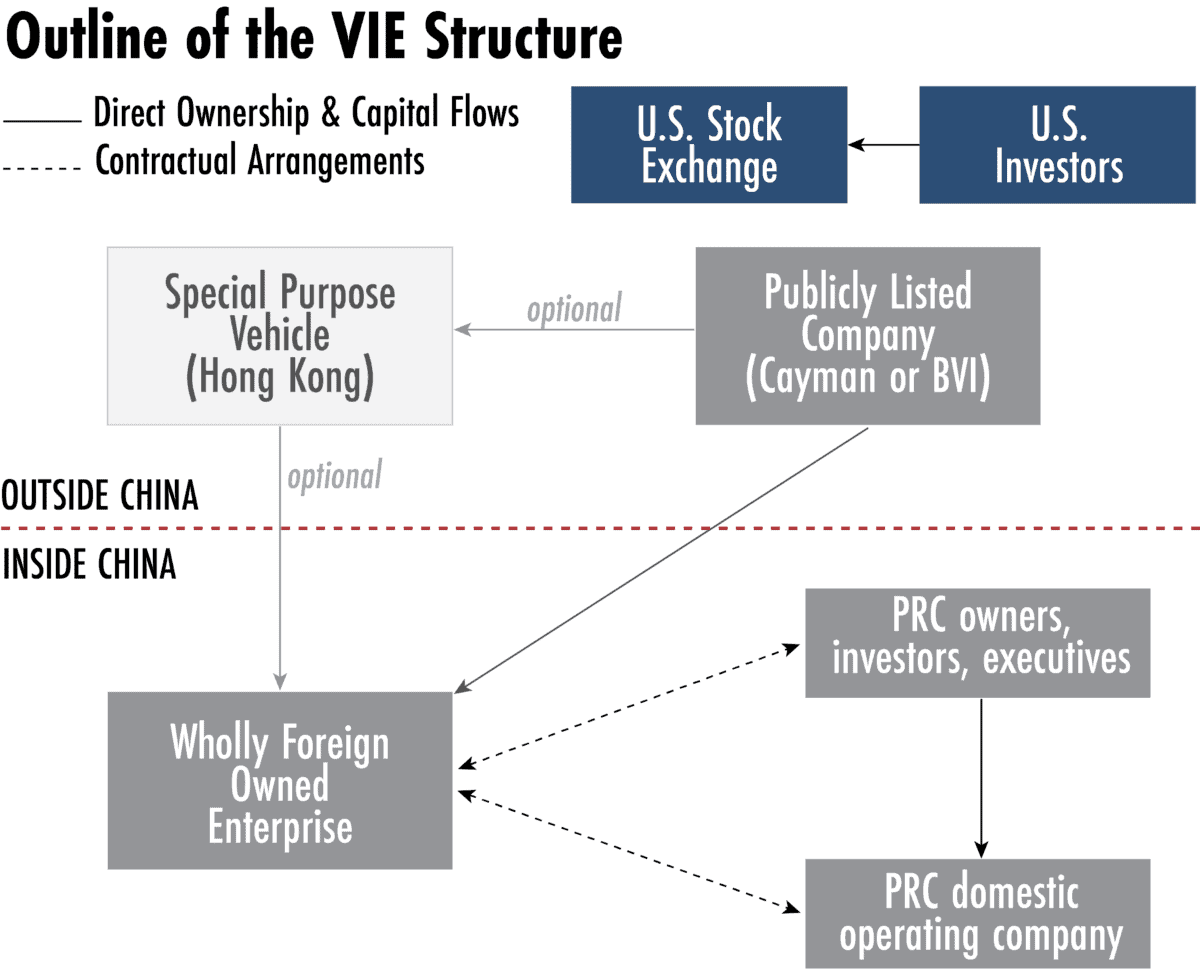

Called the “variable interest entity” — or VIE — Sina’s clever corporate structure allowed the company to get around rules that forbid foreign capital from investing in Chinese internet firms. The process worked like this: Sina set up an offshore company in the Cayman Islands to take in foreign capital, linked it to an onshore company (which held the internet license) headed by a Chinese national, and then had the various firms pledge to consolidate any profits in the offshore entity. This allowed the offshore firm to eventually vie for an overseas listing on the Nasdaq or New York Stock Exchange. It was a brilliant ploy.

“We were trying to balance two competing interests,” recalls Tae Hea Nahm, one of the key legal advisors on the Sina.com deal. “The Chinese government said foreign investors can’t control an internet company because it was a media property. On the other hand, we had investors who wanted to ride the internet boom. So we needed to come up with a structure that kept the Chinese government happy but also allowed the company to list overseas.”

When the authorities failed to intervene in the Sina IPO in the United States, signalling their tacit approval of the structure, other Chinese startups scrambled to adopt the VIE, which paved the way for global investors, led by venture capital firms in Silicon Valley, to pile into China and make huge bets on internet upstarts like Alibaba, Baidu, Tencent and ByteDance — now among the world’s most valuable technology firms.

The “Sina model,” as it came to be known, also triggered a surge in the number of offshore registrations in tax havens like the Cayman Islands and the British Virgin Islands, as budding entrepreneurs in China registered offshore firms in order to chase foreign capital (and know-how) and position their companies to list shares in the United States.

“The historical reasons for that were clear: you couldn’t easily list in China [at that time],” says Gary Rieschel, one of the cofounders of the venture capital firm Qiming Venture Partners. “Sina wasn’t profitable, so they didn’t meet the listing requirements. Before ChiNext [the new startup board] you needed to show three years of profit growth. Tech companies didn’t qualify.”

And yet, even while Chinese firms have used the Sina model to build companies now valued at more than $2 trillion, there is a simmering dispute between Beijing and Washington that underscores the legal and political issues left unclear by the VIE model. Namely, who really controls these companies and what accounting standards should be applied and enforced on them?

In recent months, the U.S. Securities & Exchange Commission has warned investors of the risks associated with Chinese firms listed on America’s stock exchanges, while Beijing has made its own moves, suggesting that it could go further and restrict Chinese firms from listing on U.S. exchanges. Chinese entrepreneurs, it appears, may soon have to reckon with new regulatory regimes, both at home and abroad.

“The VIE structure was always speculative,” says Fraser Howie, a Singapore-based investment banker and the co-author of Privatizing China: Inside China’s Stock Markets. “But now you can’t just accept all the assurances that everything will be OK.”

How China’s offshore companies are registered, and what purpose they serve, has long been misunderstood by analysts and economists. But documents in the Pandora Papers, the offshore documents that were released this weekend by the International Consortium of Investigative Journalists and shared with The Wire, help shed light on the evolution of the VIE structure, the emergence of China as the most prolific creator of offshore firms, and perhaps most importantly, how the Chinese Communist Party came to rely on them.

While global elites tap offshore financial centers to dodge taxes, hide profits and move illicit funds around the world, China is playing an increasingly significant role in offshore finance because of an altogether different aim: to circumvent the Communist Party’s harsh regulatory regime, which is chock full of restrictions on trade, cross-border capital flows and foreign investment in its domestic market; rules that often seem at odds with its globalization drive.

Much of it comes down to a simple fact: Getting money in and out of China’s fast growing economy is a problem. In the Pandora Papers, which contain more than 10 million documents, including emails and corporate registration filings from Belize, Cyprus, Hong Kong, and the Cayman Islands, there are not just clues about how wealthy individuals use secretive offshore finance to hide assets, there’s a great deal about how China has embraced offshore finance in order to adopt legal and governance structures outside of China’s rules — thereby giving Chinese firms a way to better connect with the global financial markets.

Records reviewed by The Wire show that Alibaba’s top executives setup scores of offshore entities to be deployed for takeovers and financing purposes; that state-backed Tsinghua Tongfang set up an offshore firm to co-invest in a digital TV platform. There are also details about how Rio Tinto continued to trade with the Chinese billionaire Du Shuanghua, even after he admitted to paying bribes, and how a Chinese national who gave advice to the founder of Meituan was rewarded in the British Virgin Islands with $56 million worth of Meituan shares, parked in an offshore trust. The deals share one common feature: they each have roots in the Sina model, which allows Chinese nationals to raise foreign capital and to, at some stage, stash large sums of money offshore, beyond the reach of Beijing.

Why would Beijing allow this? Perhaps because it’s not just private firms benefiting from the VIE structure and registering offshore investment vehicles. State-owned companies and investment firms have also moved aggressively to register in offshore locales as they go abroad to hunt for natural resources and advanced technology.

The oil giant Sinopec and the conglomerate CITIC have registered or invested in scores of companies in Bermuda, the Cayman Islands and even Cyprus. Hong Kong — still technically an offshore destination for China — has long served as a launching pad for state firms to borrow in dollars or finance overseas acquisitions. And the Belt and Road Initiative has fired up Chinese firms to “go global” and pile into offshore financial centers to build the world’s roads, bridges and tunnels.

Economists are now trying to make sense of China’s role in offshore finance. Matteo Maggiori, an authority on offshore finance and a professor at the Stanford Graduate School of Business, says Chinese firms domiciled in offshore financial centers now account for a large share of global securities sold in the West, and the use of VIEs and offshore holdings has created a new set of risks for global investors and regulators.

“If you ask a professional economist about offshore tax havens, they’ll say something about inequality. Rarely will they mention China,” Maggiori says. “But in the securities market, China now plays an enormous role. And many of those securities are registered in tax havens —so there’s risks behind that.”

THE OFFSHORE STATE

The secret deal was brokered in 2015, and it involved access to military technology.

Vyacheslav Boguslayev, the chairman of Motor Sich, Ukraine’s leading aircraft engine and defense contractor, had agreed to sell a large stake in his company to a group of state-backed entrepreneurs from China, according to records disclosed in the Pandora Papers.

At the time of the deal, Motor Sich was under financial duress. After Russia invaded Ukraine in 2014 and annexed Crimea, Kiev cut off exports to Russia of Motor Sich fighter jet engines and attack helicopters. Sales plummeted.

That prompted China to step in with the promise of new financing. After all, Motor Sich was also a supplier for China’s People’s Liberation Army, or PLA.

Although the financing came from a group of Chinese businessmen — led by the billionaire Wang Jing — the group’s financial backing was provided by China’s largest policy bank, the China Development Bank (CDB).

The Chinese investors set up a series of offshore firms, including British Virgin Islands-registered Skyrizon Aircraft, to acquire a major stake in Motor Sich, initially for $500 million. The investors then pledged their shares to CDB in exchange for a loan.

Although Kiev eventually blocked the deal on national security grounds — and the U.S. named Skyrizon as a Chinese military end user — the paper trail in the case provides a window into how China’s state-run firms have emerged as power players in the world’s leading offshore financial centers.

Whereas private entrepreneurs in China set up offshore firms to raise foreign capital, using the VIE structure pioneered by Sina.com, Chinese state-owned enterprises typically register offshore affiliates to acquire overseas assets, including energy and natural resources.

Beijing’s growing presence in the offshore financial centers, analysts say, coincides with its drive to acquire advanced, dual-use technologies, a push that has raised alarm in the U.S. and much of the developed world. As tougher national security reviews in the U.S. and Europe have erected barriers to China’s overseas investments, offshore shell companies have offered a convenient workaround, a means to perhaps disguise the role of the state, as in the Motor Sich case.

“It’s a problem if we find out that the Chinese are doing that,” says William Reinsch, a former Commerce Department official now a senior adviser at the Center for Strategic and International Studies in Washington, referring to the possibility that offshore registrations may mask Beijing’s efforts to acquire dual-use technologies. “It’s clearly a due diligence issue. Can the [U.S.] government do enough to understand who the ultimate beneficial owner is? That’s the challenge.”

And even when China’s state firms are not trying to disguise their activities, analysts say they have no choice but to embrace the move offshore. For much of the past two decades, just as Beijing was pushing state firms to “go global” and advance the national interests, the global financial system was rallying around offshore financial centers.

“Thousands of Chinese companies are registered offshore, including [affiliates of] state-owned companies,” says Rasheed Griffith, an expert in offshore finance and a fellow at the Mercatus Center at George Mason University. “Because of China’s currency controls, even SOEs [state-owned enterprises] have difficulty getting money in and out of China. So they set up offshore companies to do acquisitions.”

There is no reliable data on how many Chinese state-run firms have set up affiliates in offshore tax havens but documents available in the Pandora Papers offer clues about the scale of the shift in recent years. The records, for instance, detail the oil giant China National Petroleum Corp’s 2018 efforts to set up a BVI company to acquire an oil field in Syria; and how Citic Capital — an arm of the giant, state conglomerate Citic Group — stocked its investment portfolio with offshore firms with names like “Charm Spring Limited” and “Magic Ocean.”

One set of documents show that in 2017, when Citic Capital engaged Hong Kong-based Asiaciti Trust Asia Limited to form an offshore trust for the benefit of its top executives, Citic Capital provided a detailed group chart. The organizational chart showed that about 160 companies — more than half of all its affiliates — were domiciled in either the Cayman Islands or the British Virgin Islands.

In fact, China’s state-backed investment and asset management firms have emerged as seasoned offshore deal-makers. Some years ago, for instance, when the oil giant Sinopec agreed to spinoff its marketing division, Beijing approved a stake sale to a group of domestic and foreign investors. The investors included state firms like the investment bank C.I.C.C., Cinda and the State-owned Assets Supervision and Administration Commission. Each state firm had acquired shares using affiliates registered in the Cayman Islands or British Virgin Islands.

State money was dressed up as foreign funds, entering China.

And so while Beijing has not officially blessed the VIE structure, China’s state-owned firms have embraced the companies that use — and prosper — from it. In 2012, for instance, Alibaba approved a deal to buy back shares it had previously sold to Yahoo. By then, the Alibaba Group was registered offshore, with a VIE structure, in the Cayman Islands. And like Sina.com, it was eyeing a public listing on the New York Stock Exchange.

But to pay for the Yahoo buyback, Alibaba’s Cayman Islands firm needed financing. And in June 2012, it turned to, among others, China’s state policy bank, CDB — just as Skyrizon had done.

THE LOOMING RISKS

The spectacular growth of offshore finance has clearly altered China’s business landscape, fueling the country’s tech startups and empowering Wall Street and Silicon Valley.

But analysts say there are significant speed bumps ahead because of China’s role in offshore finance. The VIE structure, for one, is now in doubt. Some economists argue that the surge in registrations in offshore tax havens may not just deprive nations of tax revenue and contribute to inequality, but also make it difficult to know the risks behind deals in one of the most opaque corners of the world.

And by emerging as an offshore power, China is now forcing economists to rethink and recalculate its global influence. A recent academic paper, for instance, pointed out that while China held about $1.1 trillion in U.S. Treasury bonds in 2017, a measure of its influence on U.S. interest rates, American investors may hold nearly $700 billion in Chinese equities listed on U.S. exchanges — far more than analysts have previously understood.

The reason? A large portion of those American holdings were pegged to publicly traded Chinese companies that were registered in offshore destinations, such as the Cayman Islands and the British Virgin Islands. And so while it may have been obvious that Alibaba operates in China, the company’s official registration is the Cayman Islands. Chinese stocks, in other words, are now a huge factor in global markets.

“What’s unique about China is the incredible size and scale of the problem,” Stanford’s Maggiori says, noting the influence of VIE-listed Chinese shares. “The offshore aspect creates a layer of complexity because it’s unclear what is under Chinese law. For global investors, that means more of your money is in uncharted waters.”

Maggiori and other economists argue that the massive amount of money flowing into offshore finance can even complicate a nation’s economic policy since countries track their assets and liabilities and adjust interest rates and other policies based on knowledge of cross-border positions, in stocks, bonds and other financial products. If policy makers get distorted figures about foreign direct investment, for example, the policy decisions they make could be flawed.

The offshore aspect creates a layer of complexity because it’s unclear what is under Chinese law. For global investors, that means more of your money is in uncharted waters.

Matteo Maggiori, professor of finance at the Stanford Graduate School of Business

There’s also the potential risks to global investors who buy shares in companies registered in offshore jurisdictions. And a great deal of that risk connects back to the VIE, which analysts say is really an untested structure, built on a fragile foundation, with seemingly tacit approval from Beijing. It can easily be dismantled, or ruled illegal, by bureaucrats working for the country’s powerful leader, Xi Jinping, who has been waging a fierce campaign aimed at cracking down on some of China’s biggest technology firms — many of which are VIEs.1See this 2017 study: Buyer Beware: Chinese Companies and the VIE Structure, by the Council of Institutional Investors.

“A lot of these holdings are through mutual funds or pension funds,” Maggiori says, “and I find it highly unlikely that those types of investors would understand the risks associated with the offshore structures.”

The U.S. Securities & Exchange Commission though has begun to put investors on notice. During the Trump administration, the SEC and the Public Company Accounting Oversight Board (PCAOB) began pushing for greater investor awareness of overseas Chinese listings after the collapse, after an accounting fraud, of Luckin Coffee, which traded on the New York Stock Exchange. And in Congress, there have been calls to delist Chinese firms from American stock exchanges unless they agree to comply with U.S. accounting standards.

In late July, Gary Gensler, chairman of the SEC went public with a video and statement warning investors about the risks associated with overseas companies listed in the U.S., particularly those using the VIE structure. “For U.S. investors, this [VIE] arrangement creates “exposure” to the China-based operating company, though only through a series of service contracts and other contracts,” he wrote. “To be clear, though, neither the investors in the shell company’s stock, nor the offshore shell company itself, has stock ownership in the China-based operating company. I worry that average investors may not realize that they hold stock in a shell company rather than a China-based operating company.”

Gary Gensler, chair of the U.S. Securities and Exchange Commission, explaining VIEs in a video from August 2021. That month, Gensler directed staff to “take a pause” from listing shell companies of China-based operating companies on U.S. Credit: SEC

The VIE, of course, came of age in a different era. In the mid to late 1990s, even Chinese state-owned enterprises, like China Unicom — a telecommunications firm — were searching for ways to bring in foreign capital in a restricted sector, telecommunications. At one point, China Unicom had what appeared to be a VIE-like structure that secured investments from foreign investors such as AT&T and France Telecom.

The deal makers came up with a term for the structure, “China, China, Foreign,” which meant that, like the VIE, there was a path to both comply with Chinese law and raise foreign capital, even in a prohibited sector.2The China, China, Foreign structure, like the VIE, registered an onshore (China) company, linked to another onshore (China) company, and then to an offshore (Foreign) company.

“I worked on the deal to bring in the foreign telecoms,” says one lawyer familiar with the deal. “Just as with VIEs, everyone said, ‘Maybe it’s illegal but it’s the only way we can get foreign capital.’”

Lawyers warned about the risks of the deal, which eventually collapsed, forcing foreign telecom firms out of China Unicom, but soon after came the Sina model, a way for Chinese startups that could not easily raise money from state banks. They turned, instead, to global investors, including some of Silicon Valley’s leading venture capital firms.

“With internet firms, it became the structure dejure,” says one lawyer familiar with the deal. “But I told people, ‘This is like riding your bicycle along the edge of a cliff. But if that’s what you’d like to do, go ahead.’”

What brought the VIE to fruition was collaboration between Chinese entrepreneurs and American investors. Sina, after all, was founded as Sinanet by a group of Stanford University engineering graduates who were trying to create a website targeting the Chinese speaking world, from Silicon Valley. And after being blocked in China, for releasing banned news, it made a deal to merge with a Chinese startup — Stone Rich Sight — headed by the entrepreneur Wang Zhidong.

That 1998 merger, backed by American investors, led to a fevered push to combine the two firms, with one office based in Beijing and the other in Sunnyvale, California, in order to target the market in mainland China and join the rush of dot com IPOs.

“We were always thinking about going public,” says one of Sina’s top executives at the time. “But in Beijing, we realized there were a lot of political restrictions, particularly on the media business. So we started throwing out some ideas.”

Western and Chinese lawyers working for Sina came up with their own version of the “China, China, Foreign” structure — which they named the VIE, or “variable interest entity,” a term widely adopted after Enron failed to consolidate the earnings of its special purpose vehicles onto the books. The VIE structure would not just help Chinese startups raise foreign capital, it might also be acceptable to U.S. regulators as a way to claim the offshore vehicle had some control over those profits and therefore could list on an American exchange.

| Ticket | Company | Sector | Incorporation | IPO Year | Exchange |

|---|---|---|---|---|---|

| BSPM | Biostar Pharmaceuticals, Inc. | Health Care | Maryland | 2000 | NASDAQ |

| NTES | NetEase, Inc. | Miscellaneous | Cayman Islands | 2000 | NASDAQ |

| SINA | Sina Corporation | Technology | Cayman Islands | 2000 | NASDAQ |

| SOHU | Sohu.com Inc. | Technology | Delaware | 2000 | NASDAQ |

| UTSI | UT Starcom Holdings Corp | Consumer Durables | Cayman Islands | 2000 | NASDAQ |

| ONP | Orient Paper, Inc. | Consumer Durables | Nevada | 2002 | NYSE |

| CTRP | Ctrip.com International, Ltd. | Miscellaneous | Cayman Islands | 2003 | NASDAQ |

| JOBS | 51job, Inc. | Technology | Cayman Islands | 2004 | NASDAQ |

| JRJC | China Finance Online Co. Limited | Finance | Hong Kong | 2004 | NASDAQ |

| SEED | Origin Agritech Limited | Consumer Non-Durables | British Virgin Islands | 2004 | NASDAQ |

| NCTY | The9 Limited | Miscellaneous | Cayman Islands | 2004 | NASDAQ |

| BIDU | Baidu, Inc. | Technology | Cayman Islands | 2005 | NASDAQ |

| CNTF | China TechFaith Wireless Communication Tech Ltd. | Technology | Cayman Islands | 2005 | NASDAQ |

| HOLI | Hollysys Automation Technologies, Ltd. | Energy | British Virgin Islands | 2005 | NASDAQ |

Tae Hea Nahm, who served as a legal advisor to sina.com ahead of its Nasdaq IPO, says Sina’s lawyers consulted with both U.S. and Chinese regulators and while neither regulatory body came out publicly in favor of the Sina structure, both sides agreed to allow the listing and the structure of what is now known as the VIE.

“This combined the Silicon Valley model — VCs, IPOs and attracting money and talent — with the Chinese government’s desire for control. So this was making the Silicon Valley model work in China,” Nahm says.

And it did work. For two decades, analysts say, the global financial markets have accepted what some call a myth, the idea that the VIE is legal and defensible under Chinese law. And in many ways, the backers were enormously successful. It opened China to foreign capital, built up China’s powerhouse tech firms and brought fortunes to Chinese entrepreneurs and their backers on Wall Street and Silicon Valley.

Now, though, with economists, analysts and even lawyers raising questions about the legality and risk of the VIE, China’s offshore shell game is about to face its ultimate test, before Beijing and Washington.

“What’s relevant now is that these original sins may be undermining the edifice [they were meant to support],” says Fraser Howie, the Singapore-based investment banker. “In the U.S. the legal and accounting structures are getting tougher, and in China the Party is rolling back the flexibility that it afforded the private sector.”

As for the VIE, and the offshore structures, Howie says, “We’re not sure what we’ve got.”

David Barboza is the co-founder and a staff writer at The Wire. Previously, he was a longtime business reporter and foreign correspondent at The New York Times. @DavidBarboza2