Credit: World Travel & Tourism Council, Creative Commons

One of China’s biggest corporate failures is at hand.

The HNA Group, the massive airlines-to-hotels conglomerate that between 2015 and 2017 went on a global shopping spree, spending tens of billions of dollars to acquire stakes in the Hilton Hotels, Deutsche Bank and other overseas properties, is heading towards bankruptcy reorganization.

The company, whose assets had already been seized by the state, said Friday that it would cooperate with a court in Hainan Province, where it is headquartered, after creditors asked the authorities to approve a bankruptcy restructuring plan aimed at paying down the company’s massive debts.

The move set the stage for the dissolution of one of China’s first global companies, a sprawling conglomerate that not long ago boasted $150 billion in assets, 400,000 employees and 20 publicly traded companies. It paid $6 billion to acquire a California electronics distributor called Ingram Micro. In the summer of 2017, HNA even held an extravagant event at the Beaux Arts Petit Palace Museum in central Paris to celebrate its emergence on the global stage.

At the time, HNA executives were barnstorming through the capitals of Europe, Asia and the Americas amassing massive debts by buying up high-priced hotels, aircraft leasing firms, logistics companies and high-rise office buildings. In 2016, it bought a 25 percent stake in Hilton Worldwide Holdings from the Blackstone Group for $6.5 billion. A year later, HNA paid $2.2 billion to purchase an office tower on Park Avenue in New York whose tenants included J.P. Morgan.

Now, HNA is an unfolding disaster, with Reuters reporting on Sunday that several of HNA’s listed companies have announced that nearly $10 billion has been embezzled or siphoned off from the companies by unnamed “shareholders” of HNA. And Caixin magazine is reporting that hundreds of HNA companies could be forced to restructure,1By some accounts the firm has more than 1,500 affiliated companies. and some, like its flagship company Hainan Airlines, may have to delist from China’s stock exchanges.

Credit: Anna Frodesiak, Creative Commons

How such a muscular, politically-connected company unravelled so rapidly is still a mystery. But analysts say the fall of HNA may have been spurred on by shifts inside the Communist Party.

In 2017, alarmed by growth in state backed debt, Beijing began to rein in Chinese firms and prevent them from moving huge sums of money offshore and splurging on overseas assets with state funds. The authorities also began targeting politically-connected tycoons suspected of corruption, siphoning off state funds or backing rivals to Xi Jinping, who at the time was moving to consolidate power.

The sweeping crackdown wrecked the ambitions of a pack of companies that the government referred to as “gray rhinos,” big, reckless firms that had been feasting on cheap debt to acquire overseas properties. The leaders of the pack were easy to identify: Anbang Insurance Group, which acquired Waldorf-Astoria Hotel in New York; the privately held oil giant CEFC, which invested heavily in Prague and courted Hunter Biden, the son of now President Biden; a financial conglomerate called the Tomorrow Group; the Wanda Group, which was active buying real estate and entertainment properties in the U.S., Europe and Australia — and HNA.

The conglomerates had a few common characteristics. They were all registered in China as privately-held firms, though each had significant state backing or had grown out of a state-owned enterprise. They were also politically connected (two even had business ties to the family of Xi Jinping). 2Wanda and the Tomorrow Group both had business ties to the family of Xi. And each was heavily indebted to the state, giving the authorities the ability to claim they were a threat to the stability of the financial system.

The downfall of these “gray rhinos” was swift. Wanda, the huge property developer and entertainment giant, was broken up and forced to sell off major assets. CEFC was seized by the state, and its chairman, Ye Jianming, was arrested for corruption. Anbang was also seized by the state, and its billionaire chairman, Wu Xiaohui, who married — and then divorced — the granddaughter of Deng Xiaoping, was sentenced to 18 years in prison for fraud and embezzlement. The state also seized the Tomorrow Group in 2020, three years after its chairman and founder, Xiao Jianhua, was kidnapped from the Four Seasons Hotel in Hong Kong and smuggled across the border into mainland China, where he was placed in detention by the Chinese authorities. (He is still believed to be under house arrest.)

According to WireScreen data, HNA also built its fortunes with hefty state financing and business ties to the families of some of China’s political elites, including the relatives of former prime minister Wen Jiabao.

Then there is HNA, which has been forced to sell off much of its global portfolio and was taken over by the state. The global pandemic helped push it to the brink. It has been a dramatic turnabout for the company’s co-founder, Chen Feng, a former government official and one-time aide to Wang Qishan, who is now China’s vice president.3Chen Feng worked as an aide to Wang Qishan in the late 1980s for a state firm partially financed by the World Bank Not so long ago, Chen was traveling the world on his corporate jet, even accompanying Xi Jinping to overseas events with world leaders, boasting that HNA aimed to be in the Fortune 100.

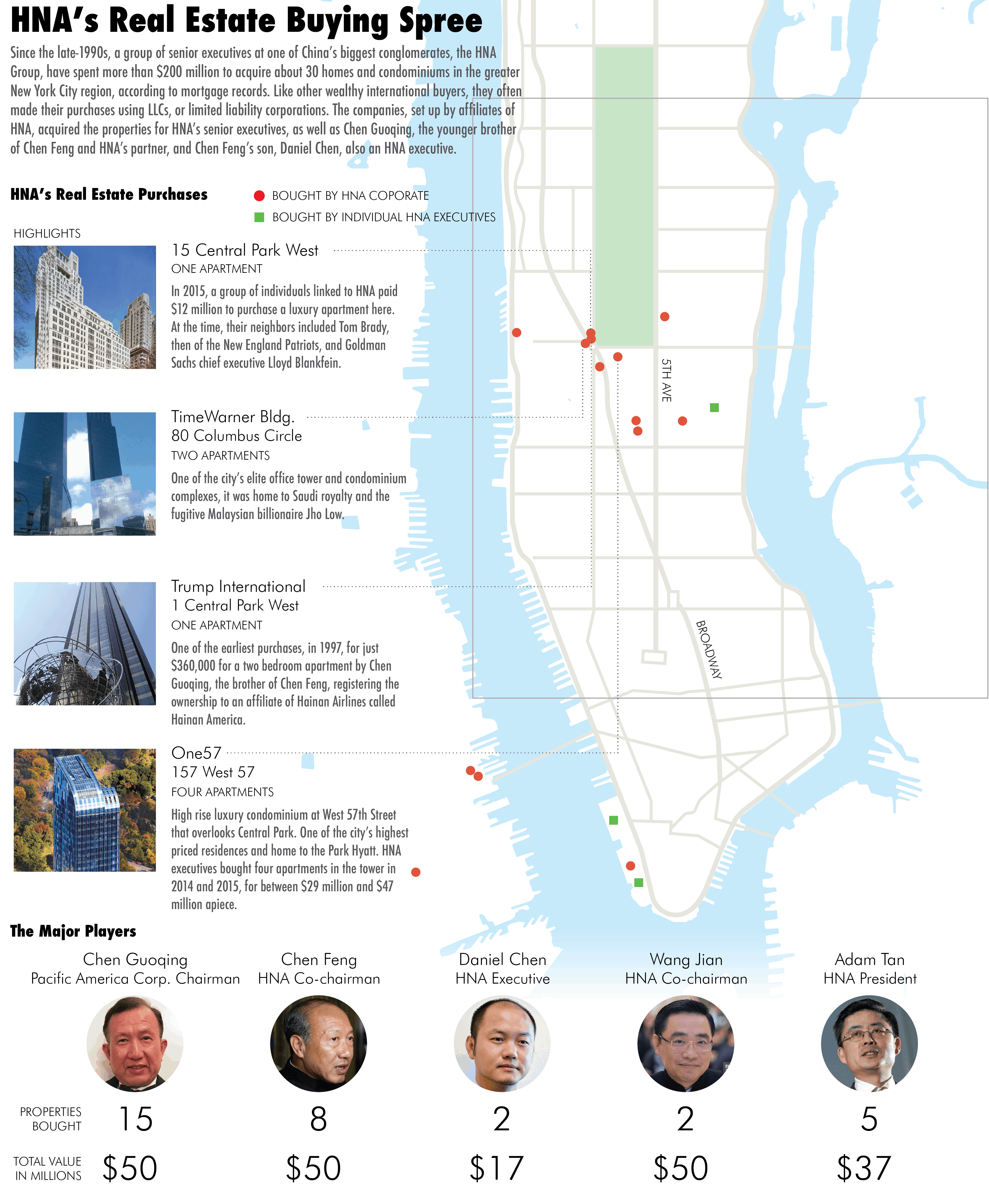

At the height of his company’s international push, Chen and his cofounder, the late Wang Jian, even acquired two of Manhattan’s most expensive residences, on the 88 and 89th floor of One57,4See this fantastic series in The New York Times about the TimeWarner building, where they also bought a condo: Towers of Secrecy the luxury condominium overlooking Central Park, properties that they bought for about $47 million apiece. (See chart below.)

Together, the two longtime partners helped transform Hainan Airlines, a startup airline with just one plane in the early 1990s, into a global powerhouse that controlled international hotels, resorts, golf courses, office towers and financial services firms. At one point, even George Soros was an investor.

But according to WireScreen, this publication’s data division, HNA also built its fortunes with hefty state financing and business ties to the families of some of China’s political elites, including the relatives of former prime minister Wen Jiabao.

Things began to unravel, though, beginning in 2017. Over the next few years, HNA was jolted by a series of sometimes bizarre allegations and scandals. The most notable was a year-long social media campaign waged by Guo Wengui (also known as Miles Kwok) a fugitive Chinese billionaire living in New York who would later partner with Steve Bannon. Guo used his social media account to publish photos, passports and flight records he claimed showed evidence that HNA was paying off senior Chinese leaders and their families.

Then the international media began to question why a man in his 30s named Guan Jun, with no corporate role at HNA, was listed in corporate records as the $100 billion company’s biggest shareholder (HNA declined to explain the individual’s identity or ties to the firm).5Not long after, HNA said Guan donated his shares to a New York charity. And then, a year later, Wang Jian, HNA’s co-chairman, died in a freak accident while on vacation in France.6See my story about the Brothers Wang and HNA here.

There was also growing evidence that HNA had poor corporate governance controls (the relatives of the top executives were allowed to buy and sell assets with HNA firms), and in the U.S., the company came under suspicion after it began courting influence with American politicians. HNA invested money in Jeb Bush’s investment fund a few years before his presidential run. And the company agreed to buy SkyBridge Capital, a firm run by Anthony Scaramucci, as he prepared to join the Trump administration. (The deal was called off after regulators failed to approve it.)

Now, HNA is said to be $100 billion in debt, despite a raft of major asset sales. And last year, the company’s chairman, Chen Feng, was humiliated. Because the company had missed debt payments, Chen was barred from buying first class tickets or high speed rail tickets. And just last week, his name was left off a list of the nine member Communist Party committee that oversees HNA.

Chen Feng, it appears, has lost control of the HNA Group.

David Barboza is the co-founder and a staff writer at The Wire. Previously, he was a longtime business reporter and foreign correspondent at The New York Times. @DavidBarboza2