The Luckin Coffee scandal carries the flavor of a familiar all-American scam: a high-flying Nasdaq stock with a technology hook collapses after accounting fraud is exposed. But Luckin is a Chinese company — and that highlights a unique set of risks too often ignored by U.S. investors.

These risks will make it very hard for the out-of-luck investors to recover significant sums from Luckin, which had been taking on Starbucks in China. Luckin’s shares plunged more than 90 percent after the company admitted to fabricating $300 million in revenue last year, and its stock has been halted for weeks.

Let’s start with Luckin’s ownership structure. The company listed on Nasdaq in May 2019 with a $651 million initial public offering, and followed that up with a $378 million secondary offering in January. Big investors like Blackrock jumped in.

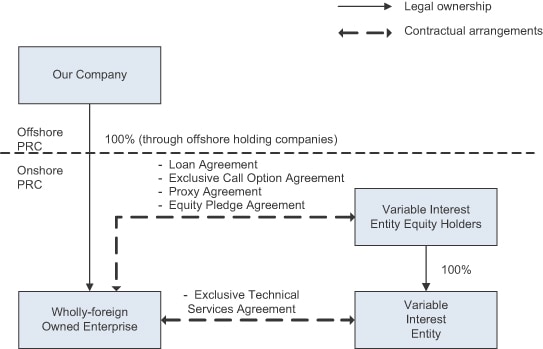

But investors in Luckin likely failed to understand that they were not buying a piece of the company that sells lattes across China. That company is based in China and is Chinese owned. Instead, investors were purchasing shares of a shell company set up in the Cayman Islands under something called a Variable Interest Entity structure, or VIE. The U.S. listings of Alibaba and dozens of other Chinese companies are also VIE-structured.

Credit: Alibaba SEC filings

Why Luckin used this structure isn’t clear. But China forbids foreign ownership in sectors of the economy that the government deems sensitive, such as technology and media. To sidestep the ban, Chinese companies that want to do an initial public offering in the U.S. or elsewhere abroad can set up a foreign or offshore company, often in the Cayman Islands.

The Cayman Islands company does not own the Chinese company’s assets. Instead, the Chinese assets are majority held by the founder or other designated individuals who must be Chinese nationals. In Luckin’s case, Luckin’s chief executive officer, Jenny Zhiya Qian and one of Luckin’s employees, Min Chen, hold 83.33 percent and 16.67 percent of the equity interest in the VIE, respectively.

The offshore entity then enters, typically through a Hong Kong intermediary, into contractual arrangements with the Chinese entity that entitle the offshore entity to all of the Chinese operation’s profits and cash flows. A power of attorney also provides the offshore entity voting and control rights. The offshore entity also obtains an option to purchase the Chinese assets should such a purchase ever be permitted under Chinese law.

Alibaba uses the VIE structure, and as of December 2017 there were 88 Chinese companies with U.S. listings set up as VIE’s, according to the Council of Institutional Investors. Luckin was a coffee shop at heart, so it probably could have had its assets directly owned, but it likely used a VIE that upped its tech credentials by saying it was more than just a coffee company.

However, there are a number of problems with the VIE approach. First, the Chinese government has never ruled that the arrangement and its contracts are legal. Their enforceability of such a structure remains in a legal netherworld. Investors in a VIE thus take on a legal risk; in a politicized environment, the Chinese government could disrupt the entire ownership arrangement by invalidating any part of it. This happened in 2012 when the Supreme People’s Court of China invalidated a VIE structure that had been used by China’s Minsheng Bank.

In addition, if the founder or other owners decide to seize the assets of the Chinese company, investors must sue in China to recapture them. There have been examples, notably in the ChinaCast scandal where the founder simply transferred the assets of the company to another entity, bankrupting the listed-U.S. vehicle. The Securities and Exchange Commission brought a successful enforcement action, but neither the SEC nor the company’s investors were able to recoup these assets.

Finally, any action to enforce shareholder rights will have to be brought against the offshore shell company. That litigation would typically be filed in the Cayman Islands, where the corporate governance regime is notorious for limiting a shareholder’s ability to sue and bring actions to enforce fiduciary duties. And Thomas P. Meier, the only independent director on the Luckin board, has resigned, which means that Luckin shareholders have no independent monitoring voice, even in the Cayman Islands vehicle.

All of these risks and limitations have been brought to bear in the case of Luckin Coffee. The SEC has been investigating the case and probably will bring suit to address what now looks like a classic securities fraud. But any judgment will likely be unenforceable in China. The best that the U.S. can do here is to bar Luckin’s officers and directors from accessing the securities markets. That’s pretty small beer.

Moreover, the SEC’s investigation is expected to be limited because China does not allow the foreign regulators to inspect or perform audits inside of China. The authorities insist they are protecting national security. This will be a flash point going forward, and it is already a concern for the U.S. Public Company Accounting Oversight Board. Sen. Marco Rubio, in an interview in The Wire, has called for greater access to these documents in exchange for continued Chinese access to U.S. capital markets.

Credit: Nasdaq (video posted on Facebook)

So, don’t expect much to come out of U.S. enforcement actions on Luckin. As for investors trying to recover the billions lost, they will be hoping that an offshore shell company will actually pay out anything left from Luckin’s assets in China — assets that may be judgment proof. That’s an uphill battle at best.

This leaves perhaps the most interesting twist of the Luckin case: the margin loans. It appears that Luckin’s chairman and controlling shareholder, Lu Zhengyao, and the company’s chief executive, Jenny Zhiya Qian, had $518 million in loans collateralized with their Luckin shares. Goldman Sachs, acting as agent for the lenders, said the loans were in default, prompting it to sell the equivalent of 76.4 million shares of Luckin stock. By the time of the announcement, however, the shares were already worth less than the value of the loan, indicating the lenders woud take a steep loss.

Don’t be too sad for Goldman; it appears to have hedged this position. But these types of loans to executives — which are often not reported in SEC filings — are ubiquitous in China. Executives use them to surreptitiously cash out of companies, giving them less incentive to competently run the enterprise. It also provides less incentive for these executives to do well for the U.S. investors in a VIE structure. Since these loans are not disclosed, investors may invest thinking that there is a fully invested founder with skin in the game, but not so with Luckin.

To be sure, there was still a classic American-style fraud here. Luckin had massive growth and made much of the fact that it was a disruptive force and a technology company, not a coffee chain, since Luckin had no cashiers and all ordering and payments were conducted through an app.

Luckin also forecast the usual venture-capital-sky-high potential market for its products; Luckin would get Chinese users to buy lots more coffee, even though tea consumption is currently 90 percent of the market.

The fast collapse of the company after its IPO shows a failure by investors, particularly those prior to the IPO, to conduct appropriate due diligence, another hallmark of technology investing.

The bottom line is that Luckin exposed the risks and fault-lines of Chinese investment. We’ve seen part of this movie before. In the reverse merger fraud over a decade ago, more than 100 Chinese companies listed in the United States and subsequently declared bankruptcy, as recounted in the 2017 documentary, “The China Hustle.” But those were low-quality Chinese companies that could not list in China, so they used a back door to list in the U.S. Luckin was of a different order, with a $12 billion market cap at its peak and blue-chip support Ernst & Young as its auditor and Credit Suisse and Morgan Stanley as underwriters.

In the wake of this massive scandal, integrity issues with Chinese companies that were little noticed before may get more media coverage as the coronavirus backlash adds to the tensions between the U.S. and China. Alibaba, which has been criticized for its accounting practices and has been investigated by the SEC in the past, may draw more examination.

The fault lines among U.S.-listed Chinese companies are substantial. Luckin’s misfortune may not be the last reminder of the risks.

Steven Davidoff Solomon is a professor of law at The University of California, Berkeley, and a columnist for The Wire. Before joining The Wire, he was author of a weekly column for The New York Times as The Deal Professor. @stevendsolomon