Eswar Prasad is one of the world’s leading thinkers and commentators on global economics and geopolitics. In his new book, The Doom Loop: Why the World Economic Order Is Spiraling into Disorder, he sets out why current trends in these areas are reinforcing each other to create a downward spiral that is creating instability both within and between countries. A former head of the China division at the International Monetary Fund, Prasad is now Senior Professor of Trade Policy and Professor of Economics at Cornell University, and a Senior Fellow at the Brookings Institution.

We spoke recently to discuss the themes of the book and his current views on China’s economic outlook. The following is an edited transcript of that conversation.

Illustration by Lauren Crow

Q: Your new book has a somewhat foreboding title: The Doom Loop. Could you kick off by explaining what you’re referring to, and what you’re trying to argue.

A: I actually planned to write a much sunnier book!

What I had in mind was that we’ve moved from a unipolar world in the 1990s when, with the fall of the Soviet Union, the U.S. became a dominant power in every respect — economic, military, financial. And now we’re in a world where economic power, at least, is much more evenly distributed.

As an economist, one tends to think that in most circumstances, competition is good for efficiency, discipline and stability, because it means that no one country can get away with very capricious policies for too long. So my story was going to be about how we are on a path of transition to a more stable equilibrium, although we may be experiencing some transitory volatility; and about all the forces that would take us back to a happier place.

But as I thought about each of these forces, I came to a very different conclusion: that each of them is, in fact, working to generate more instability rather than stability. And as I thought this through, the framing device of the book became a little clearer in my mind.

Economics, domestic politics, and geopolitics have now become intertwined in a way that is very difficult to separate. These elements could, of course, reinforce each other positively. But the concept of the ‘Doom Loop’ is that they are now stuck in a negative feedback loop where they are bringing out the worst in each other, and setting off a spiral of instability.

What lies behind the fact that these forces are now deepening rifts between countries and causing so many problems?

Let’s take globalization as an example — and by that I mean the integration of economies through greater trade and financial flows.

In the 1990s and the 2000s, there was a sense that globalization was generating benefits for countries that opened up their economies to trade and finance, and that this was generating a positive-sum game, whereby all the countries engaged in globalization would benefit together. In turn, this was offsetting the intrinsically zero-sum game of geopolitics, where one country can gain influence only if another country loses. This balancing force of globalization worked well for a while.

But it soon became clear that the benefits of globalization were being very unevenly distributed not just within countries, but also between countries. Some emerging market countries faced financial crises because of the debt that they had taken on. And among the industrial countries, there was a sense that there had been a hollowing out of their manufacturing bases. This created a class of people who felt disenfranchised, who felt that they were not able to benefit from any of these aspects of globalization, even though they were generating aggregate gains.

Populist politicians, who claim that they care about the interests of the common people, have been able to exploit this very effectively. The result is that globalization has come to be seen as a zero-sum game — or, in the eyes of some politicians, even a negative-sum game. The balancing force that once offset the zero-sum game in geopolitics is gone, and trade, financial flows and geopolitics are now feeding off each other in a very negative way.

As I just alluded to, this is also infecting domestic politics. It’s much easier when a country is not doing terribly well, to look outside and blame the ‘Other’ — it could be immigrants, it could be China — as being responsible for outcomes that many people feel are hurting their economic prospects. While there might be other forces, including domestic policies and technology, that are really at play, it’s a much more potent message to say that it is malign external forces that are causing problems.

…while we celebrate the overall benefits of things like globalization, technology, and so forth, we don’t pay sufficient attention to the distribution effects of many of these developments, both within and between countries.

So now you can see how what used to be a positive force — economics — affects domestic politics, and in turn affects geopolitics. This is the ‘Doom Loop’ encapsulated.

And to be clear, it’s not so much that globalization itself is retreating, it’s more the perception that its benefits have gone into reverse — and that’s creating the doom loop.

The perception has changed. As you pointed out, overall global trade has not actually declined, despite all of the dynamics that we spoke about.

| BIO AT A GLANCE | |

|---|---|

| BIRTHPLACE | Trivandrum, India |

| CURRENT POSITION | Professor at Cornell University and Senior Fellow at the Brookings Institution |

But there is one very important change. The benefits of trade are so great for consumers and businesses that it is going to continue. But trade and financial flows are fragmenting along geopolitical lines. In other words, geopolitical allies are increasing their trade with each other. Multinational businesses are setting up supply chains in a manner that reduces geopolitical risk, rather than in the most efficient, cost-saving manner possible — which in turn means that financial flows, like foreign direct investment, are also flowing along geopolitical lines.

Trade and financial flows used to act as bridges across geopolitical divides, especially between the two current superpowers — the U.S. and China. But what we are seeing right now is that such flows are essentially deepening geopolitical rifts. It’s not like globalization has ceased, but this fragmentation is creating its own sort of instability.

And you argue, as well, that companies that are taking what may seem to them rational steps to improve the resilience of their supply chains, may actually be adding to the problem.

Businesses are responding the way you would expect them to when faced with new sources of risk. One way to do it is by diversifying, both in terms of sources of inputs and raw materials, and also by finding different markets for their exports. But they can also do it by retreating inward; or by trying to minimize geopolitical risk, by looking to increase trade and find investment in countries that they see as aligned with their home countries.

Once upon a time, businesses used to be a great stabilizing force in international relations. The U.S.-China relationship is a perfect example of that. No matter what the rivalries were between the U.S. and China, American businesses and financial institutions had a very strong interest in using China as part of their supply chains, and in selling into the Chinese market when it comes to goods or services that increasingly affluent Chinese consumers might demand. There was a very strong interest in maintaining stable ties.

Likewise, Chinese businesses saw America as worthwhile as an investment destination, as a potential production base, and also in terms of enabling them to get easier access to certain types of technology. Business flows in both directions acted as a stabilizing force.

But businesses are now retreating back to their home countries, especially in the U.S.-China context. While they may think they are de-risking, what they are doing is removing themselves as a stabilizing force in the relationship between the two countries. Anytime there is a provocation between the two countries now, there is no longer a very strong constituency saying, let’s calm things down, because we would really like to keep the relationship on a stable footing. With that balancing force gone, the internal political dynamics in both countries are leading to a ratcheting up of tensions between the two.

Why are free flows of financial capital around the world now more of a destabilizing force than they were before?

The benefits that many countries, including emerging market countries, gained as a result of freer capital flows were quite significant. More free movement of capital across countries means that businesses around the world can access global pools of capital rather than just domestic sources. Both retail and institutional investors can also more efficiently diversify their portfolios, improving their risk-return trade-offs.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOKS | We the People: A History of the U.S. Constitution, Jill Lepore (nonfiction); Victory City, Salman Rushdie (fiction) |

| FAVORITE MOVIE | The Last of the Mohicans |

But the type of capital inflows that many emerging market countries could obtain used to be largely in the form of debt, which often ended up in crises of various sorts. That has actually changed in a very positive way, with emerging market countries now getting more foreign direct investment in the form of equity. Even when the financial crisis hit and banking capital flows retreated, foreign direct investment continued to be very strong across countries.

That, again, is now changing. It used to be the case that businesses saw the virtue of using foreign direct investment as a way of setting up lower-wage production centers, creating very efficient supply chains. That, again, acted as a bridge between countries.

That bridge is now being destroyed because even capital is now becoming a matter of geopolitical strife. Many countries, including the U.S., are limiting the ability of foreign investors to come into their economies in certain sectors. You even have outward investment into certain countries being restricted. Then, of course, you have the behaviour of businesses no longer using foreign direct investment to maximise efficiency and reduce costs. The emphasis has shifted towards resilience.

If an official from the Trump, or even Biden administrations were to join this call, they might say we still want to benefit from trade and investment, we’re just taking a few pragmatic steps to limit the risks involved.

It’s not just a matter of limiting risks. One of the elements I point out in my book is that there is a sense that the rules of the game, governing international trade and finance, have not been applied evenly across all countries.

In the U.S. and many Western countries, there is a very strong narrative that the second largest economy in the world, China, took advantage of the rules, that its accession to the World Trade Organization basically allowed it to gain markets for its exports around the world; and it did not entirely play by the rules in terms of giving foreign firms access to its markets. Foreign firms that wanted to operate in China, to enter the Chinese market, or who wanted to use it as part of their supply chains, found that there were a variety of restrictions, administrative and otherwise, that made it difficult for them to operate freely.

This is a very important issue that feeds into the ‘Doom Loop’. If everybody agrees on a common set of rules of the game, that should be a stabilizing force eventually. The problem is that there is a sense that the existing institutions like the WTO, the IMF and the World Bank, all of which are meant to create and also administer the rules for the game, are not operating in a way that everybody sees as fair.

Of course, fairness is in the eyes of the beholder. Countries like the United States now see some of these institutions, especially the WTO, as being too soft on China; but at the same time, China and other emerging market countries, including India or Brazil, see institutions like the IMF and the World Bank as tilted too much towards the interests of the advanced economies of the West.

Now, the problem is that as the emerging market economies have become more economically powerful, they have decided that they can either try to change the rules of the game from the inside, or do it through external pressure. And of course, led by China, emerging market economies have been setting up their own institutions, like the Asian Infrastructure Investment Bank, the BRICS’ New Development Bank, and so on.

One might argue that institutional competition is not necessarily a bad thing. The concern I have is that this is leading to a fragmentation of rules. And with different countries operating under different rules, you no longer have a stabilizing force.

What’s at the root of the creation of these doom loops?

The root problem lies in the fact that while we celebrate the overall benefits of things like globalization, technology, and so forth, we don’t pay sufficient attention to the distribution effects of many of these developments, both within and between countries. And the fact that we do not pay enough attention to those — and I think one can implicate a variety of people in this — has led to false populists being able to create a very effective narrative of resentment.

Some of the intrinsic vulnerabilities of what we thought was the dominant paradigm in the 1990s, basically that of liberal, market-oriented democracies, are becoming evident. And what we are seeing is that the institutional framework underpinning these terms was very fragile.

…superpower competition has gone far beyond just economic and military power to something much more fundamental about the organisation of economic, political, legal, and social systems.

So what do I mean in more concrete terms? Globalization generates a lot of benefits, but as I mentioned, the political and economic elites seem to get many of the benefits. It seems that they can in turn basically capture the democratic system so that the rules of the game are tilted in their favor — if you think about tax and regulatory regimes, and the reductions in social safety nets made in order to reduce the tax burden overall. All of these mean that those who are benefitting from forces like globalization can accrete even more of those benefits, without doing anything illegal or illegitimate. They just change the rules of the game. These internal dynamics create a sort of internal lock that becomes very difficult to get out of. And it’s going to take a lot of work because it turns out that these dynamics are not going to be very easy to reverse.

You were in Davos recently, where one of the highlights was a speech by Mark Carney, the Canadian Prime Minister, that touched on many of the themes that you’re talking about, such as the fundamental fragility of the rules-based order. What did you make of his diagnosis?

One of the things he pointed out was that the world has changed. The notion of a multilateral rules-based order that could maintain amity between countries is gone. We have two superpowers that have very different visions for the world.

It’s also worth thinking about where we are right now in the present conjuncture. The U.S. is, in a sense, isolating itself from the rest of the world, through tariff barriers and its geopolitical attacks on both old rivals and also traditional allies. It would seem logical for the rest of the world to say, let’s move on without the U.S..

On the other side, you have another superpower in China that is not seen as very trustworthy either, because of the nature of its institutions. And in particular on the economic front, there is a huge concern right now that the Chinese economy has become very dependent on exports. Countries around the world — including advanced countries like Germany and France, or emerging markets like India — are very concerned about being swamped by Chinese exports.

So neither of these choices is particularly savoury, in terms of alignment. Carney’s speech articulated the difficulty that the rest of the world faces. He argued that ‘middle powers’ need to band together — although he was quite pragmatic, saying that the middle powers may not have complete cohesion, and that they should think about specific issues where they can get together.

The problem is that the middle powers, which is basically the rest of the world including Europe, consists of small countries, large countries, rich countries, poor countries, whose interests are not perfectly aligned. In fact, there is a lot of dissension within this group. So yes, coming together on specific issues might make sense, but it doesn’t create deep rooted alliances.

Middle powers were a force that I originally thought could serve to promote stability. But my view now is that middle powers are taking an approach of forming issue-based alliances. For example, in the quest for cheap and plentiful oil, India did not participate with the sanctions on Russia when it invaded Ukraine. But on other issues, it sees its values as aligned more with the West. So it sort of teeters from one side to another. What it doesn’t do is serve as a balancing force. This is true of other middle powers as well.

Carney’s approach, while pragmatic, creates certain problems of its own in terms of whether the middle powers will just foment even more instability, or act as a force of stability.

To what extent is the fact that we now have two major economic powers with incompatible political systems and values causing the doom loops? Whilst China was rising, and wasn’t a direct challenge to the U.S., that conflict could be managed. But now it has reached a certain level of economic power and status, the clash between it and the U.S. is contributing to the doom loops?

This is a really important point. When I was writing my book, my original thesis was that eventually this must all lead to some sort of stability, and a better world. I thought back to recent history. With the collapse of the Soviet Union, as I mentioned, the U.S. became the dominant power. After that, it looked for a while like Japan might rise as a rival to the U.S., and then it faded in the 2000s. With the creation of the euro, it looked like the Euro zone, or Europe more broadly, might become a rival to the U.S., but that didn’t happen also.

There was one very important difference in those episodes relative to the U.S.’s rivalry with China. Europe, Japan, the U.S. all see fundamentally eye to eye on issues about how you organize a society, a political, economic and legal system. The rest of the competition was really just an economic rivalry.

Right now, we have a rivalry between the two superpowers, which is not just about economics. It is about fundamentally their completely incompatible visions of the world, what the role of government ought to be, what the rule of law actually means, and what the right form of political and economic organisation is.

It’s going to be practically impossible to meld these two visions in any way, because they are so fundamentally different. The lesson here is that superpower competition has gone far beyond just economic and military power to something much more fundamental about the organisation of economic, political, legal, and social systems. This is why I think that we are stuck with this instability for some time to come.

You call in your book for a strengthening of global institutions, or the creation of new and fairer institutions, that can reestablish global rules that people and countries can broadly stick by. Is that your central focus in terms of finding a solution to the Doom Loop?

That’s again crucial. Given that much of the book is very dark, I did want to leave my readers with some light at the end. Before we move to solutions, understanding the forces that brought us to where we are is really important, which is what much of the book is about.

| MISCELLANEA | |

|---|---|

| FAVORITE MUSIC | Opera — with a particular soft spot for operas by Puccini, Glass, Verdi. I even enjoy Chinese opera — both Beijing and Kunqu opera. |

| MOST ADMIRED | Those who never attain fame, fortune, or success, but still never give up trying, fighting, pushing ahead. |

The answers about how we extricate ourselves out of the doom loop are at one level kind of obvious, but at another level, extraordinarily difficult to move towards. It requires a combination of us as citizens being much more engaged, not just as citizens of our countries, with short-term interests, but of our community, the broader world order, recognizing that it is only common prosperity that is going to lead us to a better place. We need better community, business, and national leaders who can help us see beyond our short-term prejudices and not pander to our fears, but instead help us hope for a better future.

But ultimately, we also need corrective mechanisms in the form of both domestic and international institutions. The domestic institutions that I think are really important include an institutionalised system of checks and balances, an open-ended democratic system of government, the rule of law where even the government is subservient to whatever rules it creates, and elements of the economic institutional frameworks, such as an independent central bank. These are really important for an economy or society to be able to correct some of these malign forces.

And then at the international level, certainly we need institutions that are seen as much more legitimate and credible, that can administer the rules of the game in a sensible way that is seen as fair. The paradox is that while better institutions, both domestic and global, are certainly the answer, the task of rebuilding them at the moment has fallen into the hands of the very leaders who are basically shredding them. So it is going to take a lot of work to get back to a place where we can rebuild these institutions.

A more positive take is that one might view this as a time of opportunity. Many institutions, especially international institutions, are really losing their legitimacy. So rather than trying to fix them at the margin, maybe we could see this as an opportunity to create completely new institutions from scratch that don’t have most of the flaws that the present ones do. That, I recognise again, is a tall order.

Deep down, where do you worry that the Doom Loop could lead us to?

I worry that we might just accept the doom loop as our destiny, rather than trying to extricate ourselves from it. If it becomes each country for itself, each household for itself, where we stop thinking about how we can benefit through shared prosperity and just start thinking about narrow short-term interests, the doom loop will get entrenched and become much, much harder to get out of.

The doom loop is not inconsistent at all with things looking good on the surface. Financial markets can do well, economies can do well. But under the surface, you still have these tensions bubbling up, and these could explode in some nasty fashion. I’m hoping that we won’t let it get to the point where we need a crisis of some sort, either social or economic, to effect change: but sometimes that’s the way it does fall.

On China, you write in the book that the current juncture for the economy is more worrying than ever before. Why do you worry in particular about the current situation, and where do you think things are headed?

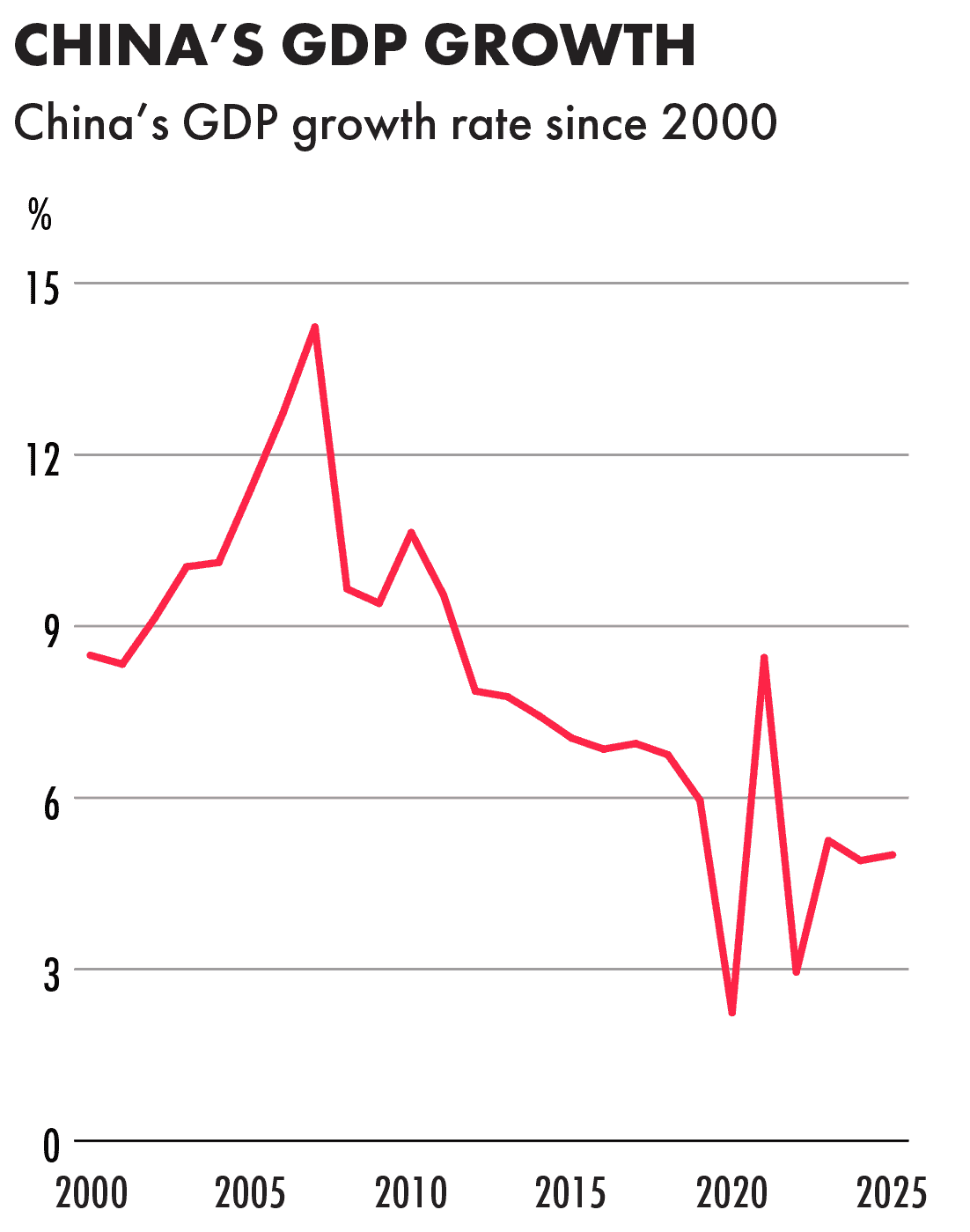

There have always been reasons to worry about the foundations of the Chinese economy, where they are weaker than they might appear on the surface. At the moment, it looks like there are very significant special problems. The Chinese economy has been able to grow, despite all the inefficiencies built into the system, first by reallocating a lot of labor from low productivity to high productivity sectors; and from the real estate sector contributing a great deal to growth. Exports have been a very important source of growth too.

But we’re at a point where the traditional drivers of growth are not working very well anymore. Bank-financed, investment-driven growth is creating too many problems. The real estate sector is finally reaching a point where it’s not going to make a big contribution to growth, and it’s negatively affecting household wealth. Demographic factors are also not working in China’s favor.

The room for maneuver is really shrinking very fast. We see this in terms of disaffection with the government, which one sees in consumer confidence measures and also in measures of household consumption.

All of these things are coming together at a time when there seems to be less confidence both in the private business community, and also among households, about the government’s ability to navigate around these difficulties. To its credit, the Chinese government has created enough room for maneuver. They can reach whatever growth target they set for themselves, whether it’s 4.5 to 5 percent for the next couple of years.

A lot of the improvements made in the post-Covid era have stalled or been reversed, in terms of rebalancing the economy so it’s less dependent on investment or export driven growth, and getting the services sector to contribute more to GDP than manufacturing. The room for maneuver is really shrinking very fast. We see this in terms of disaffection with the government, which one sees in consumer confidence measures and also in measures of household consumption.

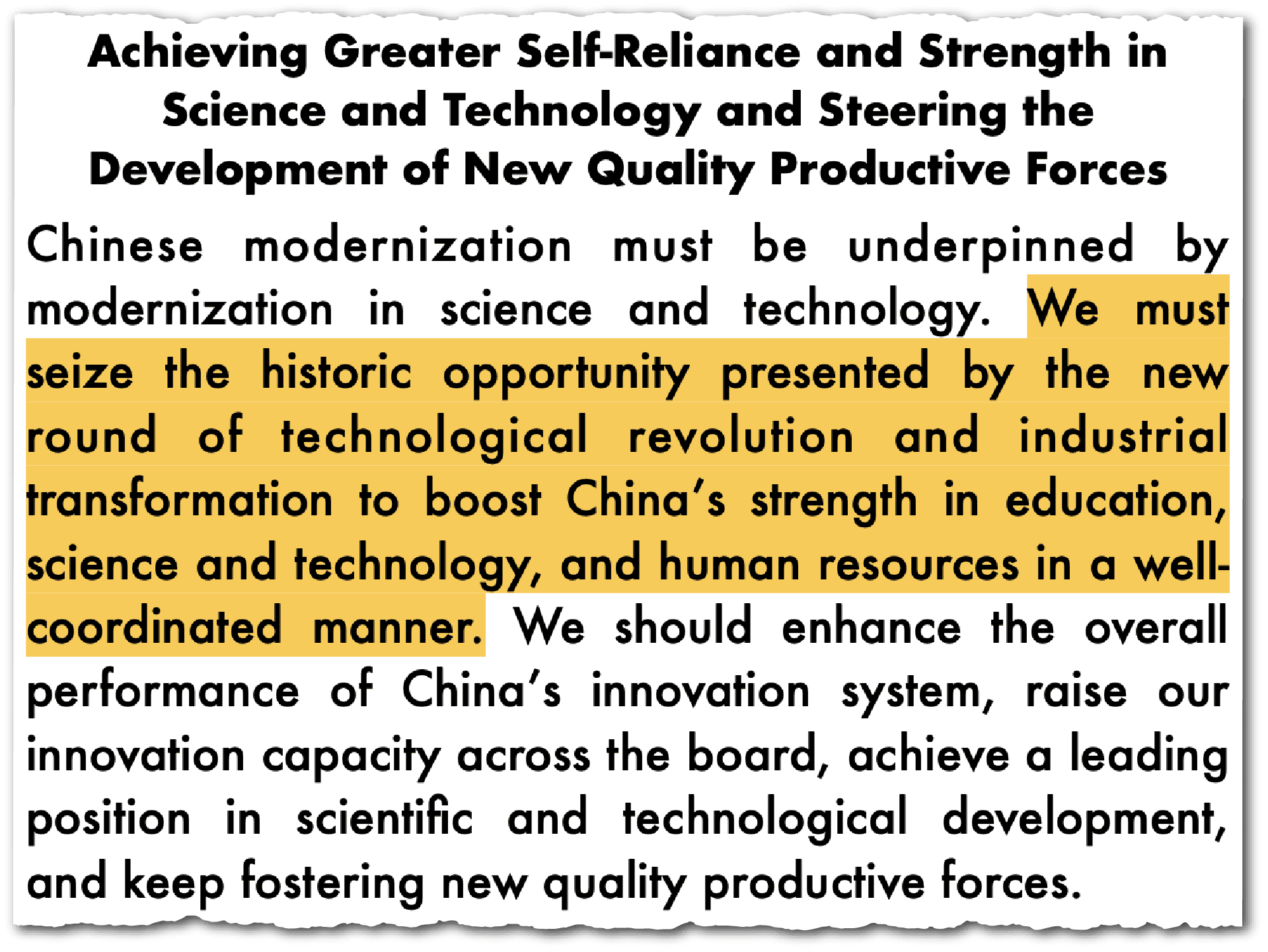

The solution, which the Chinese government seems to understand very well, requires continued economic rebalancing and also measures to increase productivity. If you don’t want to invest more, because that’s not working very well, and if the labor force is shrinking, then the only way you get growth is by generating productivity. To its credit, the government has tried to move into higher tech, higher value-added industries. It’s good that there is a sense of urgency in what one sees coming out of the CCP’s working documents.

I have learned not to predict any sort of meltdown or crisis. I think they have enough control. But the growth model is coming under increasing strain.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps