China’s national leadership is more worried about the country’s economy than many observers realize — judging by the finer details of the 15th Five-Year Plan.

For the first time, the plan includes instructions to prepare for a future financial crash by building out bailout funds. But while the risk of such a crash is primarily tied to the strained budgets of struggling local governments, most of the solutions Beijing proposes would require them to simultaneously insure more of the economy while somehow maintaining fiscal austerity.

The 15th Five-Year Plan contains two sections focused on China’s financial system. Most international coverage has touched on the first, titled “Building a Strong Financial Nation” (金融强国) which contains China’s ambitions to internationalize the renminbi and develop digital financial platforms.

The second section, which has received relatively little attention abroad, shows a very different story. Titled, “Safeguarding the Nation’s Economic Security” (保障国家经济安全), this section betrays a defensive, anxious leadership deeply worried about financial failure.

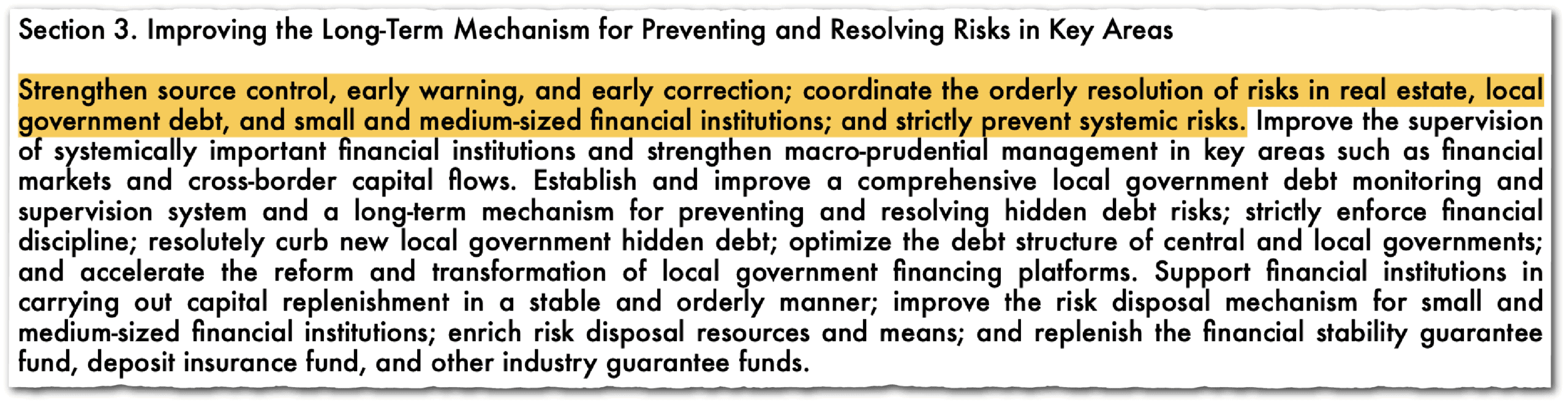

There are three main places the authors of the 15th Five-Year Plan expect calamity could hit: the real estate market, rural banks, and indebted local governments. The plan includes instructions to build up bailout funds to deal with emergencies in each of these areas. In reality, they are deeply intertwined, and already under deep strain.

Let’s start with a look at the real estate market. In many ways, China’s housing bubble resembles other booms and busts around the world. What makes China’s situation different is how much local governments depended on real estate price rises for funding. Now that the bubble has burst, local governments are scrambling.

This is because most of China’s tax revenue goes to the central government, which then allocates funds to regional governments or reserves it for central government initiatives. Yet local governments still carry the cost of the majority of public services such as healthcare, schools, and public safety.

Luckily, there is a convenient loophole: local governments do not have to share non-tax revenue gained through land leases and real estate revaluations. Moreover, auditors brought on to determine land asset values have had to work on behalf of the same local government that controlled their ability to legally remain in business. In turn, the assumption became that every new housing complex on local government balance sheets would soon be a bustling metropolis — and so they were valued as such. As long as housing prices went up and construction of new homes continued, the money would keep flowing.

The party ended between 2020 to 2022, when overleveraged real-estate developers ran out of money for construction and stopped hundreds of uncompleted projects which had already been sold. A survey conducted in early 2022 found 45 percent of homebuyers were waiting on unfinished properties. Many buyers were left with mortgages for homes that didn’t exist, and consumer trust in purchasing housing evaporated.

In summer 2022, consumer frustration transformed into protests in central China. That same summer, several Henan banks experienced a bank run, prompting more regional protests by depositors. In parallel with the flagging housing market, a rural banking crisis had begun.

After initially responding to the situation with threats and force, China’s central authorities recommended local governments compensate consumers affected by the real estate bubble or rural bank closures by providing partial deposit insurance, and financing the completion of already sold buildings. Beijing ordered both the fiscal and logistical remedy to be borne by local governments, without any new alternative sources of revenue.

Fast-forward to the 15th Five-Year Plan. Unlike prior plans, which broadly alluded to risks but shied away from specific policy prescriptions, it gives direct instructions to prepare bailout funding by refilling The Financial Stability Protection Fund (金融稳定保障基金) — created in 2022 to allow direct lending between the central bank and struggling enterprises in cases where failure could create a domino effect devastating the economy; and the Deposit Insurance Fund (存款保险基金), set up in 2015 to cover all deposits made at banking institutions within China, including rural credit cooperatives.

An economic crunch will not mean China will stop being a major global power… Overseas observers in the United States and Europe should plan on the Chinese Communist Party and current government remaining in power for the foreseeable future.

While the central government will be responsible for financing these two funds, Chinese media reporting suggests that during the Five-Year Plan drafting it was proposed that local governments should take parallel action by setting up special bonds for small banks in need of capital injection. This is already underway, with at least 86 small regional banks receiving capital increases this year, primarily through local government capital. To put it bluntly, bailout funding is being prepared at both at national and local levels.

How these rainy-day funds will be financed is not yet clear. The 15th Five-Year Plan directs local governments to curb debts, forcing them into ongoing austerity mode. Even prior to these instructions, public employees such as schoolteachers, bus drivers, and the like, have had to deal with salary cuts. Fines and penalty fees are increasing as regional governments look for different sources of revenue. Local police offices have taken to crossing into other jurisdictions to extract fines, a practice so rampant Netizens have termed the practice “offshore fishing”.

It is unclear what revenue options are available to local governments without a major overhaul of the national tax revenue distribution system.

The rest of the 15th Five-Year Plan suggests China’s leadership is betting hard on technology-driven productivity changes jumpstarting employment, revenue, and consumption. Maybe China’s leadership imagines they will recreate the boom from the 1990s and 2000s, when technological catchup and new infrastructure transformed every aspect of society. Or more conservatively, maybe they know this is a long shot but consider it the best of many bad options.

An economic crunch will not mean China will stop being a major global power, or stop its progress in scientific research. China will still have the world’s largest population and second largest economy. Overseas observers in the United States and Europe should plan on the Chinese Communist Party and current government remaining in power for the foreseeable future.

But economic shocks create aftershocks across the world, and even after a decade of rising trade tensions the U.S. and China are still among one another’s top trading partners.

We should all take note that China’s economy is in a tenuous situation right now. The 15th Five-Year Plan is preparing for a financial crisis. We should be mentally preparing for one too.

Ann Listerud is a senior analyst at Pamir Consulting who specializes in China’s industrial and economic policy making systems. She formerly worked for Strider Intelligence, Sayari Analytics, Trivium China, and the U.S.-China Economic and Security Review Commission. Ann has previously worked in Kaifeng, Shenzhen, and Tokyo. She holds a Master’s in International Affairs from the UC San Diego School of Global Policy and Strategy.

{kind=link}