This year’s National People’s Congress in China has taken place against a troubled international economic and geopolitical backdrop. The fighting in Iran, a sharp rise in oil and gas prices, and the shipping freeze in the Straits of Hormuz — the chokepoint through which China gets over half its oil imports — has already put significant elements of the government’s largely sanitized economic thinking and forecasts at risk: not least for exports, which have been a key growth driver.

The new 15th Five Year Plan (FYP, 2026–2030) is predictably optimistic as it parades the government’s industrial policy and self-reliance priorities. Yet, the combination of a fractious external environment and stubborn structural problems at home beg the question as to whether the government’s messages for the year ahead, and over the plan period, count as confident — or cavalier.

The main macroeconomic projections and forecasts for 2026 appear unremarkable. The GDP target has been set at 4.5-5 percent, allowing a little slippage from last year’s 5 percent. But that target still exceeds China’s sustainable rate of growth of about 3 percent, and may only be attainable via more non-productive investment, and higher indebtedness. Other targets, including for unemployment, gross job creation, inflation and personal income were mostly unchanged but are also of little informational value. The normal optimistic tone, therefore, is worth checking against the caveats.

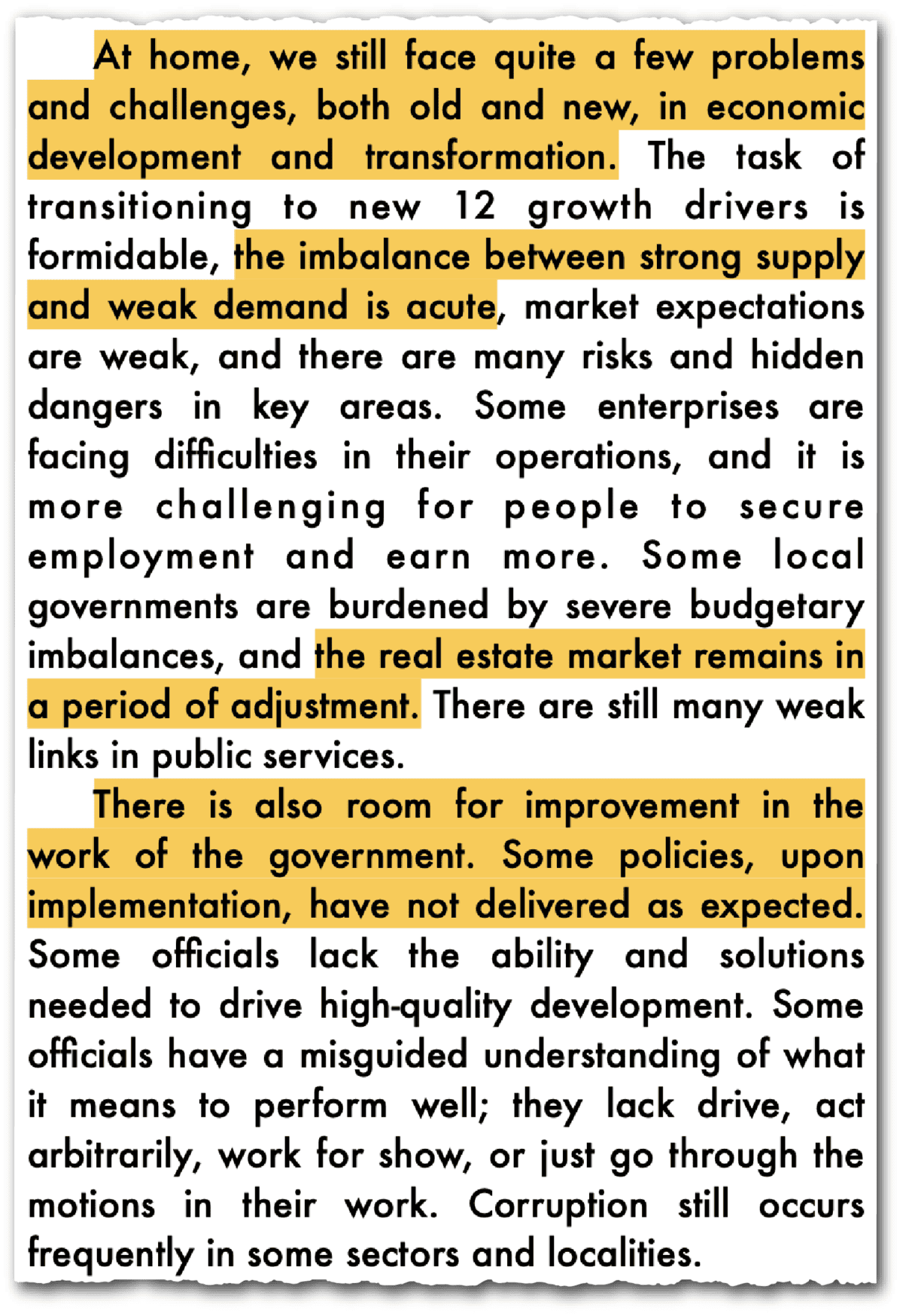

The Work Report itself, acknowledged that ‘the imbalance between strong supply and weak demand is acute’, an allusion to China’s chronic overcapacity and deflation. It recognized underlying problems in employment and income growth: some estimates are that informal or gig workers now account for almost a third of the labor force and over 40 percent of the urban workforce. It said that fiscal revenue-expenditure tensions in some localities are pronounced: but this understates the revenue crisis for local governments whereby their total inflows fell last year to just over 15 percent of GDP, compared with a peak of over 27 percent in 2015. Inevitably, the report said the real-estate market is ‘still adjusting’, which is a euphemism for a sector that is still in decline: prices haven’t been allowed to adjust properly, while consumer confidence and banks’ loan portfolios are still both at a low ebb.

The report from the National Development and Reform Commission, China’s economic planning ministry, was more strident. After having referred last year to ‘involution in some sectors’ and ‘some business difficulties’, this year it took the gloves off. It says, ‘The imbalance between strong supply and weak demand is acute; real-estate development investment continues to decline; infrastructure investment growth has turned from positive to negative; manufacturing investment growth has slowed further; overall investment faces mounting downward pressure; consumption growth lacks momentum; and the price level continues to run low’.

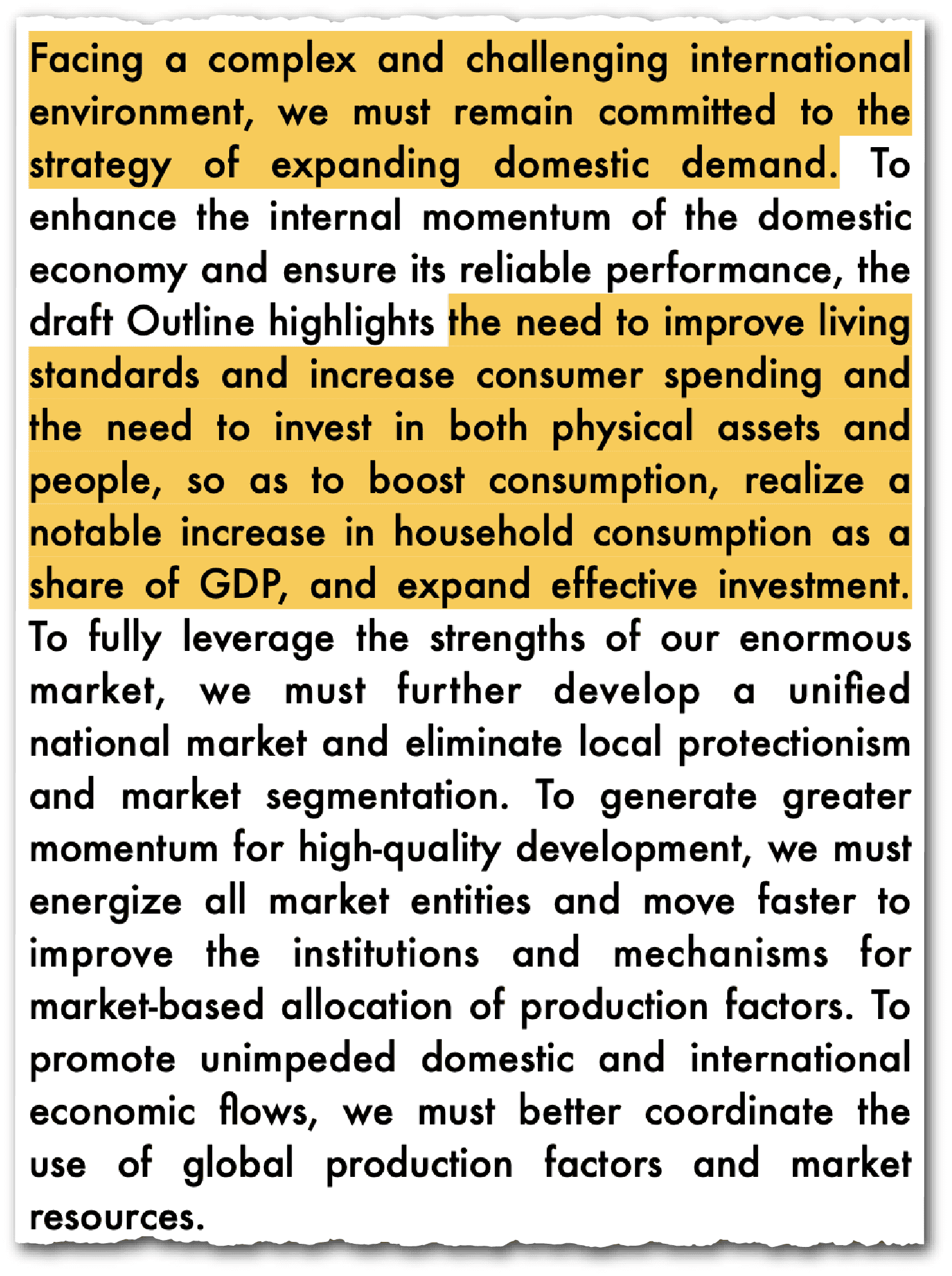

Boosting consumption — which many economists, myself included, see as China’s top economic priority — figures prominently in official rhetoric meanwhile, but hasn’t figured in a significant fashion in practice.

This is a much sharper assessment. It asks questions, implicitly, about policy options, and about the perennial issue of how, or if, to rebalance the economy towards higher consumption.

The government meanwhile says it intends to maintain a pro-active monetary policy, but this tool lost its leverage a long time ago. Interest rates are already low, but credit demand is weak, and banks’ loan and capital positions are under pressure. Additional easing moves are expected but necessary moves such as a radical change in the capital adequacy of banks, the discipline of hard budget constraints in credit allocation, and the orientation of the financial system away from local government and SOEs to private firms and efficient capital allocation are not even on the agenda.

The government’s scope to use its budgetary policy is also limited. Beijing’s plans are quite conservative on paper: the central government fiscal deficit remains at about 4 percent of GDP. But the actual deficit is nearer 8.5 percent, allowing for transfers from other funds, the regular issuance of special purpose bonds, and other off-budget entities. Adding in local government finance vehicles, the IMF thinks China’s augmented deficit is over 14 percent of GDP.

CHINA: SELECTED ECONOMIC INDICATORS

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 (est.) | |

|---|---|---|---|---|---|---|

| Nominal GDP (RMB billion) | 104,224 | 117,311 | 123,341 | 129,427 | 134,921 | 140,188 |

| Augmented debt (percent of GDP) | 97.50% | 98.70% | 104.20% | 111.30% | 117% | 126.60% |

| Augmented net lending/borrowing (percent of GDP) | -16.20% | -12.10% | -13.50% | -12.80% | -13.20% | -14.30% |

Sources: Bloomberg; CEIC Data Company Limited; Wind; IMF International Financial Statistics database; and IMF staff estimates and projections

The central government’s balance sheet could be used more, and some of the new bond issuance this year will do that. There will be new issues to fund national strategies, security, consumer product and industrial equipment upgrades, large state bank recapitalization, and new consumer loan interest guarantees. Overall though, the fiscal stance is only mildly stimulative.

Boosting consumption — which many economists, myself included, see as China’s top economic priority — figures prominently in official rhetoric meanwhile, but hasn’t figured in a significant fashion in practice. The government is planning to allocate additional funds to subsidize the consumer goods trade-in scheme, a new small fund to subsidize loans, measures to deal with the consequences of aging, and extra funding for childcare, pensions, education, and rural-urban income disparities. However, the scale of the fiscal transfers to households is small, the increases to social welfare programmes are limited, and there are no plans for any significant redistribution of assets or wealth.

There had been a widespread expectation that the new FYP would contain a commitment to raise the consumption share of GDP, but this was not included. There are references to raising consumption, but equally, there are also many references to investment in the context of 109 projects.

In the Plan, China’s stated high level priorities — namely the pursuit of industrial policy, the exploitation of ‘new productive forces’ in science and technology, and the realization of self-reliance — are spelled out in detail. Perhaps in a nod to the problems of overproduction and deflation, or the harm imposed by involution competition, the government’s emphasis on strategic emerging industries has given way to a focus on the ‘smart’, or digital economy. This elevates integrated circuits, aerospace, biopharmaceuticals, and the low-altitude economy to pillar industries, and nurtures industries of the future such as hydrogen and fusion energy, quantum technology, embodied AI, brain-computer interfaces, and 6G technology. The government also wants to promote ‘unconventional measures’ in important chokehold fields, including semiconductors, high-end machine tools, basic software, and advanced materials.

The 15th Five Year Plan may trumpet China’s progress in science and technology. But that isn’t the yardstick against which either China’s ability to cope with such a challenging external environment, or its capacity for change, should be judged.

China wants to double income per head (2020-2035), which would need growth of 4.2 percent a year for the next decade. This is still about a third higher than the economy’s trend rate of growth. It could be done without fuelling unproductive investment, but only if the government were willing to embrace reforms it now considers politically awkward or impossible.

Yet the current trajectory, based on a relentless rise in manufacturing investment, and high trade surpluses with the rest of the world also won’t work. Many nations will be unwilling to accommodate China’s advanced manufacturing ambition for fear of compromising their own industrialisation, and rising trade tensions are liable to intensify. Moreover, as the recently published IMF Article IV report on China states, much to Beijing’s chagrin, China should reverse its unprecedented-in-scale industrial policy — which has not been reflected in productivity gains — and adopt a more forceful policy response to boost consumption, so as to both lower the country’s unsustainable trade surplus and also resolve deflationary pressures.

None of these things look likely to happen any time soon. Xi Jinping certainly exudes confidence in asserting that the new industrial revolution will bring prosperity to China, as well as geopolitical dominance —a political judgement that is now set in stone.

China’s modern manufacturing and technology sector is certainly dynamic. Yet given its small size, it is cavalier to imagine that its success can compensate for, or change the structural problems in the other 85-90 percent of the economy, where fiscal and financial weaknesses, misallocation of capital, overproduction, low productivity, deflation, and weak real estate figure prominently. The 15th Five Year Plan may trumpet China’s progress in science and technology. But that isn’t the yardstick against which either China’s ability to cope with such a challenging external environment, or its capacity for change, should be judged.

George Magnus is a research associate at Oxford University’s China Center and at SOAS, and the author of Red Flags: Why Xi’s China is in Jeopardy. He is the former Chief Economist of UBS.