For the past three months, hawks have called on the Securities and Exchange Commission to end the ease with which American investors can invest in Chinese companies. They are demanding delisting, a process by which the SEC would seek to remove Chinese companies from U.S. exchanges unless the firms voluntarily decamp.

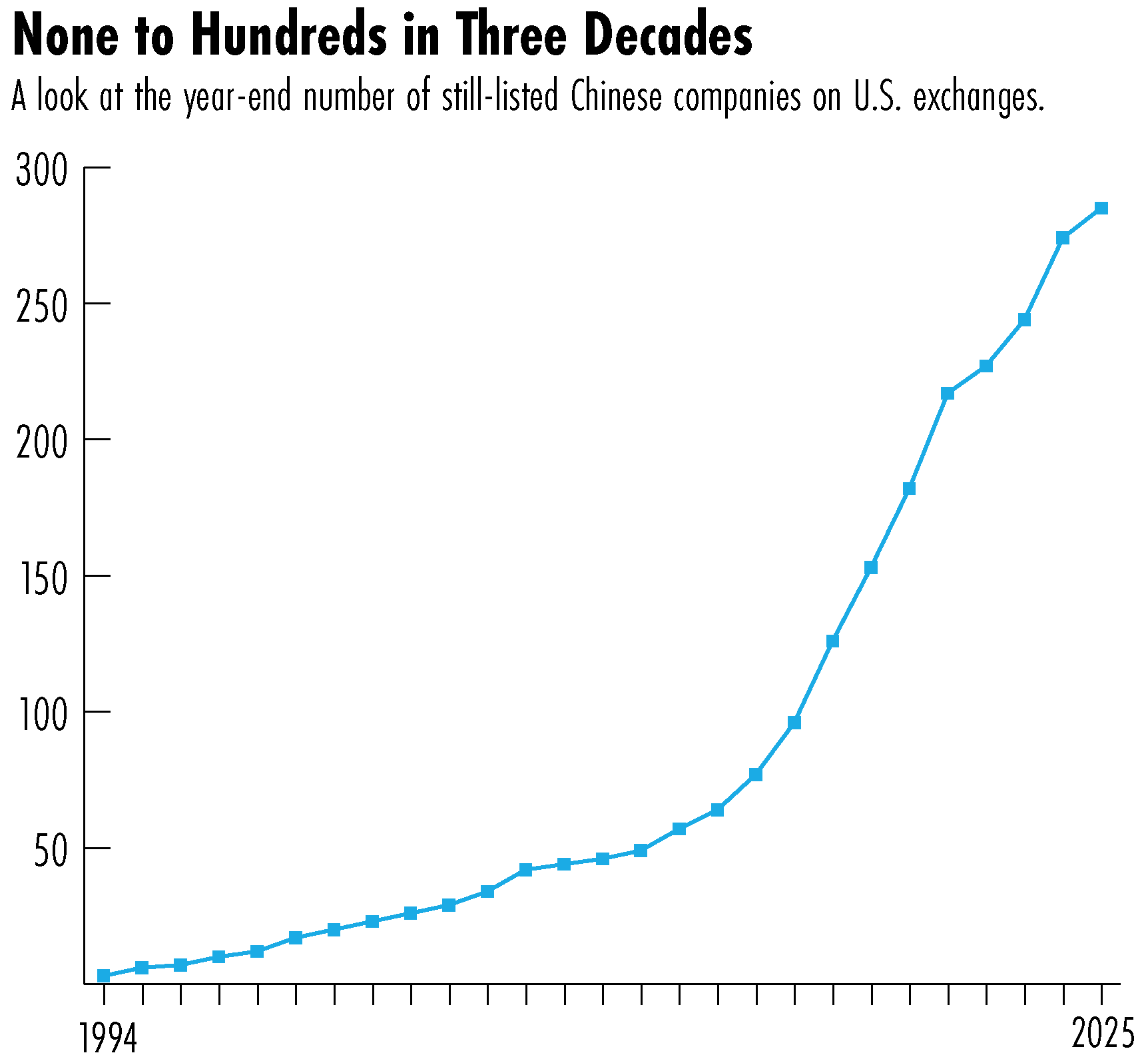

At stake are the publicly traded shares of almost 300 companies with a collective market cap north of $1 trillion.

In February President Donald Trump released a memo accusing China of “exploiting United States capital to develop and modernize its military, intelligence, and other security apparatuses.” After April’s “Liberation Day” tariffs sparked a trade war, Treasury Secretary Scott Bessent told Fox News that a forced financial exodus was an option “on the table.”

Washington and Beijing have since de-escalated their trade war, but proponents of delisting are not backing down.

On May 2, ten congressional Republicans sent a letter to newly confirmed SEC chair Paul Atkins, urging the commission to delist companies “that are inseparable from China’s military-industrial system or fundamentally incompatible with U.S. disclosure laws.” They specifically pointed to 20 Chinese firms, including Alibaba and Baidu, two of China’s biggest and most influential companies.

Less than three weeks later, Republican officials in 21 states followed with their own letter urging the SEC to investigate the delisting of Chinese issuers.

The White House, the Treasury Department, and the SEC did not respond to requests for comment.

“The delisting threat is a tool in the toolkit of negotiation,” says Eric Wong, founder of China-focused hedge fund Stillpoint Investments. “Or it could just be a rattle.”

Note: Data is as of March 7. Source: U.S.-China Economic and Security Review Commission

HONG KONG ESCAPE ROUTE

In an extreme scenario, financial decoupling between the U.S. and China could result in $800 billion of outflows that U.S. investors hold in Chinese companies, Goldman Sachs analysts estimate. (They do not view this scenario as likely.)

Chinese mainland and Hong Kong are much harder to do IPOs, so [the] U.S. market is the last and best destination for small and middle size companies.

Li Shoushang, a senior partner with law firm Dacheng in Beijing

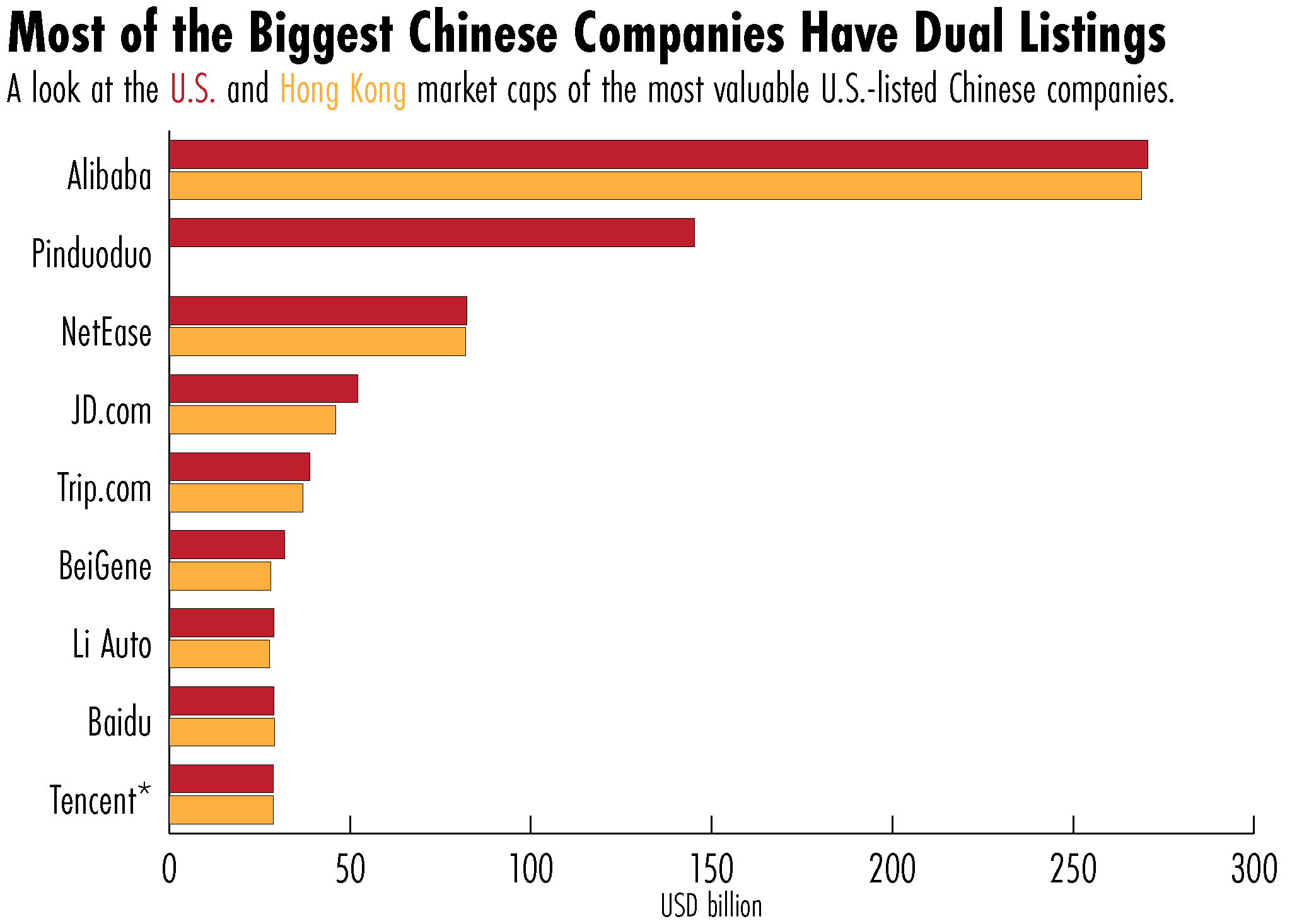

However, three-quarters of Chinese companies with U.S.-listed equities by market value have secondary listings in Hong Kong, according to Chinese brokerage Huatai Securities. If firms are kicked off Nasdaq and the New York Stock Exchange, investors’ holdings could simply be shifted to Hong Kong.

“Even if there’s delisting, you can convert [U.S. shares] to Hong Kong shares seamlessly,” says Bing Yuan, a China-focused portfolio manager at French firm Edmond de Rothschild.

Some investors are limiting their exposure to U.S.-listed Chinese stocks that don’t have backup listings in Hong Kong. “The bar has to be really high for us to own one of those,” Stillpoint’s Wong says. “I don’t want to be on the short end of that stick.”

The largest such firm by market cap is Pinduoduo, the parent of e-commerce giant Temu. The company went public on the Nasdaq in July 2018 and has seen its valuation more than quadruple to more than $140 billion in the years since. Its stock is included in indexes offered by major investment management firms like MSCI and Invesco.

Pinduoduo would be able to list in Hong Kong if it so chooses. The firm has an established track record of profits and netted $15.4 billion last year. It did not respond to a request for comment.

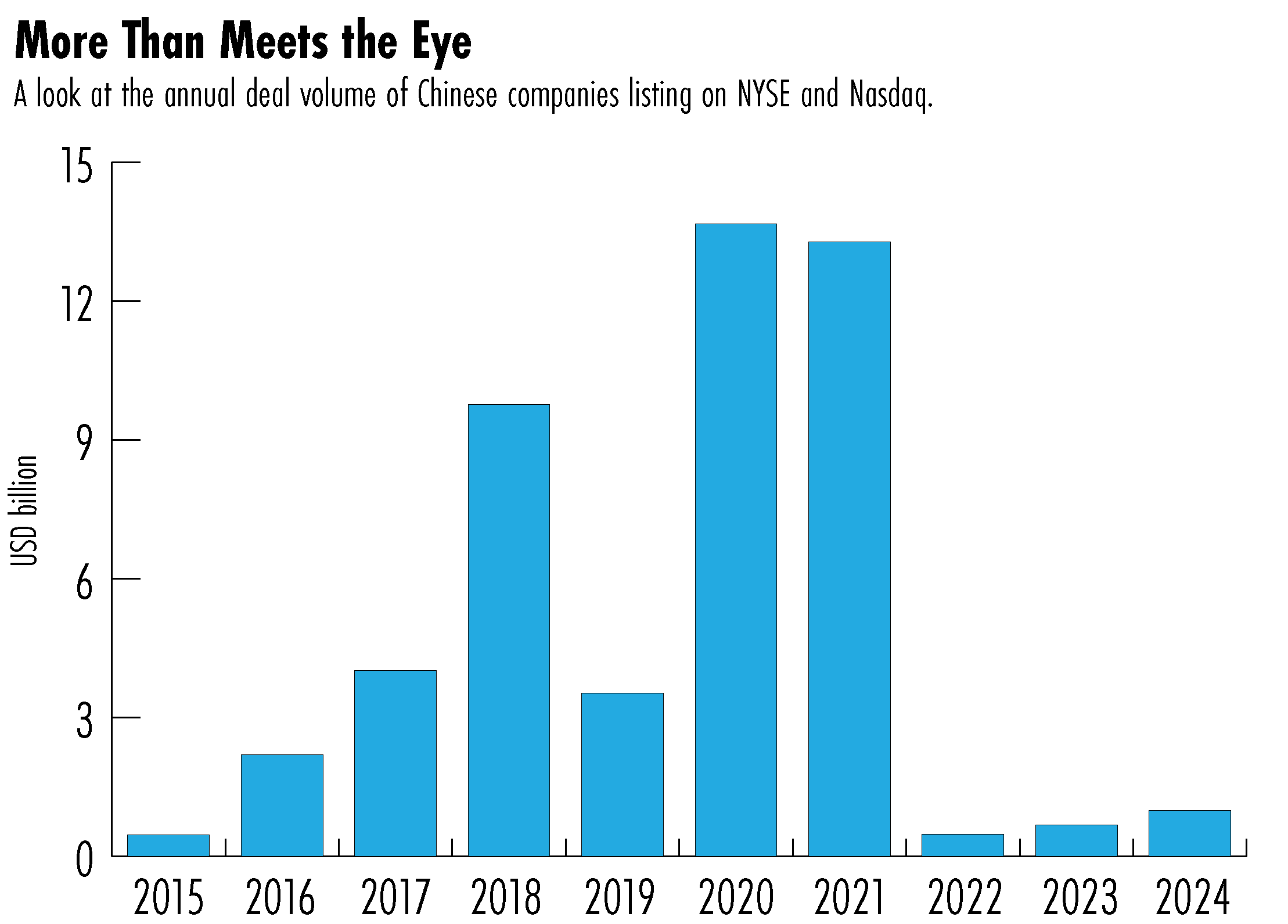

Around 170 other U.S.-listed Chinese firms are not eligible to go public in Hong Kong because they do not meet the bourse’s criteria in areas like profitability and market cap, according to Goldman. The more than 50 Chinese companies that went public in the U.S. between 2022 and 2024 raised slightly more than $2 billion, Dealogic data shows, which is less than half of what battery firm CATL raised listing in Hong Kong last month.

Li Shoushang, a senior partner with law firm Dacheng in Beijing, says companies he advises are still preparing to list in New York. “Chinese mainland and Hong Kong are much harder to do IPOs, so [the] U.S. market is the last and best destination for small and middle size companies.”

But if smaller firms cannot relist elsewhere, their American investors have more to lose if they face delisting in the U.S.. In such a scenario, they may end up going private on terms that are unfavorable to U.S. investors, says Jesse Fried, a professor at Harvard Law School who has studied Chinese firms listed in the U.S.. “American retail investors will get hammered.”

Jeremy Schwartz, Global Chief Investment Officer at exchange-traded fund sponsor WisdomTree, says his firm has been hedging by putting money directly into A-shares, or stocks listed on mainland exchanges. But what if Trump prevents U.S. firms from putting money in the Chinese market altogether? “That’s an existential risk,” he says.

Other ETF providers are entirely excluding China from their emerging markets funds. Last month, Vanguard filed with the SEC to create an ex-China emerging markets ETF.

BRILLIANT BEGINNINGS

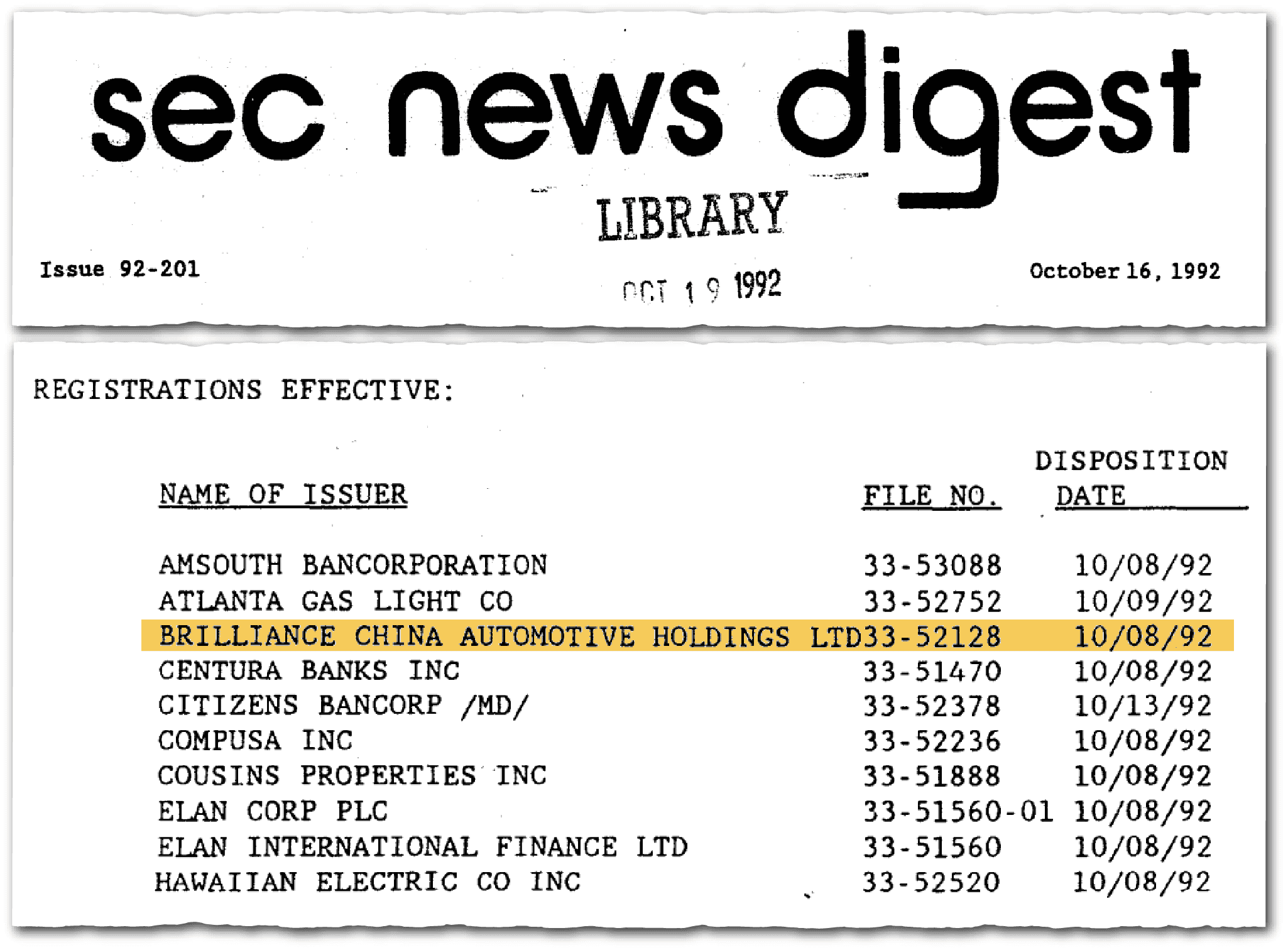

Hong Kong was not always the best option for Chinese companies seeking foreign cash. In 1992, state-owned Chinese van manufacturer Brilliance Automotive looked instead to the U.S. and went public on the New York Stock Exchange that October. It became the first Chinese company listed in the United States.

In China, the deal was a national priority. The Shanghai stock exchange, newly reopened after a four-decade hiatus, was hardly a consideration.

At that time Sheldon Kasowitz, then an equity research analyst at Hong Kong-based Jardine Fleming, often visited Chinese companies. He remembers meeting executives who wore ill-fitting Western suits with designer labels resewn on the outside. “Very clearly the bankers had taken the management shopping,” he says.

With their home market not an option, Chinese central bank officials tracked down Clark Randt, a former commercial attache at the U.S. embassy in Beijing who had become a partner at law firm Gibson Dunn in Hong Kong. “They had gotten my name from colleagues and knew I was an American lawyer who spoke Chinese,” says Randt, who went on to become U.S. ambassador to China during President George W. Bush’s administration. “They came to my office in Hong Kong and said they wanted to learn about the U.S. stock market by listing a restructured Chinese company on the NYSE.”

Randt called Lee Spencer, a former SEC lawyer who had joined Gibson Dunn in New York, and the duo began talking to Brilliance Automotive. After visits to the company’s base in Shenyang and some 11,000 hours of accounting work, the company’s prospectus was ready to file to the U.S. securities regulator. “We did it by the book,” Spencer says. “We didn’t ask for any favors.”

In October 1992 Brilliance Automotive began trading on Wall Street, raising $80 million in its IPO. By late November, its share price had more than doubled to nearly $33 per share from its initial offering price of $16.

The offering was so well received in Beijing that Randt, Spencer, and the bankers and accountants who led the deal were invited to a state dinner. The next day, they met Party General Secretary Jiang Zemin, who became president a few months later. “We were feted,” Spencer says.

You don’t have to have a view on how good it is for [U.S. investors] to invest in [Chinese companies] to say we should make this straightforward equity. Everybody has an interest to make this [VIE structure] better and more efficient. If you say it is equity, let’s just [make it] equity.

Matteo Maggiori, a finance professor at Stanford University

Brilliance Automotive would go on to advise a wave of Chinese companies seeking to follow its model, including many state-owned enterprises. And follow they did, attracted by the deep pool of capital and relatively lenient listing requirements that have made New York a global financial hub for the past century.

Hong Kong, which is now a common destination for Chinese IPOs, had far stricter listing requirements, including strict rules on voting rights and profitability that kept out many newer companies. “Long story short, Hong Kong wasn’t ready,” says Eliot Fisk, a former JPMorgan investment banker in the city.

But by 1999 Brilliance Automotive was ready for Hong Kong. In October of that year, it listed on the city’s exchange, again trailblazing a model by which Chinese companies would list first in New York and then in Hong Kong. (The company took it one step further, also listing in Frankfurt. It delisted from the New York Stock Exchange in 2007 amid a decline in trading volume.)

THE VIE LOOPHOLE

By the late 1990s Chinese companies looking to list in the U.S. faced more barriers in Beijing than in Washington. Chinese regulators restricted foreign investment in local firms, particularly those in sensitive sectors.

In 2000, the Chinese internet start-up Sina found a way through the barrier. It set up an offshore company in the Cayman Islands that had contractual ties to a mainland entity. The offshore company listed on the Nasdaq and signed contracts through which it claimed the rights to the mainland firm’s profits. At the time Matt Pottinger, then a Reuters reporter who would later become deputy national security adviser during the first Trump administration, wrote that Sina was “performing corporate backflips” to demonstrate the strength of its contracts.

The structure became known as a “variable interest entity.” After Chinese authorities let Sina’s VIE deal proceed, other Chinese companies quickly followed suit. In the five years after Sina pioneered the structure, more than a dozen other Chinese companies used it to list in the U.S..

Experts on offshore finance have long viewed VIE structures as risky, particularly for retail investors and pension funds who may not realize that their holdings depend on the untested enforceability of complex contracts.

“They were clearly engineered on one end to fulfill a seeming miracle of formally stating to Chinese regulators that none of this is equity,” says Matteo Maggiori, a finance professor at Stanford University. “And at the other end, under accepted international accounting principles, saying that because the contracts amount to the key characteristics of equity — control and the residual claims to the profit — they should be regarded as being equity.”

“This clearly was a gimmick to begin with,” he adds. “This is an accident waiting to happen.”

More than half of Chinese companies currently listed in the U.S. still use VIE structures, including giants such as Alibaba and Baidu.

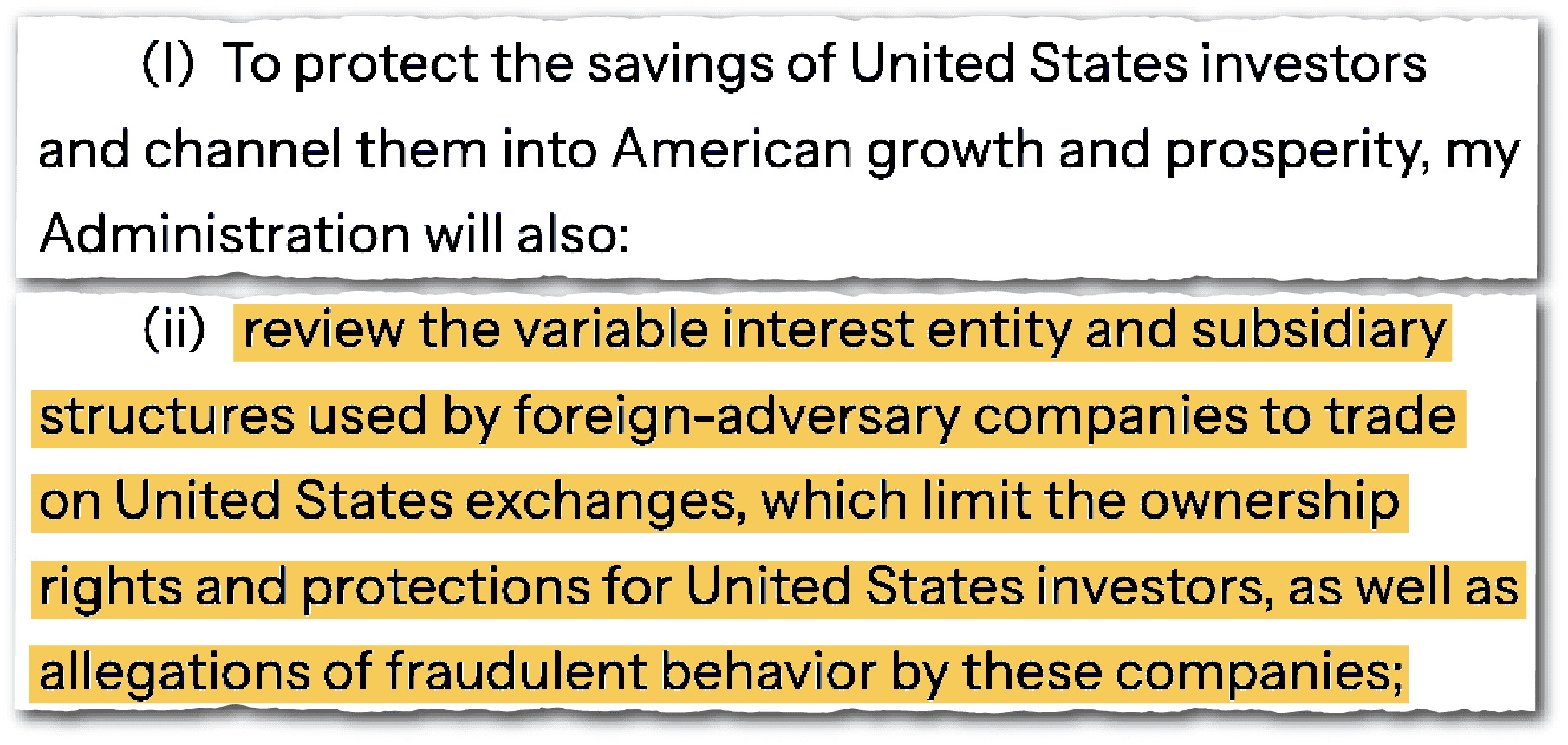

These arrangements are now in Trump’s crosshairs. In his February memo, Trump specifically ordered federal agencies to review the “variable interest entity and subsidiary structures used by foreign-adversary companies to trade on United States exchanges.”

Trump’s scrutiny of Chinese firms’ U.S. listings is not new, however. In November 2020, he signed an executive order prohibiting U.S. investment in 31 “Chinese military companies,” a step that resulted in the forced delisting of China Telecom, China Unicom and China Mobile.

The month before his firm term came to an end, Trump signed the Holding Foreign Companies Accountable Act, which required foreign companies listed in the U.S. to allow the Public Company Accounting Oversight Board (PCAOB), an independent federal agency under the SEC, access to their auditors — or else face delisting.

The 2002 legislation known as Sarbanes-Oxley created the PCAOB to ensure auditing oversight for all U.S.-listed companies. But experts say China, whose laws restrict the sharing of audit documents if deemed necessary for national security, never allowed the watchdog sufficient access to records for U.S.-listed companies.

The HFCAA brought the issue to the fore, setting off a two-year battle between U.S. and Chinese officials. It ended with a detente in December 2022, when the PCAOB announced that it had secured “complete access” to Chinese firms “for the first time in history” — but not before many state-owned enterprises, including oil major Sinopec and insurer China Life, voluntarily delisted. China Eastern Airlines and China Southern Airlines, the last two state-owned enterprises still on U.S. exchanges, delisted in 2023.

Chinese regulators too put pressure on mainland companies with U.S. listings, resulting in the high-profile departure of rideshare firm DiDi from the NYSE in June 2022.

Trump has signaled that he could yet break the auditing truce. His February memo said the administration would “determine if adequate financial auditing standards are upheld for companies covered by [HFCAA].” At the same time, a Republican bill working its way through Congress is threatening to dismantle the PCAOB and delegate its authority to the SEC.

Investors are now better prepared for delisting disruption, however. The tensions sparked by the HFCAA acted as a test-run for the current round of delisting threats. Rothschild’s Yuan says she didn’t have to make major adjustments to her portfolio during recent delisting threats because she had already addressed the risk over the previous five years.

Trump’s preferred path towards forced delistings, should he choose to pursue them, is unclear. Goldman analysts reckon there are four ways Chinese stocks in the U.S. could be delisted:

- U.S. sanction, such as an executive order that bans trading outright

- Non-compliance with the HFCAA

- Accusations of accounting fraud

- Violation of Chinese regulations

Trump would have control over the first three. Each potential choice would have different implications for investors. For example Americans cannot trade shares in China Mobile, which Trump exiled citing national security concerns, but they can still buy and sell shares over-the-counter in firms that have been delisted following allegations of fraud, such as Luckin Coffee.

Then there’s the issue of VIEs. Both the U.S. and China tacitly acknowledge VIEs function like equity, so formally recognizing them could reduce risks for retail investors while building goodwill for trade negotiations. “You don’t have to have a view on how good it is for [U.S. investors] to invest in [Chinese companies] to say we should make this straightforward equity,” Stanford’s Maggiori says. “Everybody has an interest to make this [structure] better and more efficient. If you say it is equity, let’s just [make it] equity.”

Noah Berman is a staff writer for The Wire based in New York. He previously wrote about economics and technology at the Council on Foreign Relations. His work has appeared in the Boston Globe and PBS News. He graduated from Georgetown University.