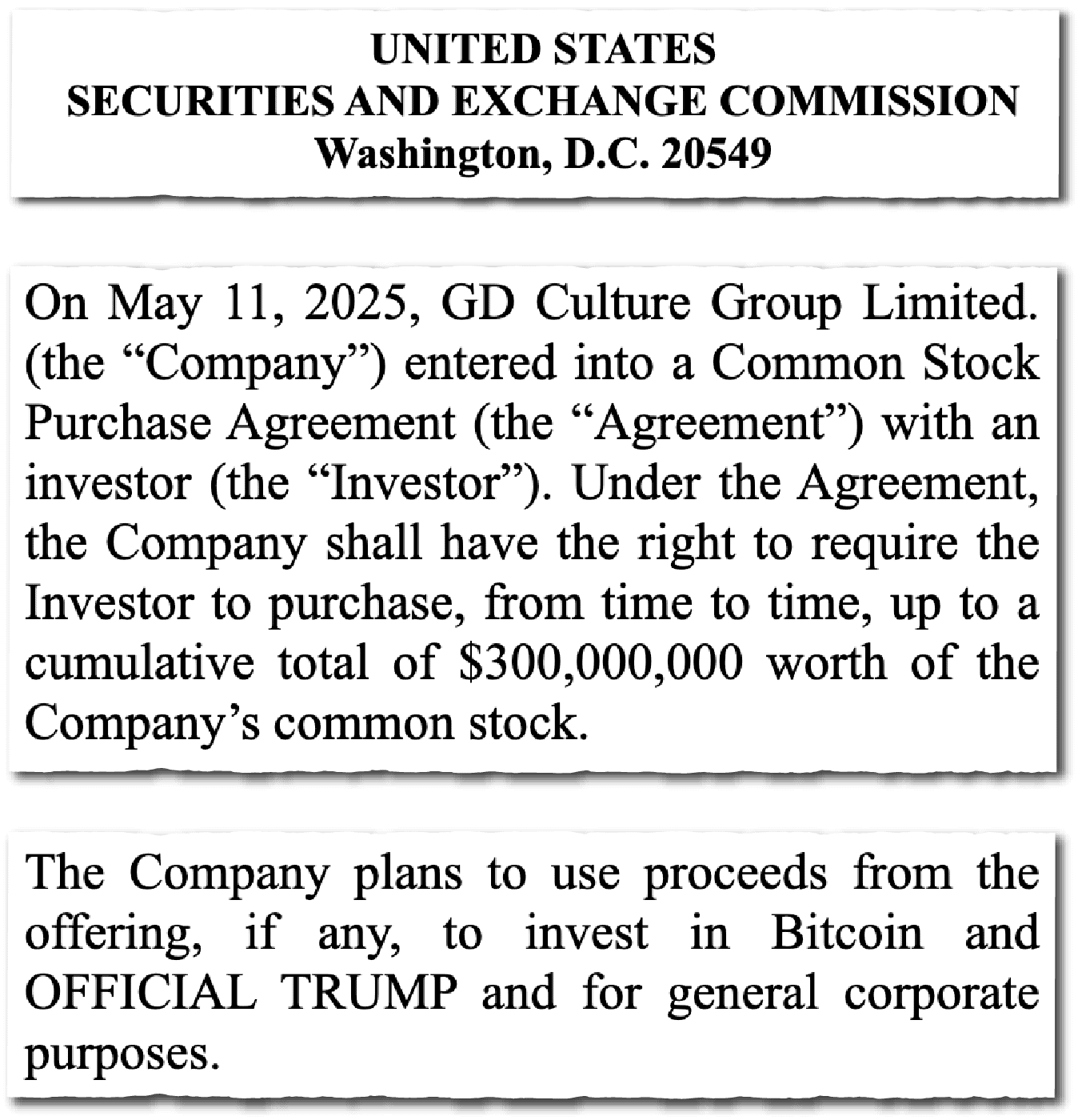

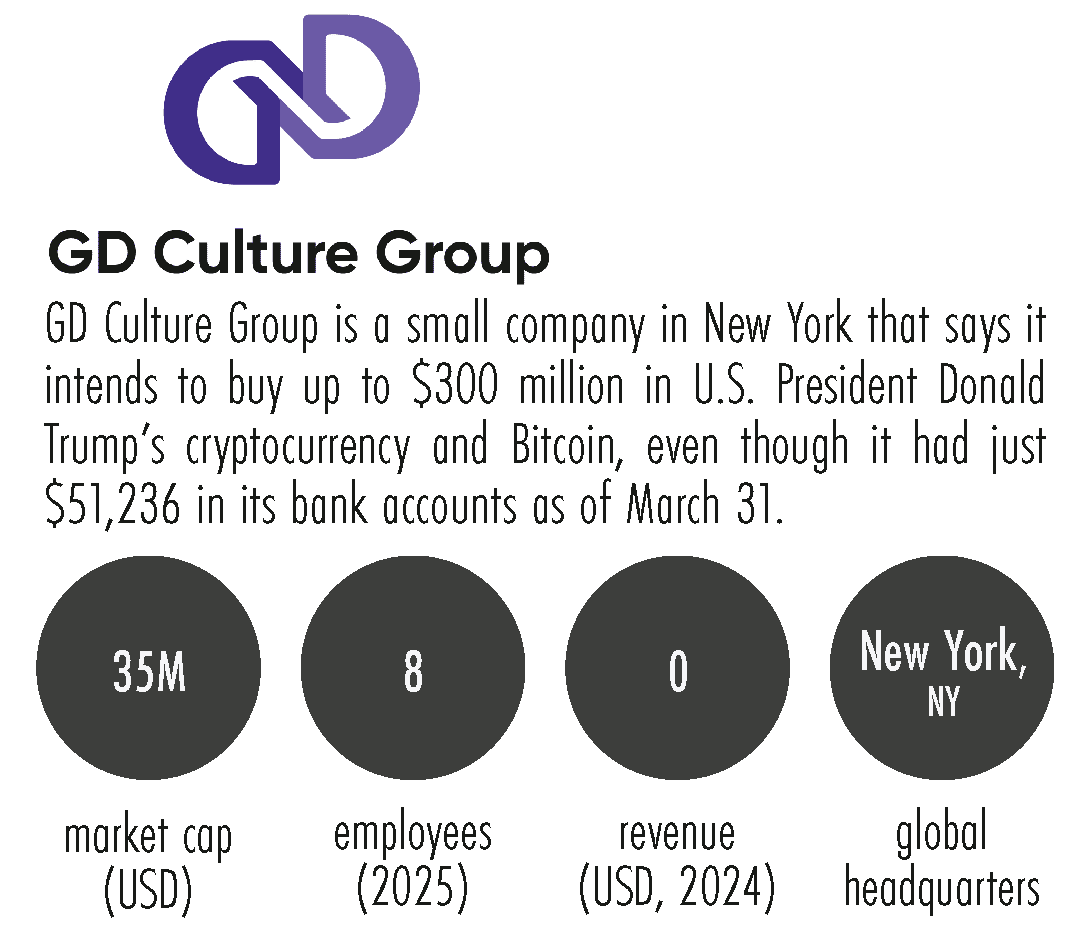

When an unknown company that creates AI avatars for TikTok users said it would raise hundreds of millions of dollars to invest in President Donald Trump’s cryptocurrency and Bitcoin last week, it raised plenty of questions.

The identity of the investor set to plow up to $300 million into New York-based GD Culture Group remains unknown: The company has said only that it is raising the money from a British Virgin Islands entity. But through a review of corporate records and U.S. filings, The Wire has traced GD Culture’s extensive links to China, including to an entrepreneur with connections to Chinese elites and an affinity for blockchain.

It’s not the first time people or entities linked to China have moved to buy Trump’s cryptocurrencies, even as the president moves to shut many Chinese firms out of the U.S. market with tariffs.

In February, the Securities and Exchange Commission paused a suit against Chinese national Justin Sun over alleged market manipulation, after he said he bought $75 million worth of a cryptocurrency backed by Trump’s family. Sun announced on Tuesday that he is also the largest holder of the memecoin $TRUMP, a title that has won him and the next top 219 buyers dinner with the president. GD Culture Group is also seeking to buy $TRUMP.

Three days after GD Culture Group announced its planned purchase, another Chinese company, Addentax Group, announced that it too would buy up to $800 million in $TRUMP and Bitcoin.

White House spokesperson Anna Kelly said in an email to The Wire that Trump’s assets are in a trust managed by his children. “The President is working to secure GOOD deals for the American people, not for himself…There are no conflicts of interest,” she said.

The Trump Organization, which is led by Trump’s sons Eric and Donald Jr., did not respond to a request for comment.

CHINA TIES

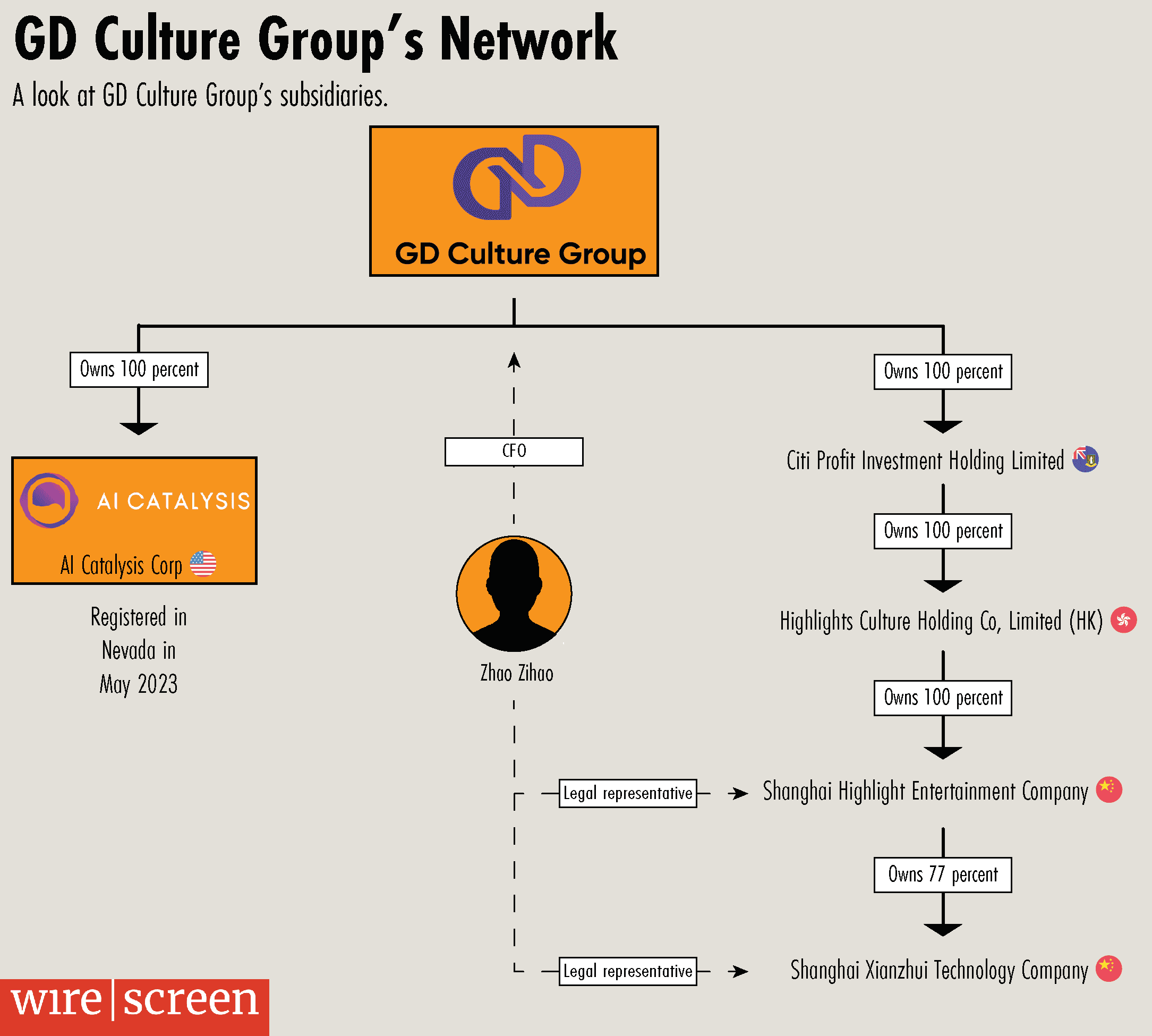

In its filings, GD Culture Group explains that it controls a subsidiary in Shanghai, via its own subsidiary in the British Virgin Islands — a common destination for offshore finance. The New York Times first reported those links.

But GD Culture Group is itself the product of several business combinations involving Chinese firms.

Too many SPACs went public all at the same time, chasing too few companies, and a lot of dodgy companies went public in the process.

Jim Angel, a professor of financial regulation at Georgetown University

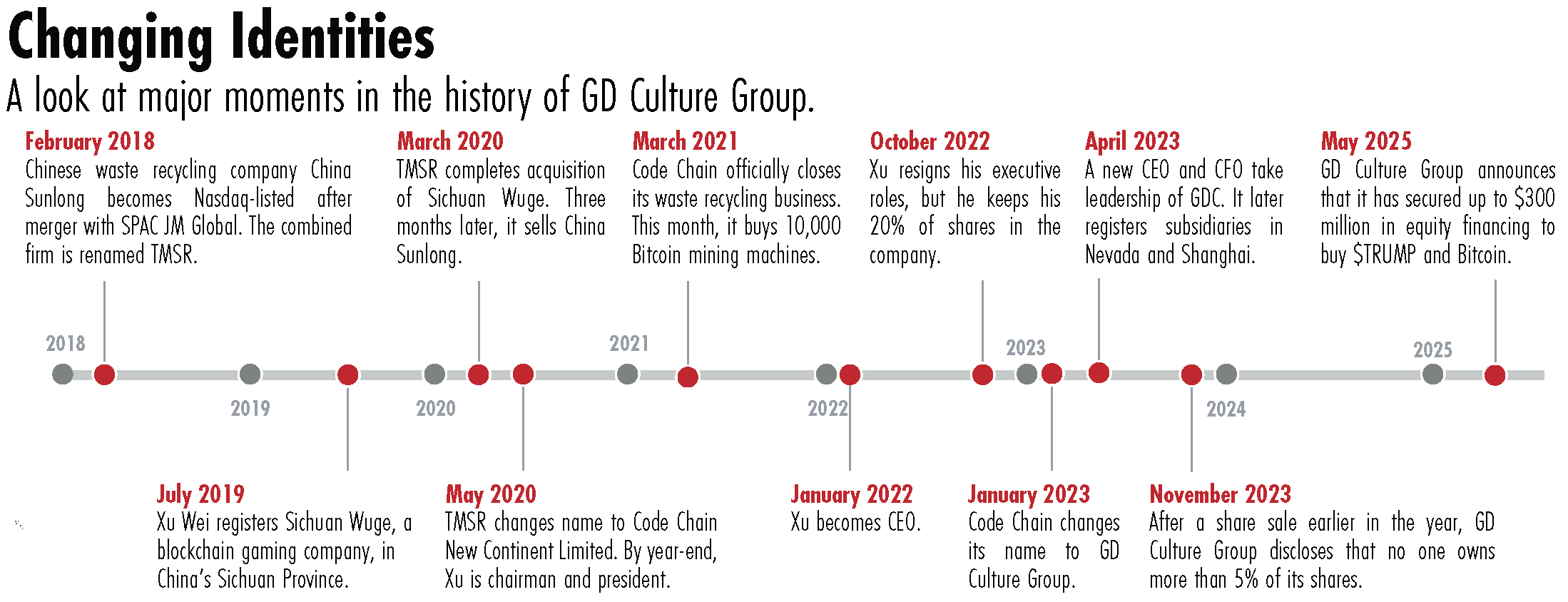

In 2018, a Chinese waste recycling company called China Sunlong merged with a Nasdaq-listed special purpose acquisition company (SPAC) called JM Global, forming a new entity called TMSR. By 2020, the TMSR entity had expanded again, acquiring a Chinese company called Sichuan Wuge Network Games Co, which coded videogames using blockchain technology.

The latter acquisition — aimed at diversification, according to the company — brought TMSR into the world of Xu Wei, a well-connected Chinese entrepreneur and blockchain enthusiast who had founded Sichuan Wuge in 2019. In February 2020, Xu became co-chairman of the newly combined entity and changed its focus from waste recycling to blockchain gaming. Three months later, the company again changed its name to Code Chain New Continent Limited — matching several companies Xu owned in China with a “Code” nom de guerre, according to a review of his holdings in WireScreen.

Code Chain’s ascent to the Nasdaq came amid a peak in so-called reverse mergers between publicly listed SPACs and private companies. “Too many SPACs went public all at the same time, chasing too few companies, and a lot of dodgy companies went public in the process,” says Jim Angel, a professor of financial regulation at Georgetown University.

By year end in 2020, Xu was chairman and president of the still Nasdaq-listed Code Chain New Continent, a role for which he received just $10,000 in annual compensation, according to an SEC filing. The next year, Code Chain doubled down on crypto, announcing that it had bought 10,000 Bitcoin mining machines.

PATENT PLAYER

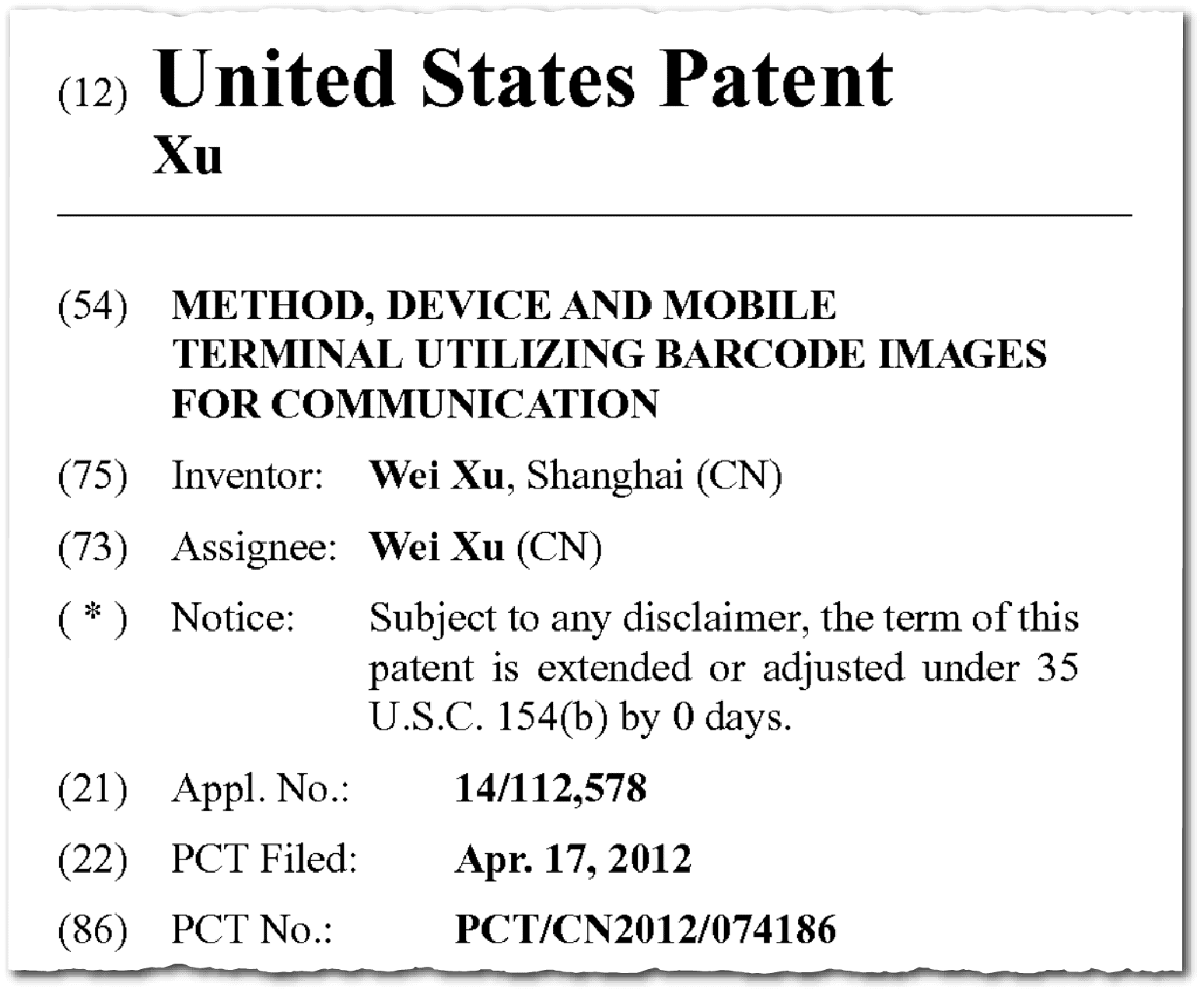

Xu had spent the previous half-decade attempting to enforce patents on scan-to-pay QR codes — a payment method that had grown ubiquitous in China with the rise of platforms like Alibaba’s Alipay. Since 2015, Xu has held a U.S. patent for a “method and a device utilizing barcode images to communicate between a mobile terminal and a backend server.” He obtained a similar patent in China the same year — even though a Japanese engineer named Masahiro Hara had invented QR codes themselves in 1994. (Hara’s company, Denso Wave, made the patent freely available.)

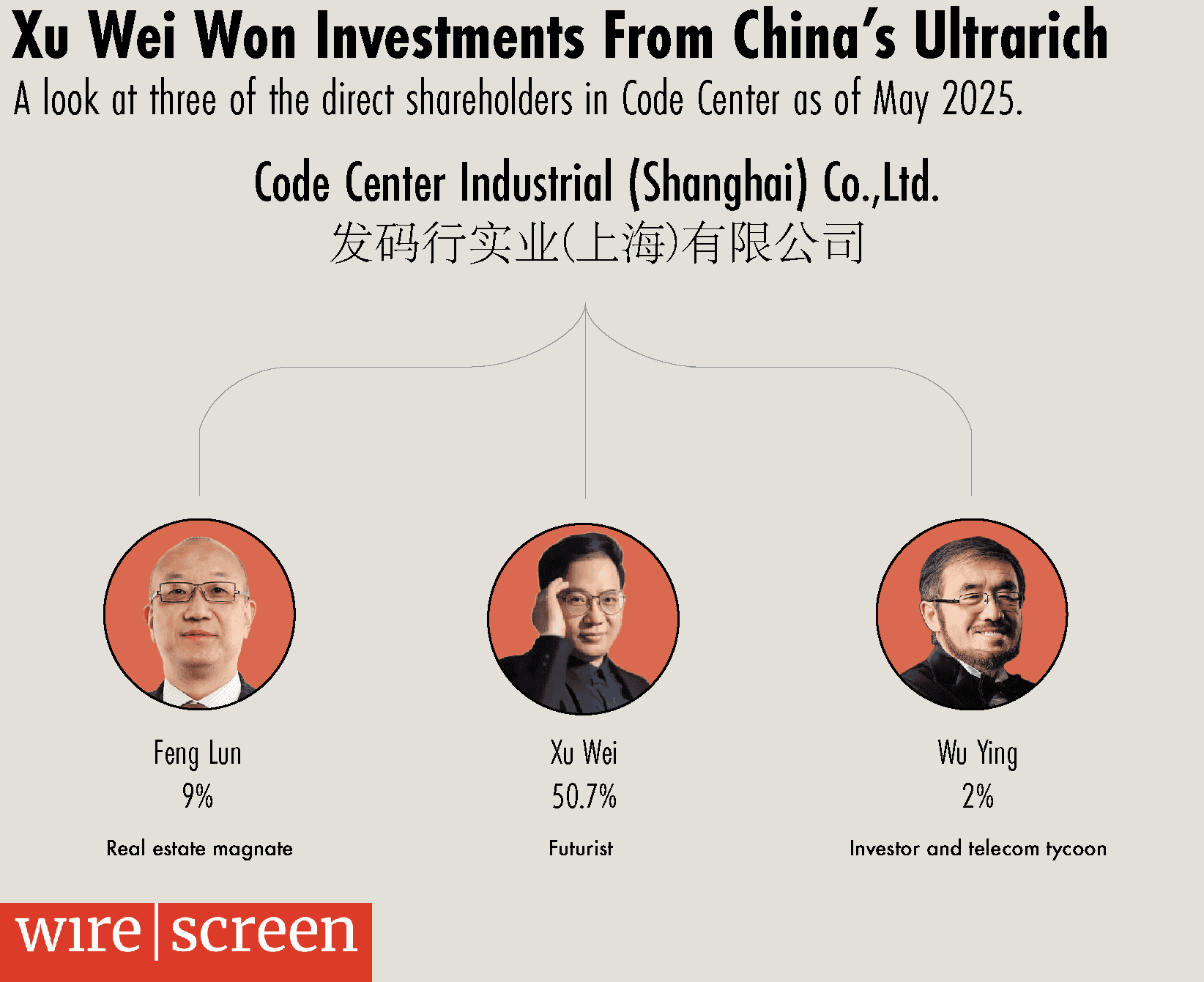

The scheme proved lucrative. In 2017, Chinese media speculated that overseas licensing fees for Xu’s patents could bring in as much as $100 million. A company he set up that year, called Fāmǎxíng, or Code Center, won direct investments from some of China’s wealthiest men. Feng Lun, the founder of real estate group Vantone, and Wu Ying, the co-founder of telecom firm UTStarcom, each sat on the board, according to corporate records accessed through WireScreen.

In an email to The Wire, Wu denied owning shares in Code Center. “I quit that company long ago,” he said, without specifying when. Feng could not be reached for comment.

Over time, Xu became more assertive with enforcement, earning critics that accused him of patenting technology without an underlying business purpose. In 2020, he sued Apple and Alibaba’s Alipay unit for patent infringement, according to an interview he gave a Chinese finance magazine that year. Another company he sued, Shanghai Rongtai Health Technology, reportedly said in court that Code Center’s “business model is only to profit from patents.”

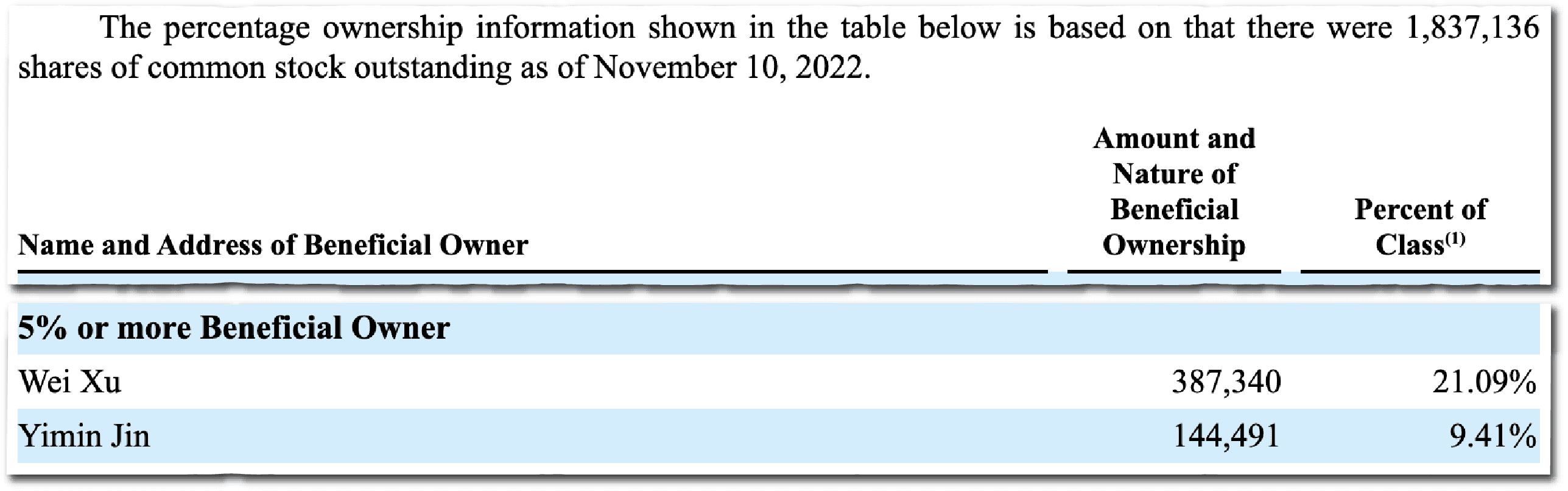

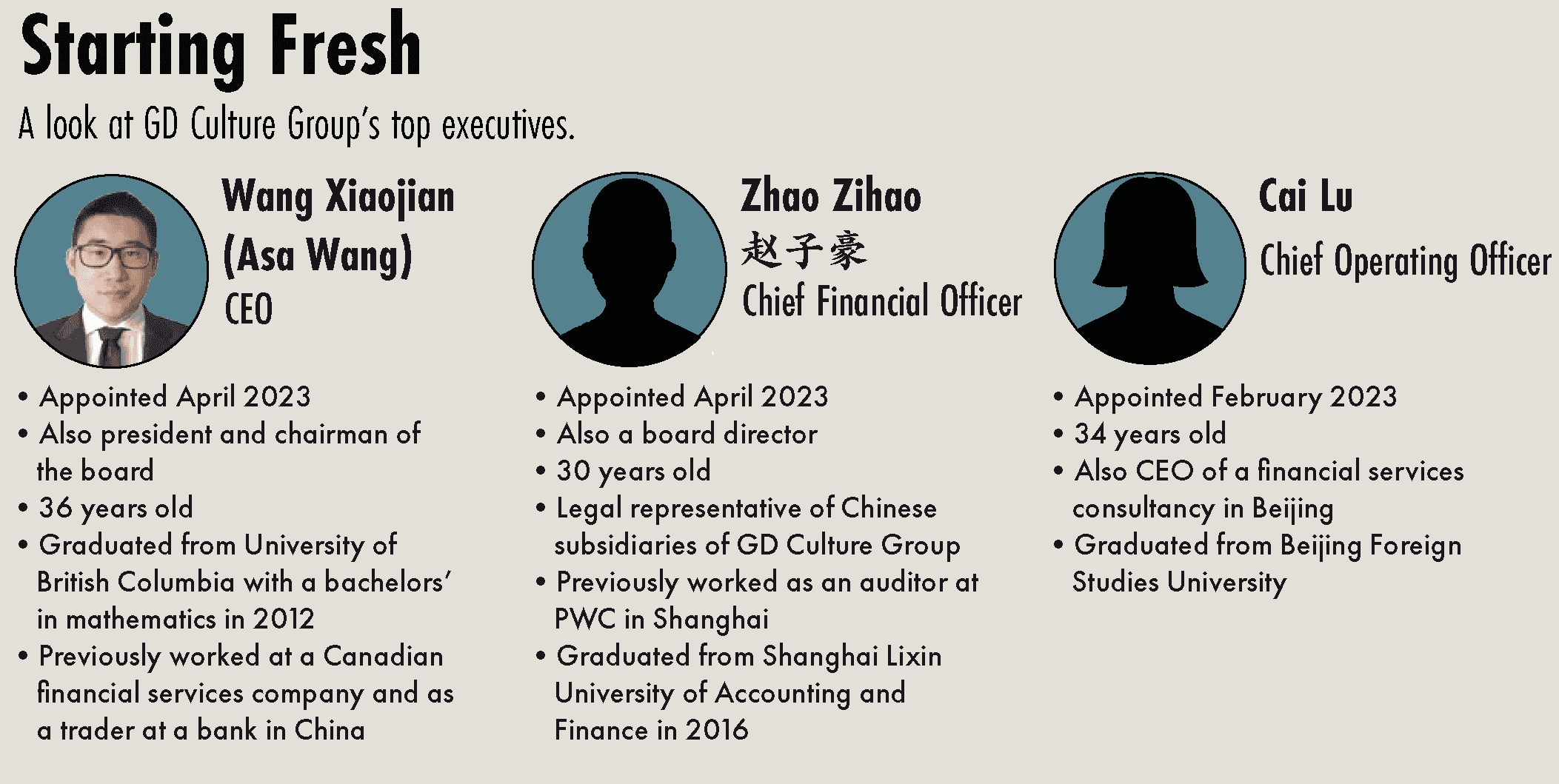

Two years later, Xu’s tenure at Nasdaq-listed Code Chain came to an abrupt end. He resigned from his positions at the firm in October 2022, having become CEO earlier that year. The following January, the firm changed its name to GD Culture Group, ending the Xu era — except that he remained the company’s largest shareholder, with more than 20 percent of its shares.

A new chief executive and board soon took over in the spring, and promptly announced a share sale that diluted Xu’s ownership. In November 2023, GD Culture Group disclosed that no shareholder owned more than 5 percent of its outstanding stock, according to an SEC filing. However, Bloomberg data shows that as of the end of 2024, Xu was still the company’s largest individual shareholder. The Wire could not independently determine the status of Xu’s shareholdings.

GD CULTURE’S SWITCH

Under fresh leadership — and with $400,000 in zero-interest loans from its new CEO — GD Culture Group has pivoted toward TikTok. The company plans to make money by creating customizable AI avatars for livestreamers on the platform. Examples of AI avatars on the firm’s website include a white man narrating a video about why pets are better than siblings and an Asian woman describing the lineup at the Coachella music festival.

‘Jenny’, an ‘AI-driven virtual digital human’, created by AI Catalysis. Credit: AI Catalysis

In its most recent quarterly report, the company says that it conducts business through the Nevada-based AI Catalysis and the China-based Shanghai Xianzhui. The efforts are yet to bear much fruit, with the company recording a $14 million loss last year. Meanwhile, it drew scrutiny from Nasdaq in March for failing to retain the minimum $2.5 million in shareholders’ equity. The company has not said if it is back in the exchange’s good graces.

GD Culture Group did not respond to requests for comment, nor did its CEO. A security guard at the midtown Manhattan building where GD Culture Group is based stopped The Wire from going up to its corporate office. An attorney at a law firm that has worked with the company, Ortoli Rosenstadt LLP, declined to comment.

The Wire was unable to reach Xu for comment. An unconfirmed Chinese media report from last week says he has been detained in Xinxiang County since 2022.

At a golf course in the DC suburbs, meanwhile, Sun and 219 other buyers of $TRUMP are set to meet President Trump for dinner on Thursday. If GD Culture Group purchases as much of the cryptocurrency as it says it plans to, the company will be there for the rerun.

Noah Berman is a staff writer for The Wire based in New York. He previously wrote about economics and technology at the Council on Foreign Relations. His work has appeared in the Boston Globe and PBS News. He graduated from Georgetown University.