While President Trump has ratcheted up tariffs on Chinese goods to 145 percent this year, Xi Jinping has been trying both to reconcile with the business community at home and to send a message overseas that China can be taken seriously as a supporter of free trade and open markets.

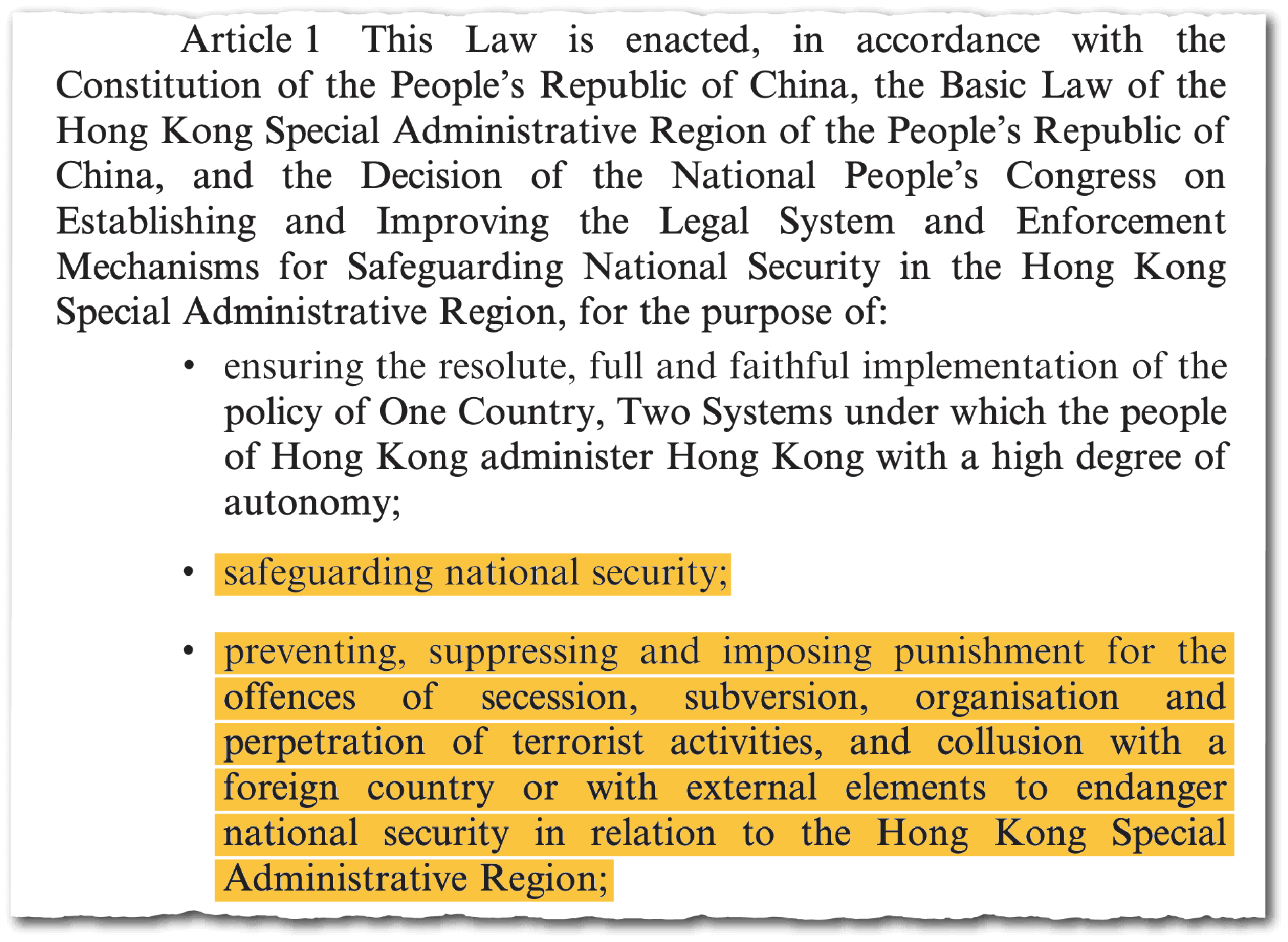

It is hardly a good time, then, for a row over whether Beijing is threatening the independence of companies based in Hong Kong.

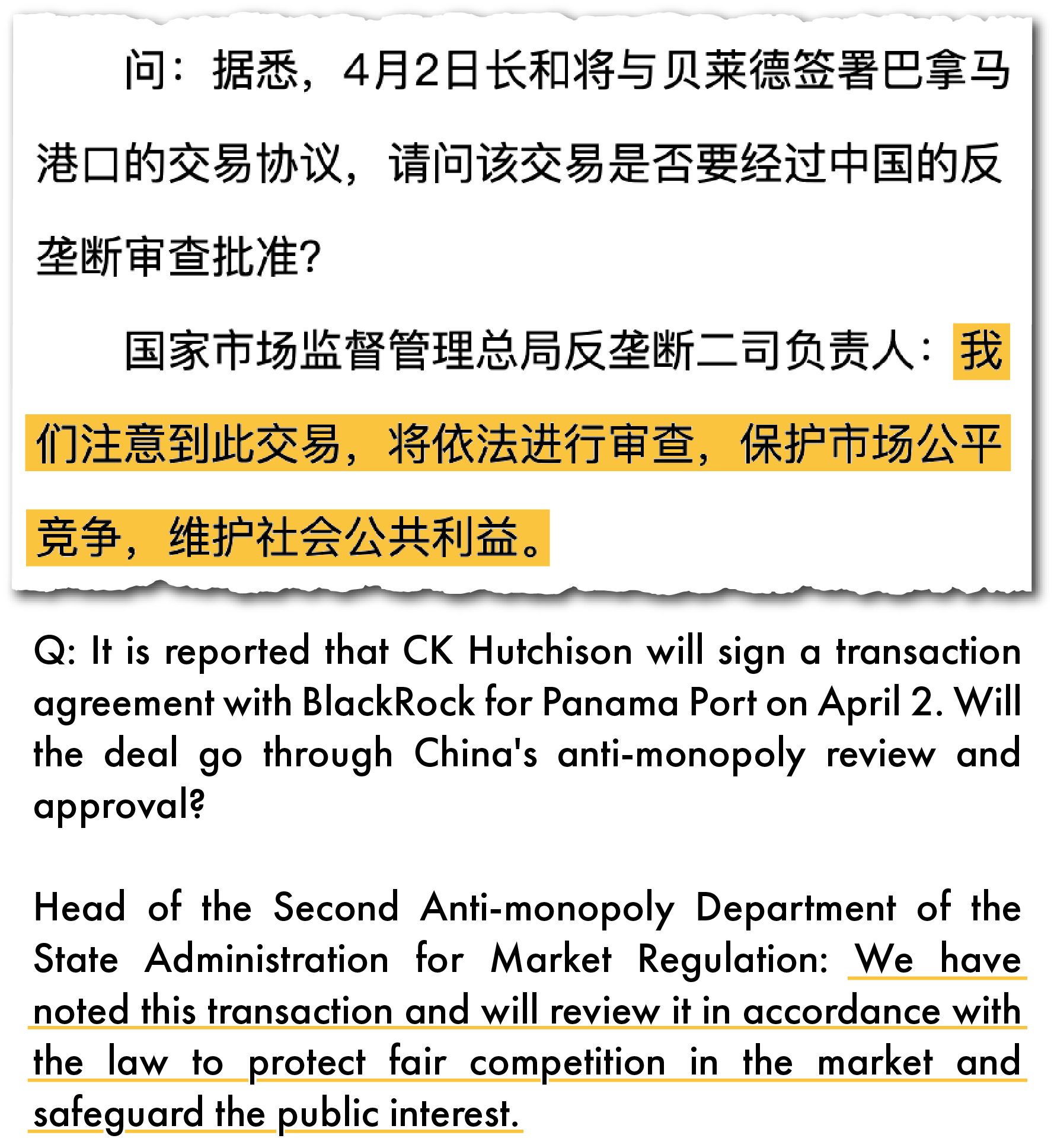

Yet, rumors now abound that Chinese regulators may be planning to utilize the national security regime to threaten industrial conglomerate CK Hutchison into reconsidering the sale of 45 ports to U.S. fund management giant BlackRock for $22.8 billion. That would confirm what many have long suspected — that Hong Kong companies can no longer boast autonomy from the Chinese Communist Party.

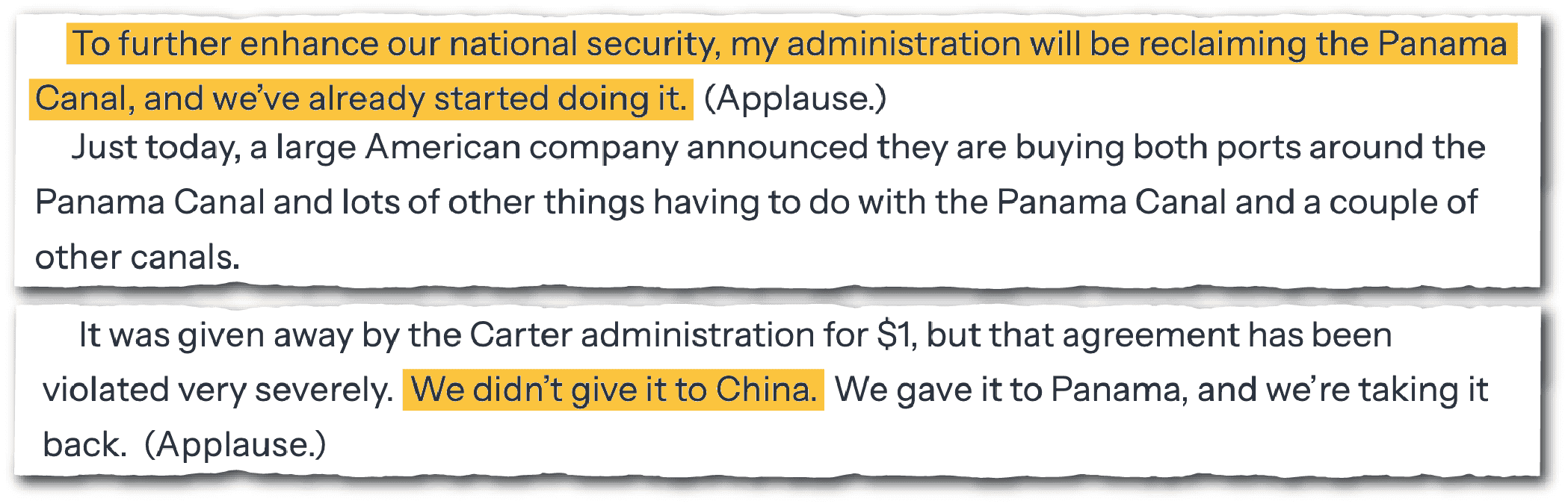

The ports CK Hutchison owns and operates on the Panama Canal drew the early ire of the Trump administration, with the president claiming in his recent address to Congress that its ownership in effect means that the PRC controls the vital trade passage.

The sale quickly negotiated with BlackRock, which included an exemption for CK Hutchison’s port holdings in Hong Kong and China, was widely seen as a straightforward resolution of the matter. Some analysts even speculated that this agreement had the blessing of Xi Jinping, and might serve as a precursor to a potential meeting between the U.S. and China to resolve their trade tensions.

In recent weeks the deal has instead appeared to unravel, as Chinese and Hong Kong regulators have sought to review it. Hong Kong lawmakers and pro-Beijing media outlets have also sought to publicly pressure the company and its chairman Li-Ka Shing to reconsider the sale by floating possible violations of the National Security Law (NSL), the Safeguarding National Security Ordinance (SNSO), or the PRC’s Anti-Monopoly Law. In a rare move, the official website of the PRC’s Hong Kong Macau Affairs Office shared multiple articles attacking the CK Hutchison port deal as unpatriotic, stopping just short of outright criticism from Beijing itself.

Similarly, the authorities in Panama have opened their own audit of the agreement, citing irregularities. Despite this, the U.S. and Panama have signed a security cooperation agreement which includes not charging U.S. warships to pass through the Panama Canal.

The ire of regulators and the loss of face for Xi Jinping and Hong Kong Chief Executive John Lee if they let the deal proceed would pale in comparison to the greater risk if the PRC insists on marshalling the NSL or the Anti-Monopoly Law to punish CK Hutchison.

The problem for Beijing is that while CK Hutchison’s executives, headquarters, and primary stock market listing is in Hong Kong, the company is registered in the Cayman Islands, while most of its business is outside of China — including significant investments in infrastructure, retail, telecommunications, financial products, and ports in several overseas countries.

Moreover, CK Hutchison’s ports arm has historically accounted for less a tenth of its annual revenue — which may explain why Li-Ka Shing, Hong Kong’s richest man, is happy to settle for a payday from BlackRock and an opportunity to remove his company from Trump’s firing line.

For these reasons, CK Hutchison has long argued that it is a multinational business first, and a Hong Kong business second. This perceived autonomy from Beijing is the reason why historically it has been treated separately from PRC-based companies when it comes to most other countries’ investment screening regimes, enabling it to invest in critical infrastructure in over 50 countries across the world.

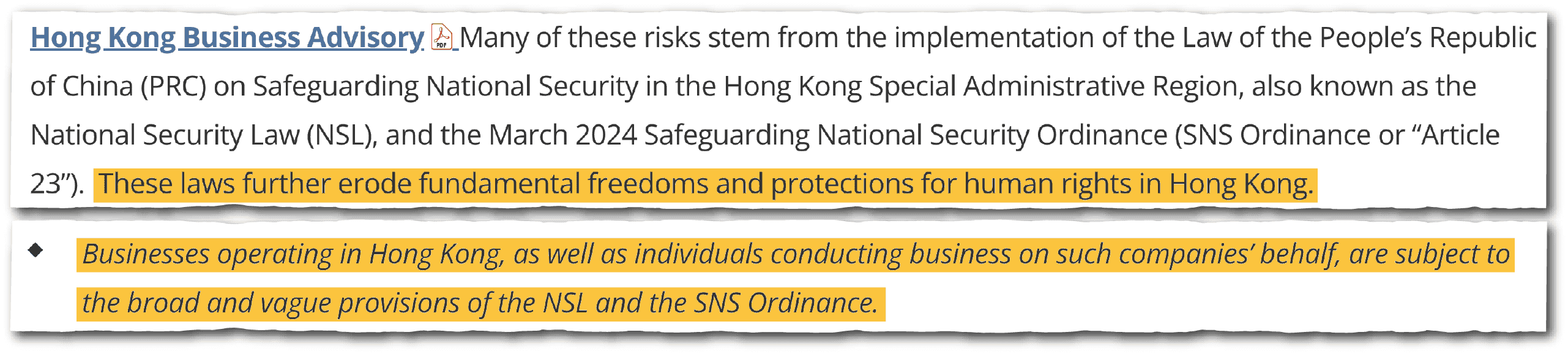

The imposition of the NSL in Hong Kong in July 2020, the jailing of pro-democracy figures such as Jimmy Lai and Joshua Wong, and the introduction last year of the SNSO have already led to increasing skepticism amongst Western countries about the independence of Hong Kong companies like CK Hutchison. The U.S. updated its business advisory guidance in September 2024 to highlight businesses operating in Hong Kong are subject to the ‘broad and vague provisions of the NSL and the SNS Ordinance’.

Despite this skepticism, international investors and countries that remain heavily reliant on Hong Kong as a profits centre and a source of foreign direct investment have been inclined to continue considering the city as being separate from the PRC. For the most part this is because there has not been a smoking gun incident to signify that the CCP leadership is able to interfere with and control Hong Kong companies in the same way that it can with mainland Chinese state-owned enterprises, or even the likes of Chinese technology companies like Huawei or TikTok-owner ByteDance.

Any public intervention by Beijing to directly block CK Hutchison’s sale of its ports arm through the direct targeting of its executives, or the raiding of its offices in Hong Kong, would offer a clear signal that this is no longer true. Nor can a credible case be made that the deal undermines China’s Anti-Monopoly Law, or that it touches upon its Data Security Law, as it has a clear carve-out to protect the operation, ownership, and data of CK Hutchison’s ports in Hong Kong and China.

It is more likely that Chinese officials are using the threat of the provisions related to “collusion with foreign political forces” in the National Security Law, and those related to “state secrets” and “external interference” in the SNSO, to privately pressure CK Hutchinson to reconsider its position. These provisions have imported the wide-ranging PRC concept of state secrets, national interests and security into Hong Kong’s legal system, which would arguably include PRC’s overseas interests in critical infrastructure. Armed with these local laws, the Hong Kong National Security Committee on paper may have enough legal grounds to inquire into the port deal, with its decisions by design non-transparent and not subject to the scrutiny of any Hong Kong courts.

Both the company and Beijing have much to lose in this increasingly tense situation. CK Hutchison is currently seeking a secondary listing on the London Stock Exchange, which might include spinning out its telecommunications arm into a separate entity. This could all be scuppered by Chinese and Hong Kong regulators as revenge, if CK Hutchison goes ahead with the port deal. Following the recent example of British pharmaceuticals company AstraZeneca, shareholders may also take legal action against the company, citing the underreporting of the risks of CCP interference in its annual accounts.

A crackdown on CK Hutchison could meanwhile upend the efforts Xi Jinping has been making to improve relations with domestic and foreign business. Any such overt move would also play directly into U.S. arguments that CK Hutchison is ultimately under Beijing’s thumb — the whole reason for its complaints about the company’s ownership of the Panama Canal ports in the first place. The ire of regulators and the loss of face for Xi Jinping and Hong Kong Chief Executive John Lee if they let the deal proceed would pale in comparison to the greater risk if the PRC insists on marshalling the NSL or the Anti-Monopoly Law to punish CK Hutchison. That could see other jurisdictions follow the Trump Administration in pushing the company to divest from its holdings in critical national infrastructure on national security grounds.

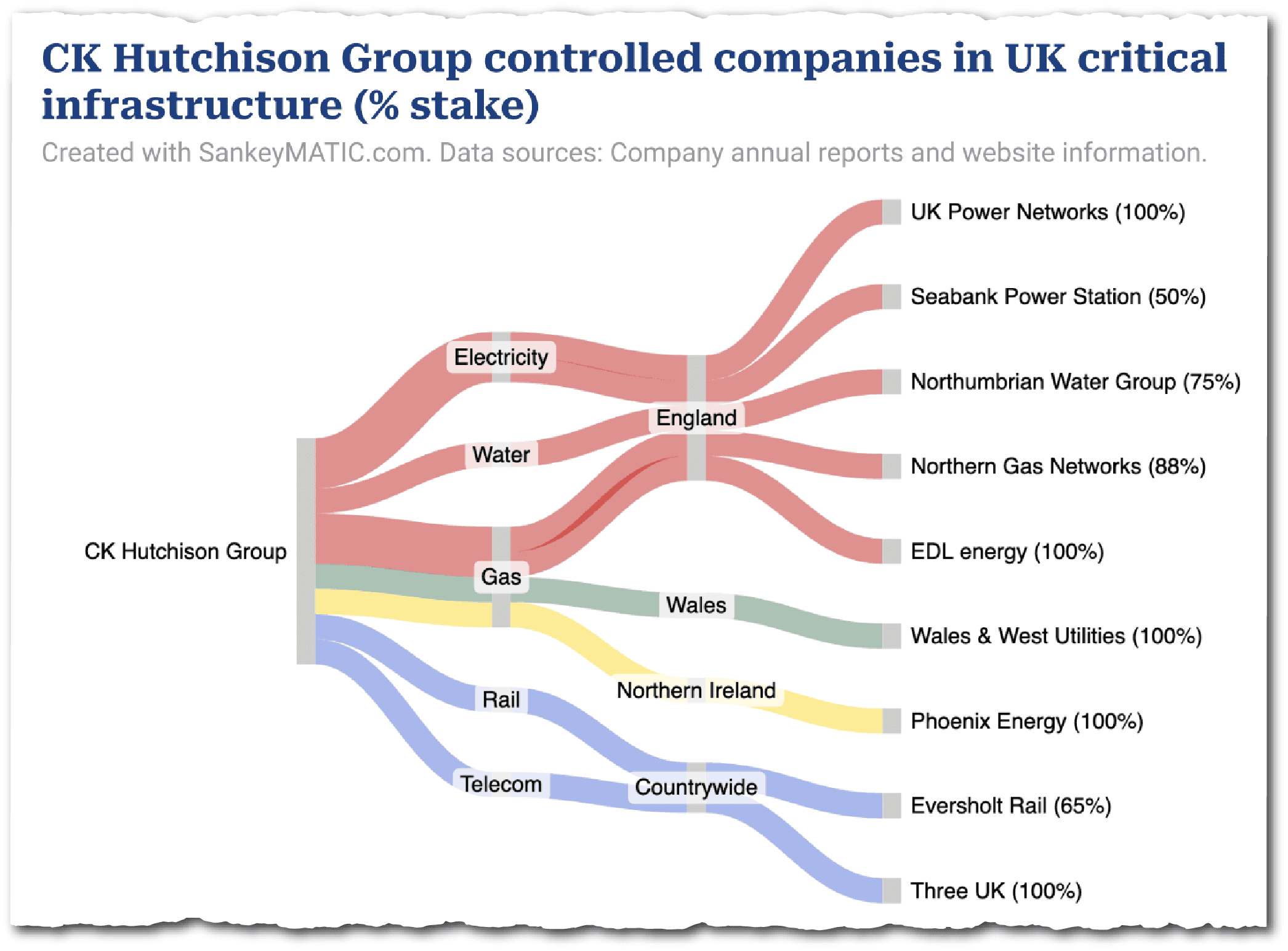

Take the case of the UK, where our analysis has found that CK Hutchison owns assets ranging from a 100 percent stake in the UK Powers Network, to 75 percent of Northumbrian Water Group and 100 percent of mobile network 3 (which recently merged with Vodafone). If the UK Government forced divestment from such assets it would mean CK Hutchison losing a significant portion of its business, and the loss for Beijing of an important lever of influence.

No wonder both sides are approaching this stand-off with caution and seeking a private resolution. The risks of the NSL, SNSO, or even the PRC Anti-Monopoly Law being used could sow the destruction of CK Hutchinson’s global empire and with it Xi Jinping’s rapprochement with the international business community.

Dennis Kwok is Co-Founder of the China Strategic Risks Institute (CSRI) and a faculty affiliate at Northeastern University. He previously served as a member of Hong Kong’s Legislative Council from 2012 to 2020.

Sam Goodman is the Senior Policy Director of the China Strategic Risks Institute.