When Craig Allen, then-president of the U.S.-China Business Council, met with the governor of one of China’s poorest agricultural provinces last year, he was surprised by the governor’s economic policy goals. Anhui, which is overwhelmingly rural, is hardly one of China’s top manufacturing hubs, and yet the governor rattled off a list of advanced industries he planned to prioritize: semiconductors, software, biotechnology, robotics, aerospace, batteries, and new energy vehicles — “neatly reciting,” Allen noted in a speech at Stanford University last year, “the key industries under the ‘Made in China 2025’ plan.”

The response stuck out to Allen not only because it seemed to ignore the needs of the governor’s constituents, but also because “it reinforced to me the very strong impression that the Chinese government, from top to bottom, is engaged in a techno-utopian quest that is breathtaking in scope. China’s unswerving and unquestioning commitment to advanced technology to resolve virtually every problem is going to have profound consequences for China and for the rest of the world.”

Indeed, that was the intent of Made in China 2025, Beijing’s industrial policy masterplan that debuted in May 2015 and comes due this year. The plan, which was signed and approved by premier Li Keqiang, proposed a three step process to vault China into the “ranks of manufacturing powers by 2025,” with the ultimate goal of leading global manufacturing and innovation by 2049, the 100th anniversary of the founding of the People’s Republic.

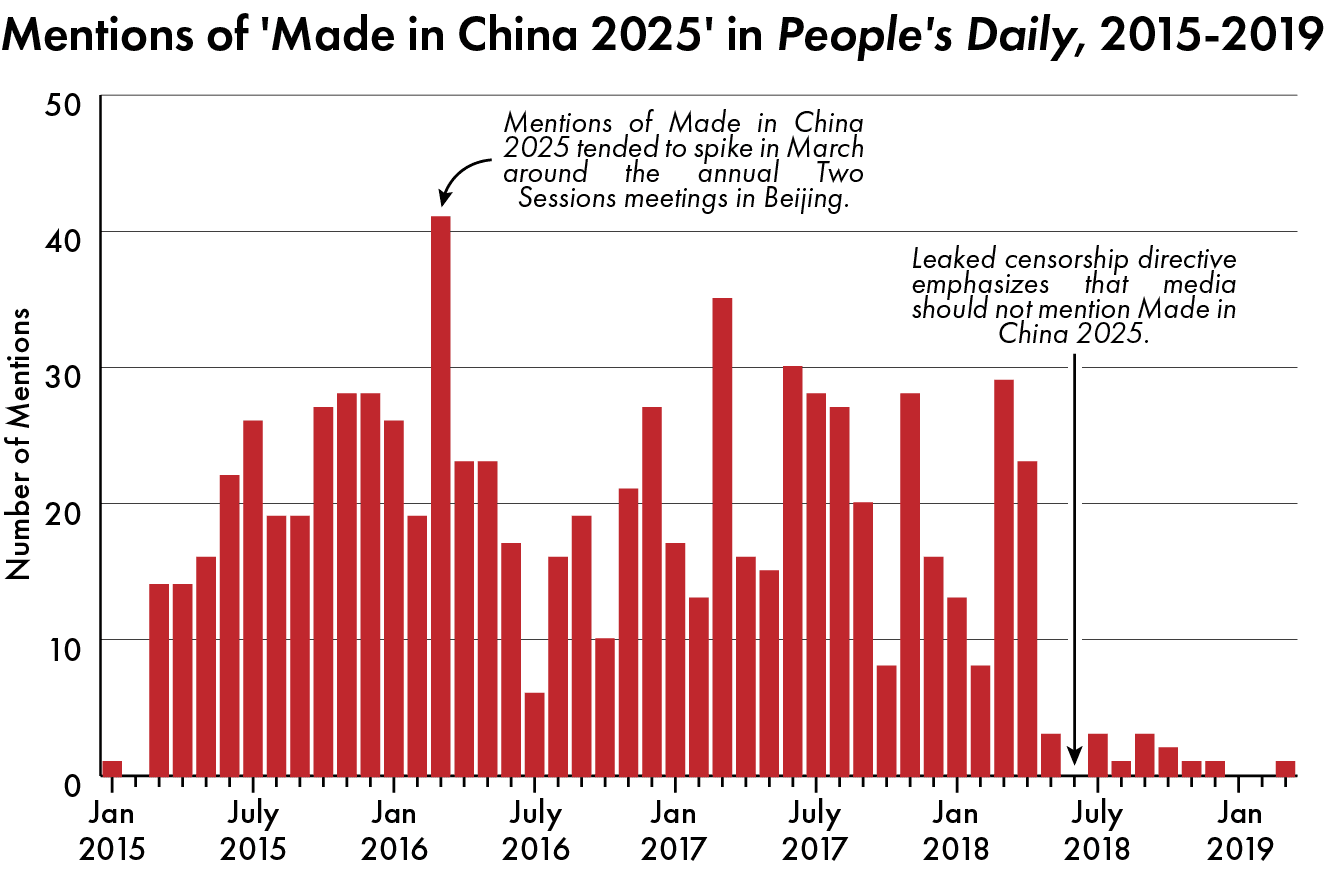

With the help of a wide array of policy tools — including research funding, import tariffs, subsidies, and tax exemptions — domestic producers mobilized with alarming speed. At one point, the fervor was so intense that People’s Daily, the official Chinese Communist Party mouthpiece, was talking about the policy, on average, six out of seven days a week.

Today, China has met many of its targets — and often vastly exceeded them. In industries like robotics and electric vehicles, China has gone from a bit player to the world’s dominant manufacturer and consumer.

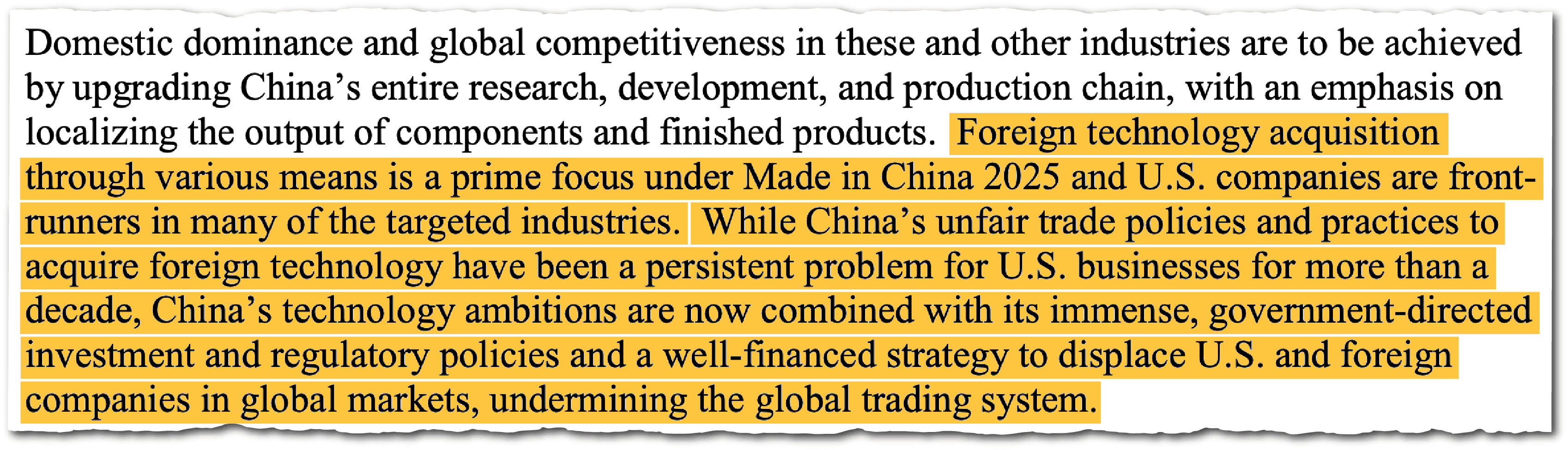

But that is not to say that all has gone according to plan for Beijing’s strategists. While Made in China 2025 was launched to great fanfare at home, it received a frostier reception abroad. Business leaders were some of the first to sound the alarm, with the European Chamber of Commerce in China issuing a dire report in 2017 warning that the strategy “amounts, in large part, to an import substitution plan.” And by 2018, the strategy was mentioned 116 times in Robert Lighthizer’s 2018 Section 301 report, which justified the U.S. tariffs that kicked off the first U.S.-China trade war. The initiative was also cited as a motivator for other measures, including the 2018 law that strengthened the powers of the Committee on Foreign Investment in the United States (CFIUS) and the U.S. semiconductor export controls.

The sharp downturn in relations with the West forced China’s economic planners to double down on building self-sufficiency — an objective that was not, in fact, a primary goal of the original Made in China 2025 plan. Feeling the pressure of self-sufficiency, however, policymakers soon became impatient with the pace of change, leading them to adopt increasingly direct interventions and exacerbating waste. Indeed, despite its efforts, China has still struggled to reach its goals in some industries — most notably, the semiconductor sector.

Amid growing backlash and criticism from foreign governments, Beijing abruptly stopped talking about the program around April 2018 and even ordered domestic media outlets to cease mentioning the initiative.

TALKING ABOUT MIC2025

Although you would be hard pressed to find a Chinese official uttering the Made in China 2025 name today, the initiative is still very much alive and well. And, as Allen’s interaction in Anhui shows, it continues to impact China’s economy — and influence U.S. policy.

“The strategy is still alive and more successful than ever,” says Jost Wübbeke, managing partner at Sinolytics, a China-focused consultancy, who wrote one of the first western reports on Made in China 2025. “If you look at the [2021] 14th Five Year Plan, you see a lot of the spirit of Made in China 2025 went into it. The core industries were almost the same; the only one they added was biotech.”

In honor of its 10-year anniversary and due date, we’ve decided to take a step back and assess the landmark initiative — its history, successes, struggles, and hurdles going forward.

Grading Made in China 2025 at a Glance

The Wire’s assessment.

| Next-generation information technology (inc. integrated circuits) | High-end numerically controlled machine tools and robots | Aerospace equipment | Ocean engineering equipment and high-end vessels | High-end rail transportation equipment |

|---|---|---|---|---|

| Failure | Success | Failure | Success | Success |

| Energy-saving cars and new energy cars | Power generation equipment | Farming machines | New materials | Pharmaceuticals and advanced medical equipment |

| Success | Success | To be determined | To be determined | Success |

AMBITIOUS GOALS

From the start, Chinese premier Li Keqiang made it clear that domestic substitution was a central objective of the plan.

“Now, the traditional ‘Made in China’ should continue,” he told global CEOs at a roundtable summit in June 2015, “but the core of Made in China should be ‘Chinese equipment.’” (The CEOs, at least publicly, responded warmly: the State Council published excerpts of positive letters. Klaus Kleinfeld, the chief executive of Alcoa, an aluminum giant, said in an interview with China Daily the company’s growing footprint in China was “aligned with the ‘Made in China 2025’ action plan.”)

Official documents from Beijing introducing the policy avoided specific production targets — any official mention could risk putting China offside of its World Trade Organization commitments. But hundreds of other documents published by semi-official sources, and ultimately endorsed by top government officials, spelled out China’s exacting plans for industrial dominance.

The most important of these documents was the “green book.” Authored by a committee of China’s top scientific minds, it set specific numerical targets for market share and local content requirements for China to hit within five and then ten years.

Some of these figures were wildly ambitious: in 2015, for example, China produced less than 100,000 electric vehicles, and almost none that were commercially competitive. Yet the auto industry may be one of the clearest victors among the Made in China 2025 sectors. Today, China commands 57 percent of the global EV market, producing 6.3 million cars in 2024. Shenzhen-based automaker BYD sold more cars globally in March than Tesla did.

Even economic planners involved in drafting targets back in 2015 failed to foresee the EV industry’s leapfrogging of internal combustion. Many of the numerical targets set by those planners were squarely focused on internal combustion technology, prescribing targets for fuel consumption standards, for example.

While foreign observers took note of the plan, few took Beijing’s wildly ambitious goals at their word.

“China puts out these sorts of plans, maybe less to that level of specificity, but it does put out very ambitious industrial plans all the time,” says David Lin, a senior director at the Special Competitive Studies Project (SCSP), a Washington, D.C., think tank.

Lin was working as a foreign service officer at the U.S. consulate in Shanghai when the plan was unveiled. “I remember a colleague saying at the time that they didn’t see any investment opportunities, so they kind of disregarded [the plan]. But that was the point. It’s an industrial strategy plan that is expressly aimed at eliminating U.S. investment opportunities.”

ROBOT SUPREMACY

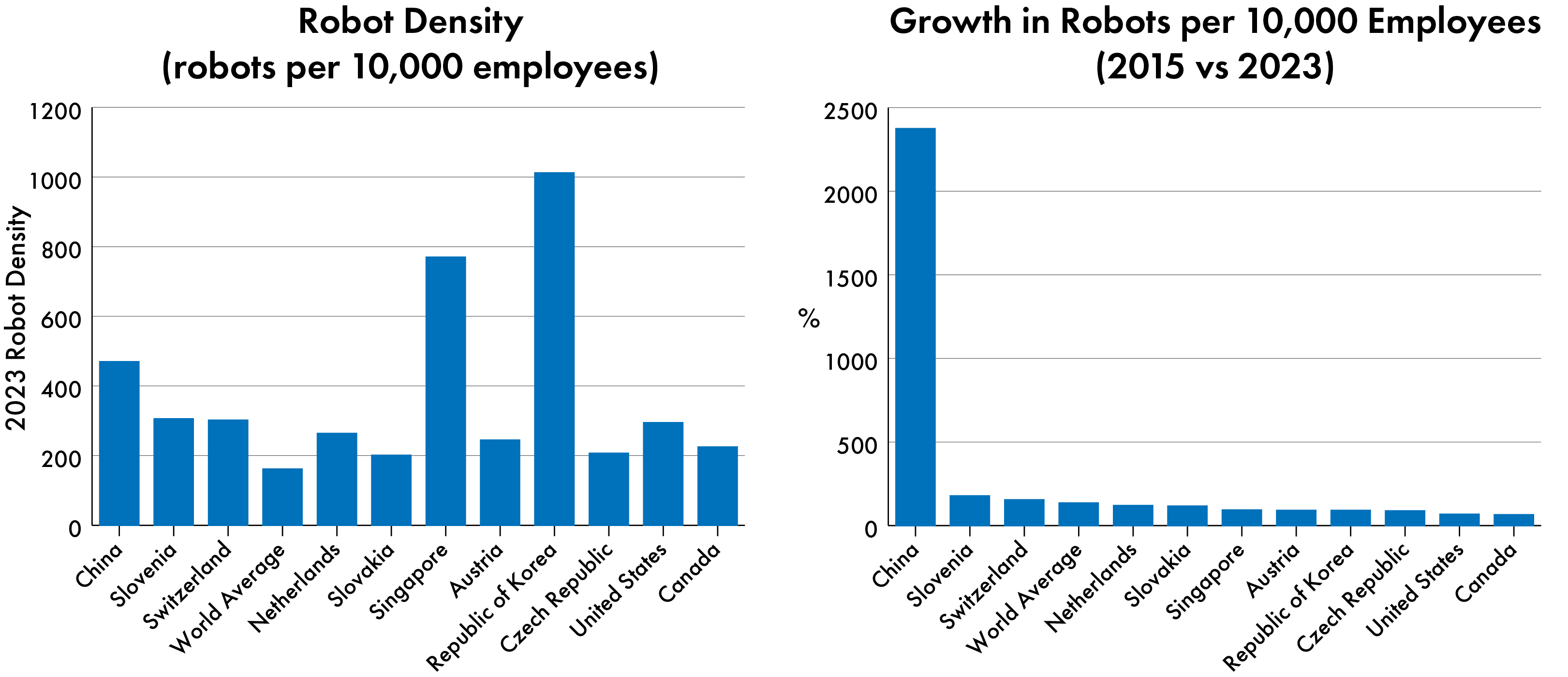

Although China’s EV triumph is often highlighted, a lesser known but correlated success from MIC2025 is the dramatic growth in industrial robot installations. Worldwide, the density of factory robots (the number of robots per 10,000 people) has more than doubled since 2015. But that figure is almost single handedly inflated by growth from China, where robot density ballooned a staggering 2,400 percent between 2015 and 2023.

In 2015, China was a laggard in robot installations, with a robot density rate that was one quarter of the global average, and 10 percent of the United States. Today, China ranks 3rd in the world in robot density.

As of 2023, 1.8 million robots operated on China’s factory floors — that’s more than 40 percent of the world’s factory robots, over twice the number that are installed in Europe and more than quadruple the number installed in the United States.

At facilities like Xiaomi’s electric vehicle factory in Beijing, automation reigns over whole parts of the production line for the smartphone-giant-turned-automaker’s flagship car, the SU7. While the most complex tasks like interior outfitting is still done by hand, the company boasts an overall 91 percent automation rate for its car manufacturing. (Volkswagen, for comparison, pledged in 2022 to automate 20 to 30 percent of its new EV plant near its Wolfsburg, Germany headquarters. Tesla, meanwhile, claims its Gigafactory in Shanghai is 95 percent automated.)

The Xiaomi SU7 being assembled at Xiaomi’s factory in Beijing. Credit: Lei Jun via X

Domestic firms, moreover, control more than half of the Chinese market, up from 30 percent in 2020, according to SemiAnalysis, a chips and AI consultancy. The most well-known (and controversial) is Guangdong-based Midea Group, which was originally a white goods company before it acquired the pioneering German robotics firm Kuka in January 2017.

“Kuka was a lighthouse project that stood for German smart manufacturing,” says Wübbeke. It really was producing cutting edge technology, and then Midea said it would buy it outright. I would say that was a turning point in how Germany saw China. After that it became much easier to block Chinese investment.”

Many Chinese firms remain reliant on foreign parts manufacturers for complex components like sensors and motors, but decreasingly so. Estun, for example, a Jiangsu-based industrial robot maker, boasts that 95 percent of its components are produced in-house.

The extraordinary growth has made China into a frontrunner in the race to develop “humanoid robots,” which hope to use artificial intelligence in combination with humanlike machines.

Building an effective humanoid robot requires large amounts of three-dimensional data, which is “very different from [large language model] data,” says Sunny Cheung, a fellow for China Studies at the Jamestown Foundation, who has studied China’s robotics and AI ecosystem. China’s lead in deploying robots and its advances in developing key components like high quality sensors, he notes, puts it at an advantage over rival countries.

SHIP BONANZA

As with China’s dominance in EVs, much has been made about China’s dominance in shipbuilding. But interestingly, the country has only modestly increased its total capacity over the last decade: in 2015, China delivered ships with a total deadweight capacity of 41.8 million tons; in 2024, it delivered 48.2 million tons — a 15 percent increase.

Yet China’s shipbuilding has captured attention, especially in Washington, because last year, Chinese shipyards built more than half of the world’s new ship capacity. Moreover, a single Chinese shipbuilding, China State Shipbuilding Corporation (CSSC) built more vessels in 2024 by tonnage than the U.S. has since World War II, according to a recent estimate by the Center for Strategic and International Studies.

China now builds 359 vessels for every one vessel built in the United States.

Far from one single policy intervention or technological innovation, however, China has mostly been able to gobble up market share because overcapacity in the shipbuilding industry in the mid 2010s forced many other countries, including the U.S., to downsize their industries.

Developing China’s shipbuilding industry has long been a priority for Chinese policymakers: Since 2003, Beijing has passed at least 25 national-level plans to advance the industry. The overcapacity issue in the mid 2010s, however, offered a window of opportunity that policy advisors behind Made in China 2025 were quick to emphasize. They also channeled investment into high-tech ships and maritime equipment, such as deep sea oil rigs, icebreakers and LNG tankers.

It worked: In 2023, China led in orders for 14 out of 18 major types of ships, according to the country’s Association of the National Shipbuilding Industry (CANSI). CSSC, the state-owned shipbuilding behemoth, is also making progress towards building its first heavy icebreaker, which would allow China to traverse waters in the harshest polar conditions for the first time.

WHERE HAS CHINA FALLEN SHORT?

If EVs and robots are MIC2025’s biggest successes, experts point to two areas where China has most clearly fallen short of its goals: civil aviation and semiconductors.

Beyond being a matter of national pride, China’s economic planners have long viewed the development of a commercial aviation industry as a potential major economic driver. A frequently cited statistic in Chinese state media, attributed to Boeing, states that every 1 percent increase in civil aircraft sales contributes 0.7 percent growth to the national economy.

China’s leaders first wanted a domestic competitor to Boeing’s 737 and Airbus’s A320, and they charged COMAC, China’s civil aviation manufacturer, to deliver it. In May 2017, the C919 took its maiden flight, fulfilling what China’s State Council described as “the dream of generations of Chinese people.” Since then, China’s big three state-owned airlines have clamored to place orders for the jet.

But to date, its deliveries continue to lag far behind Boeing and Airbus, which collectively delivered close to 1,400 737s and A320s to Chinese carriers over the last decade.

COMAC has delivered only 14 C919 jets in the past eight years.

Made in China 2025’s target was to have domestic aircraft hold 10 percent of the domestic market.

The C919 also remains heavily dependent on foreign parts, despite China’s efforts to indigenize key parts of the supply chain.

“Most of the equipment… are effectively western products,” Richard Aboulafia, Managing Director of AeroDynamic Advisory, an aerospace consultancy, told the U.S. China Economic and Security Review Commission in February this year. “Some of those are the result of joint ventures between Western technology companies and local Chinese producers with the stated goal of copying them. But there are key areas, particularly engines… where they are simply imported in a box.”

“If they’re going to achieve true self-sufficiency, they need their own engine industry,” Aboulafia added. “But here, the barriers to entry in jet engines are even higher than in the airliner industry.”

CHIPS, CHIPS, CHIPS

In 1999, Xu Guanhua, China’s then vice-minister for science and technology, remarked that the country’s burgeoning information technology sector lacked a “core” — referring to semiconductors — and a “soul” — referring to operating systems. Made in China 2025 set out to change that — and received a lot of flak from the West as a result.

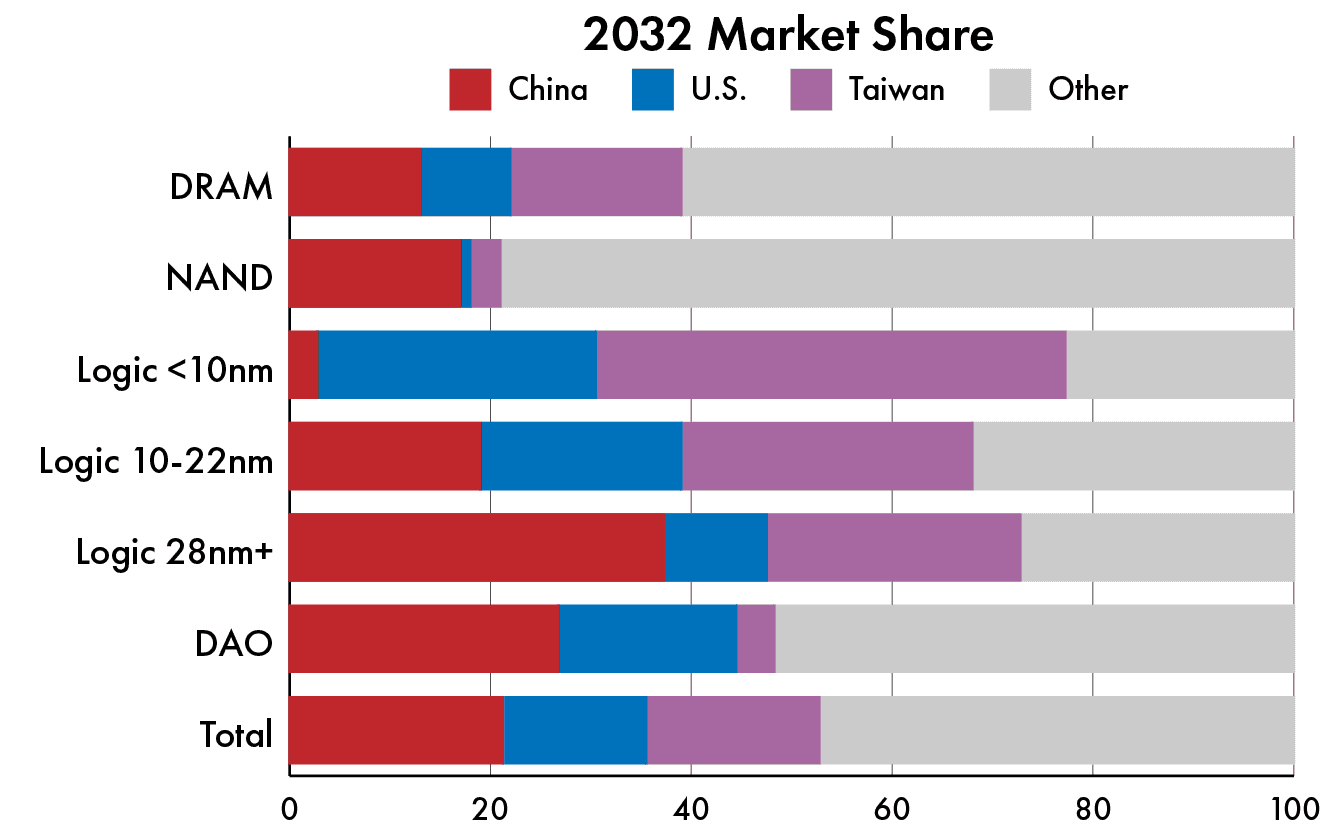

China’s advancements in chips is a mixed story so far. Although China has spent $142 billion dollars on its chip industry since 2014, the country still struggles to produce cutting-edge chips at the 10 nanometer process node and below. Sweeping U.S. export controls on the sale of cutting-edge chipmaking equipment to China makes it unlikely that the country will catch up in advanced chipmaking soon.

In fact, China’s share of global chipmaking is set to decrease while the U.S. market is expected to grow significantly. According to the Semiconductor Industry Association, a U.S. industry group, China is expected to hold 21 percent of the market in 2032. In 2022, it held 24 percent.

Although the U.S. is most concerned with leading-edge chips, China’s already sizable production lead on ‘legacy’ semiconductors — the less sophisticated chips that are nonetheless critical to many other electronics, such as solar panels and EVs — is expected to grow even more. The SIA forecasts that China will account for 37 percent of chips at 28 nanometers and above by 2032. In February, Huawei founder and chairman Ren Zhengfei even told Xi Jinping that the worries China had about a “lack of core and soul” had eased. “We firmly believe that even if the international situation changes, as long as the Party Central Committee with Comrade Xi Jinping as the core leads… there is nothing that cannot be overcome,” he said, according to the People’s Daily.

Credit: DSET

CHINA’S GROWING SELF SUFFICIENCY PUSH

Many analysts note that Made in China 2025 has changed considerably over the years and that many key themes — such as self-sufficiency — that are commonly associated with the initial plan were added on or bolstered along the way, especially as relations with the West soured. For instance, in late 2020, after the U.S. introduced sweeping sanctions against Huawei and as U.S.-China relations were thrown into a Covid-induced nadir, Beijing began drafting the 14th Five Year Plan, which more explicitly aimed to cut the West out of China’s supply chains by establishing “science and technology self-reliance and self-improvement” as a core position.

Scott Kennedy, chair of the Chinese business and economics program at the Center for Strategic and International Studies, argues that this was a small yet important change in strategy.

“The 14th Five Year Plan is different from Made in China 2025 in that it discusses [industry policy] in the context of China facing restrictions on global technology,” he says. “That may be a subtle shift, but it is a different framing. I think that framing is partially the result of expanded tech restrictions from the United States.”

As Beijing doubled down on self-sufficiency, it began erecting walls to both U.S. companies and foreign firms operating in the country. In the railway sector, for example, formal restrictions on procurement heavily favor China’s two state-owned rail stock manufacturers, CRRC and CRSC. There are also informal barriers, such as quotas set in 2021 for domestic procurement by public institutions like hospitals.

In a 2024 survey, the European Chamber of Commerce found that 58 percent of European businesses said they had missed business opportunities in China due to market access restrictions and regulatory barriers.

That’s the highest share recorded by the European Chamber of Commerce in China’s annual business confidence survey since Made in China 2025 was introduced.

The level of restriction varies widely by sector; the pharmaceutical and medical device sectors, for instance, which were included in MIC2025, are especially closed off to foreign competitors.

Although Kennedy notes that China’s “position in a variety of industries has improved dramatically,” the country still has a ways to go before it can fully cut foreign suppliers out of its supply chains, even for the Made in China 2025 sectors.

“No country is a successful island to itself,” says Kennedy.

Made in China 2025 was so successful, Sinolytics’ Wübbeke adds, in part because of its clear name and marketing. Today, by contrast, Beijing is trying to rally the country around “new productive forces” and other party lingo, as the U.S. and other western nations make moves to slow it down.

In other words, MIC2025’s past success is not predictive of whatever comes after it. As Wübbeke puts it, “There’s no story so powerful as Made in China 2025 was.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen

{kind=link}