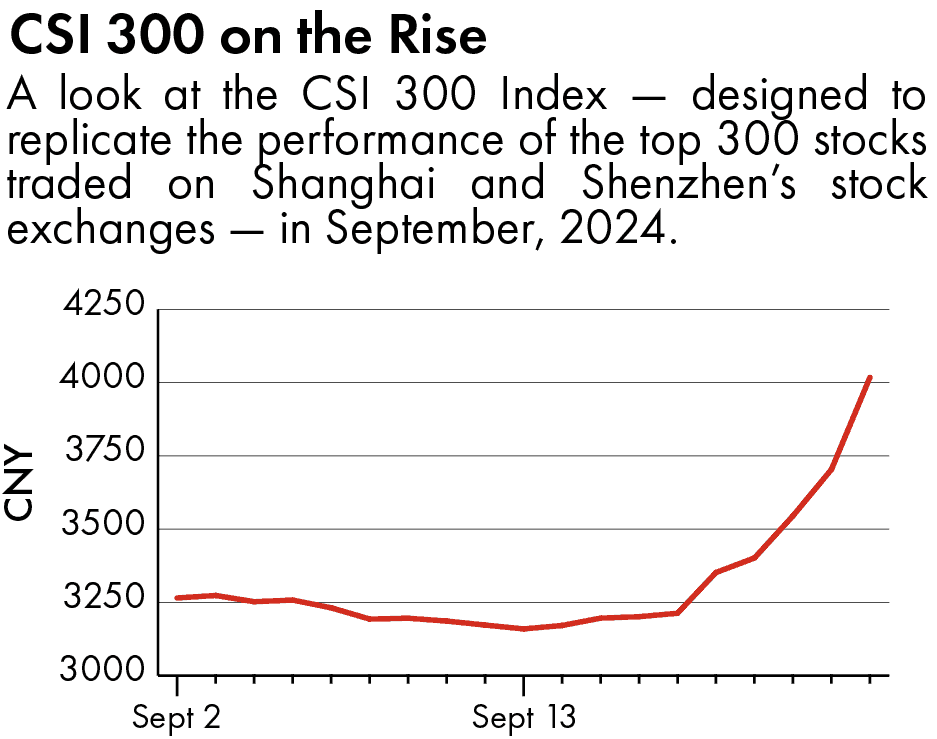

China’s recent economic pivot has electrified financial markets and captured the attention of investors across the globe. In late September 2024, Beijing unleashed a potent blend of fiscal and monetary measures, spearheaded by the People’s Bank of China (PBOC), in a surprise move that caught even seasoned insiders off guard. The result? An extraordinary market surge, with the Shanghai Composite and CSI 300 indices skyrocketing over 25 percent, while sentiment reversed sharply from pessimism to exuberance.

To understand the depth of this shift, context is crucial. China’s economy was buckling under the weight of deflation, dwindling consumer demand, and a property sector in tatters. Policymakers had tried multiple stimulus measures over the past year, but these fragmented efforts fell flat. Market participants had grown disillusioned with the PBOC’s cautious, piecemeal approach, where rate cuts and liquidity injections seemed more like drops in a bucket.

Local bureaucracies, paralyzed by fear from ongoing anti-corruption campaigns, compounded the problem. Officials opted to sit on their hands, more terrified of making mistakes than taking action. Burdened by local debt, resources were drained, leaving central government policies to stagnate at the grassroots level. This inertia gave rise to what many described as “passive resistance,” where policy changes were either reluctantly implemented or ignored altogether. China’s economy seemed stuck in neutral — something had to give, and fast.

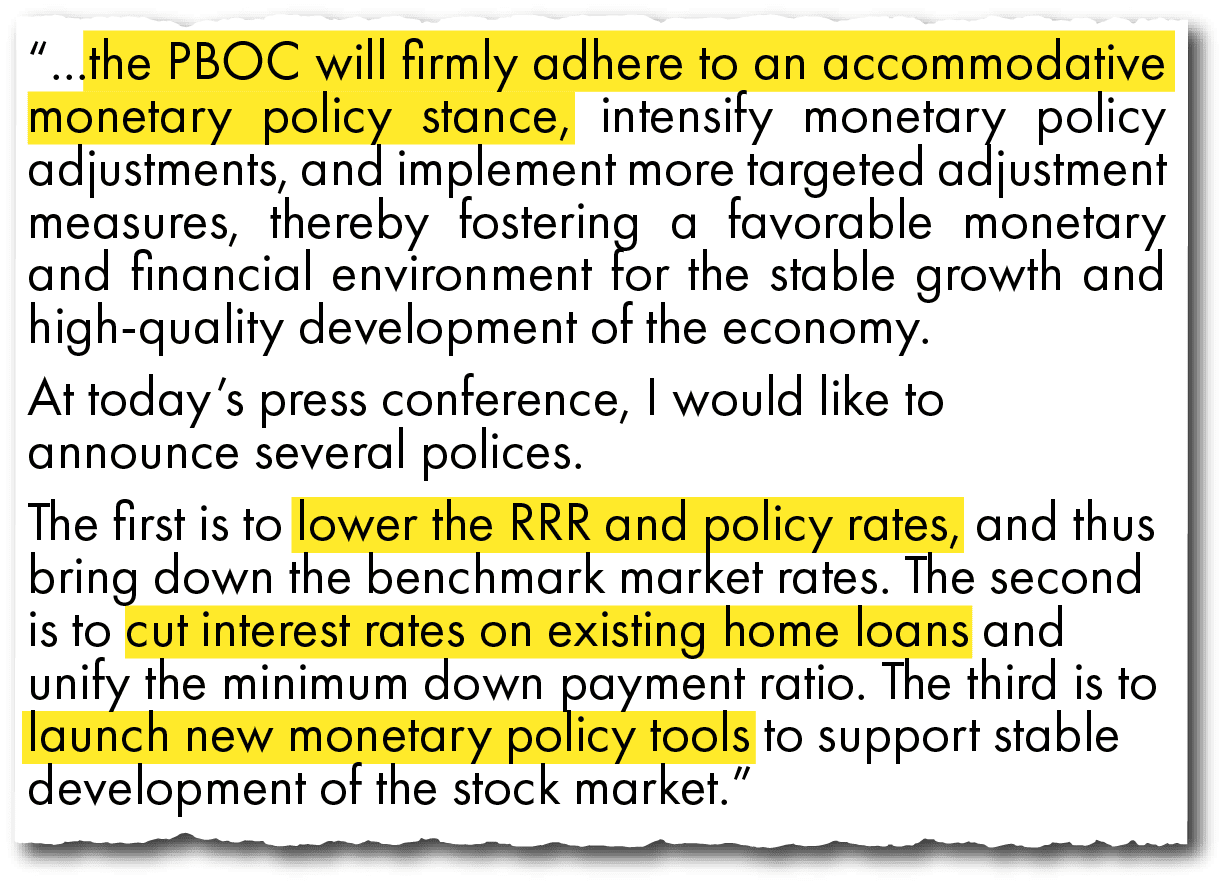

The events of late September marked a radical departure from this cautious stance. The PBOC, known for its hesitant “drip-feed” style, adopted a bold approach reminiscent of the U.S. Federal Reserve’s forward guidance strategy. The central bank made it clear that further rate cuts were imminent before the year’s end, breaking with the opaque, incremental measures that had left investors in the dark. This move sent a powerful signal: Beijing was no longer content with small fixes — it was prepared to go big.

The PBOC’s action was just one piece of a larger, coordinated policy shift. President Xi Jinping delivered an unambiguous message: it was time for officials to “be bold,” embracing risk to confront the nation’s economic challenges head-on. For a leadership that has often been risk-averse, this marked a sharp break from the past.

The timing of this intervention was as surprising as its substance. Even Chinese officials, accustomed to Beijing’s carefully choreographed policy maneuvers, were caught off guard by the rapid succession of announcements.

So why now, and why the sudden pivot? The pressure had been building for months. Deflationary fears were mounting, with troubling readings on the producer price index (PPI) pointing to Japan-style stagnation. Advisors had grown increasingly vocal, warning that China’s sacred 5 percent GDP growth target might be unattainable without more aggressive intervention.

The crux of their concerns was the crumbling real estate sector. Property prices had dropped around 10 percent annually, dragging down national wealth and shattering consumer confidence. As property values cratered, the impact rippled across the economy. Collateral for loans lost its value, liquidity risks mounted, and local governments, reliant on land sales for revenue, were left grappling with a fiscal crisis.

Foreign investors had grown increasingly wary. Concerns over inconsistent regulations and a lack of policy direction were mounting. Many business leaders had expressed these concerns to Xi Jinping’s economic advisors, who, in turn, relayed the gravity of the situation to the top leadership. Xi, it seemed, was listening.

The decision to launch what amounts to a campaign-style mobilization of local officials shows that the government is willing to pull out all the stops to ensure the success of its economic pivot.

At the heart of this sudden pivot lies a looming political challenge: mounting youth unemployment and the risk of social unrest. With youth unemployment climbing sharply and official figures for the 16-24 age group hovering near 18.8 percent, the sense of discontent was palpable. For a government that sees stability as non-negotiable, the risks posed by mass joblessness and growing social frustration had reached a tipping point.

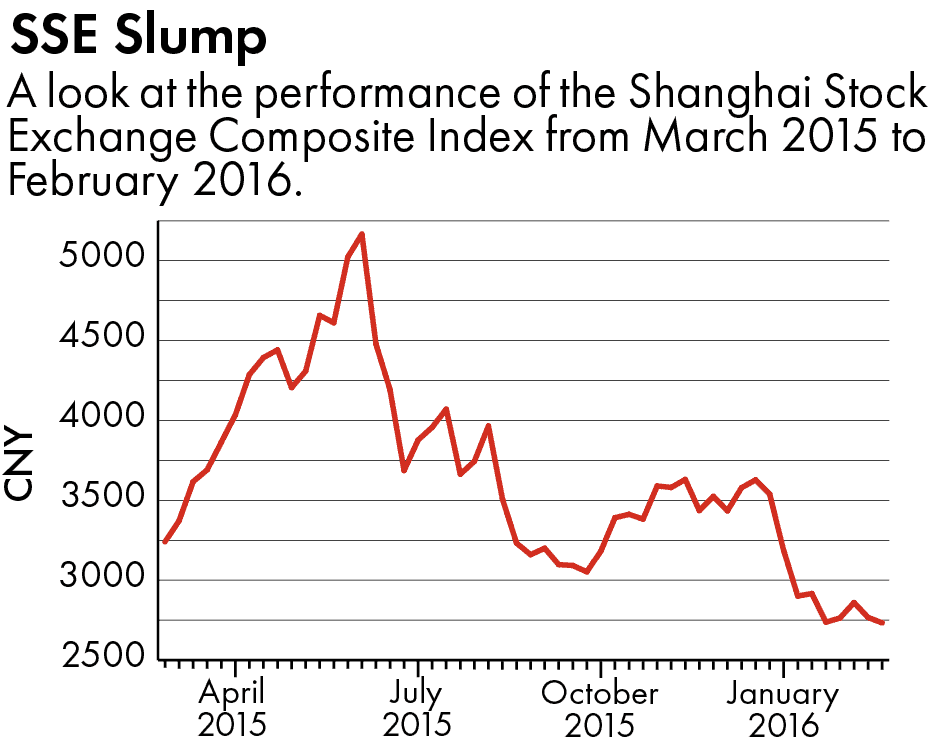

The PBOC’s forward guidance and Xi’s call for bold action have so far succeeded in reigniting market optimism. But while the initial results are promising, the question remains: will this newfound momentum last? China has been down this road before. The scars of the 2014-2015 stock market surge — and the subsequent crash — still run deep.

That previous bull market, fueled by similarly aggressive stimulus measures, ended in disaster. Speculative excesses pushed valuations to unsustainable levels, and when the bubble finally burst, the shockwaves rattled the entire financial system. Xi, who had just assumed power, was scarred by the experience and has since been cautious about allowing markets to spiral out of control.

But this time could be different.

For one, Beijing appears to have learned from past mistakes. Current financial regulators are less focused on inflating speculative bubbles and more aimed at creating a solid foundation to support China’s growth priorities. Stock valuations are much more reasonable now than during the 2015 bubble. Chinese equities are trading at historically low price-to-earnings ratios, making them attractive to both domestic and international investors. This more rational pricing provides a sturdier base for market stability.

Federal Reserve Chair Jerome Powell announces a cut to the interest rate by a half percentage point, September 18, 2024. Credit: C-SPAN

Moreover, the global environment is more supportive this time. Unlike in 2015, when China’s stimulus measures were battling against global monetary tightening, today’s international backdrop is one of easing. The U.S. Federal Reserve, after more than a year of interest rate hikes, is signaling a pause. This divergence between Chinese and U.S. monetary policy creates breathing room for the PBOC, reducing the risk of capital flight and giving Beijing more flexibility to stimulate growth without destabilizing the yuan.

But perhaps the most crucial difference is that the stakes for Xi Jinping are now even higher. The decision to launch what amounts to a campaign-style mobilization of local officials shows that the government is willing to pull out all the stops to ensure the success of its economic pivot. Local officials are now under direct orders to act swiftly and decisively.

To sustain this momentum and translate it into long-term growth, several critical steps must follow. Favorable capital market policies must continue to support the stock market to boost retail investor wealth. Increased household wealth can, in turn, fuel consumption and investment, creating a virtuous cycle of growth.

The IPO market needs a revival. Venture capital and private equity have historically fueled innovation and growth in China’s tech and energy sectors. To support long-term recovery, Beijing must encourage more companies to go public, giving institutional investors the chance to invest in high-growth industries. However, the government must strike a delicate balance between raising capital and maintaining investor confidence in secondary markets to ensure stability.

The real estate sector remains the linchpin, deeply linked to local government finances, banks, and household wealth. To stabilize it, the central government must deliver direct support to local governments, banks, and developers, likely through large-scale fiscal transfers, debt restructuring, and liquidity injections. Local governments, starved of revenue from land sales, need immediate fiscal aid. Banks, exposed to bad loans from defaulting developers, require a debt restructuring program to manage rising non-performing loans. Developers, too, may need targeted bailouts or mergers to prevent widespread bankruptcies.

But ultimately, China’s future success will depend on whether it can tackle its deeper, structural problems. Pension reform, relaxing the household registration system (hukou), and creating a robust social safety net are critical to ensuring that future growth is both sustainable and inclusive.

For now, Beijing has succeeded in reigniting market optimism and sending a clear message that it is serious about steering the economy back on track. Whether this marks the dawn of a sustainable bull market or just another fleeting boom depends largely on Beijing’s ability to deliver on its promises and tackle the structural issues head-on. The stakes are higher than ever, and Xi Jinping knows it.

Lizzi C. Lee is a Fellow on Chinese Economy at the Asia Society Policy Institute’s (ASPI) Center for China Analysis (CCA). She is an economist turned journalist, and graduated from MIT’s Ph.D. program in Economics before joining the New York-based independent Chinese media outlet Wall St TV.