It remains one of the most dramatic moments during a tumultuous presidency: Donald Trump stood in the White House’s Rose Garden on April 2 last year and announced America’s ‘liberation’ from unfair markets by applying sharply higher tariffs on U.S. imports from around the globe.

A year on, and the president’s signature economic policy has undergone several changes, most notably in February after the Supreme Court ruled against the tariffs the administration had imposed on the basis of emergency powers.

This week, The Wire takes stock a year on from Liberation Day, focusing on the main target of tariffs: China. And we look at how the U.S. government is seeking options to replace the role tariffs played in trade negotiations, while building a more diverse toolkit to boost strategic industries such as rare earths and semiconductors.

DOWN BUT NOT OUT

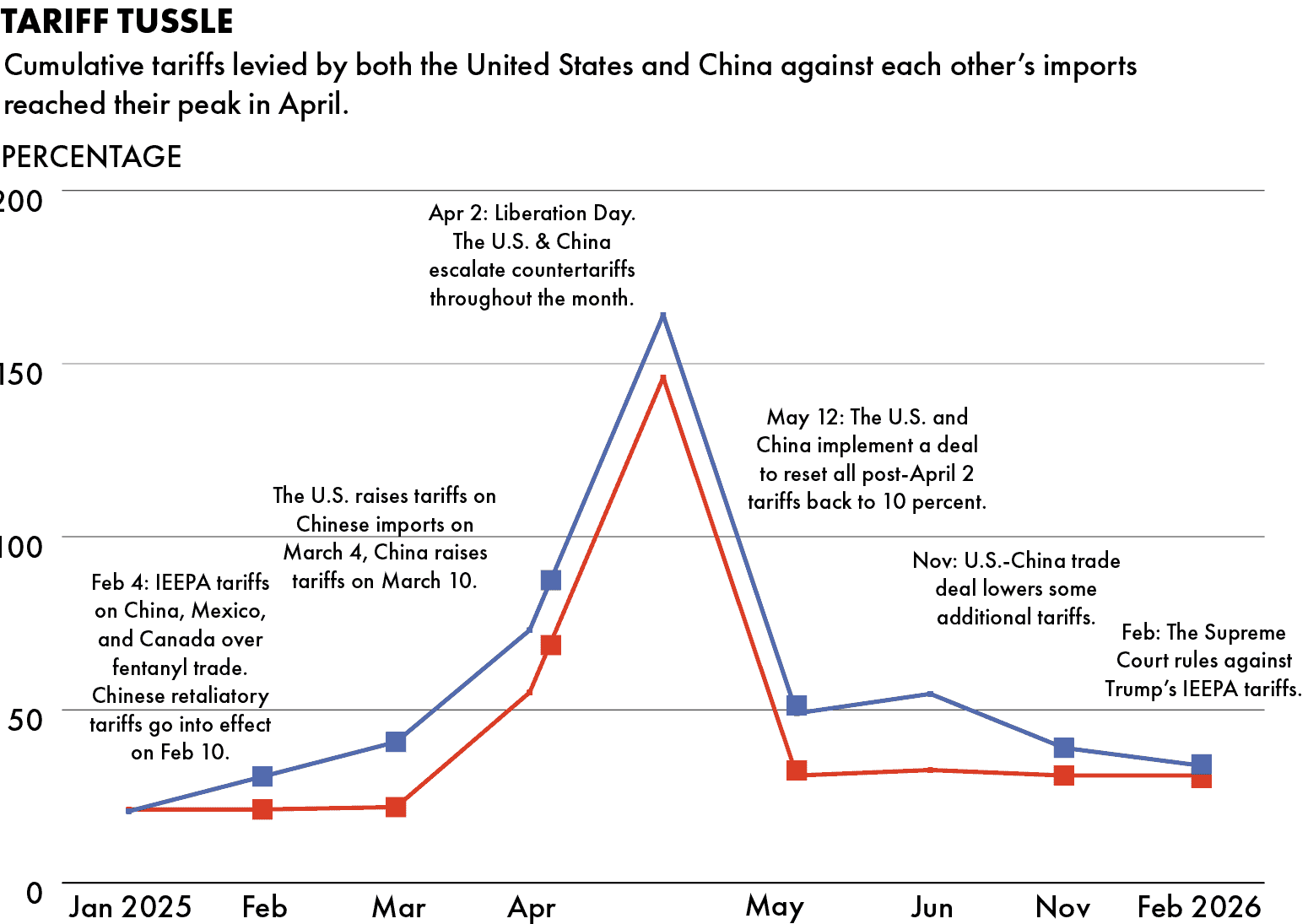

First, a recap. When Trump returned to office in January 2025, cumulative U.S. tariffs on China stood at about 20 percent. Even before Liberation Day, the president raised tariffs on Chinese imports by 20 percentage points under the International Emergency Economic Powers Act (IEEPA). On April 2, Trump levied a minimum 10 percent global tariff, with the overall levy on China even higher at 73 percent.

Throughout that April, China and the United States imposed escalating tariffs on each other. At their peak, U.S. tariffs on Chinese goods reached 164 percent. Both sides negotiated a climbdown in mid-May, and further deescalations in a trade deal after Trump and Xi met in South Korea last October. By February 20, the average rate had dropped to 36 percent, according to the Congressional Research Service.

After the Supreme Court’s February ruling against the IEEPA tariffs, there are three main types of tariffs still levied against China.

The Trump administration used one of them, Section 122 of the Trade Act of 1974, to enforce a 10 percent global tariff on February 24 as a quick replacement for IEEPA. According to a report by the Congressional Research Service, this was the first time Section 122 has been used.

Current U.S. Tariffs on Chinese Imports

| Applies to | Date introduced | Key Chinese imports affected | Features | |

|---|---|---|---|---|

| Section 122 of the Trade Act of 1974 | Globally | Feb 24, 2026 | All | Maximum rate: 15%; Time limit: 150 days |

| Section 301 of the Trade Act of 1974 | Select imports, in response to actions that violate or restrict valid U.S. commerce | First round of tariffs on China imposed from July 2018 | 100% on EVs, 50% on semiconductors and solar modules and other related products | No maximum rate; Time limit: 4 years, unless renewed |

| Section 232 of the Trade Expansion Act of 1962 | Select imports, in response to national security concerns | Aluminum and steel tariffs first imposed from March 2018 | 50% on iron, steel, aluminum, copper, and their derivatives; 10-25% on timber, automobiles & vehicle parts, and buses | Section 232 tariffs exempt from additional Section 122 tariffs |

Sources: PIIE, the White House, USTR, UN Trade and Development

The actual task of collecting these tariffs is complicated due to the shifting patchwork of exemptions and guidelines for the different products under each tariff law.

While these three trade acts give the U.S. tools to target strategic imports, none of them allow the government to target specific countries with high tariffs on all of their exports to the United States.

High tariffs against China were intended to push supply chains to relocate from the country for good, says Chad Bown, senior fellow at Peterson Institute for International Economics.

“All of that went away with the IEEPA decision,” Bown says. “If the Trump administration wants to replicate what they had last year in terms of that differential…they’ve got to figure out new legal authorities to get them there.”

THE TARIFF EFFECT

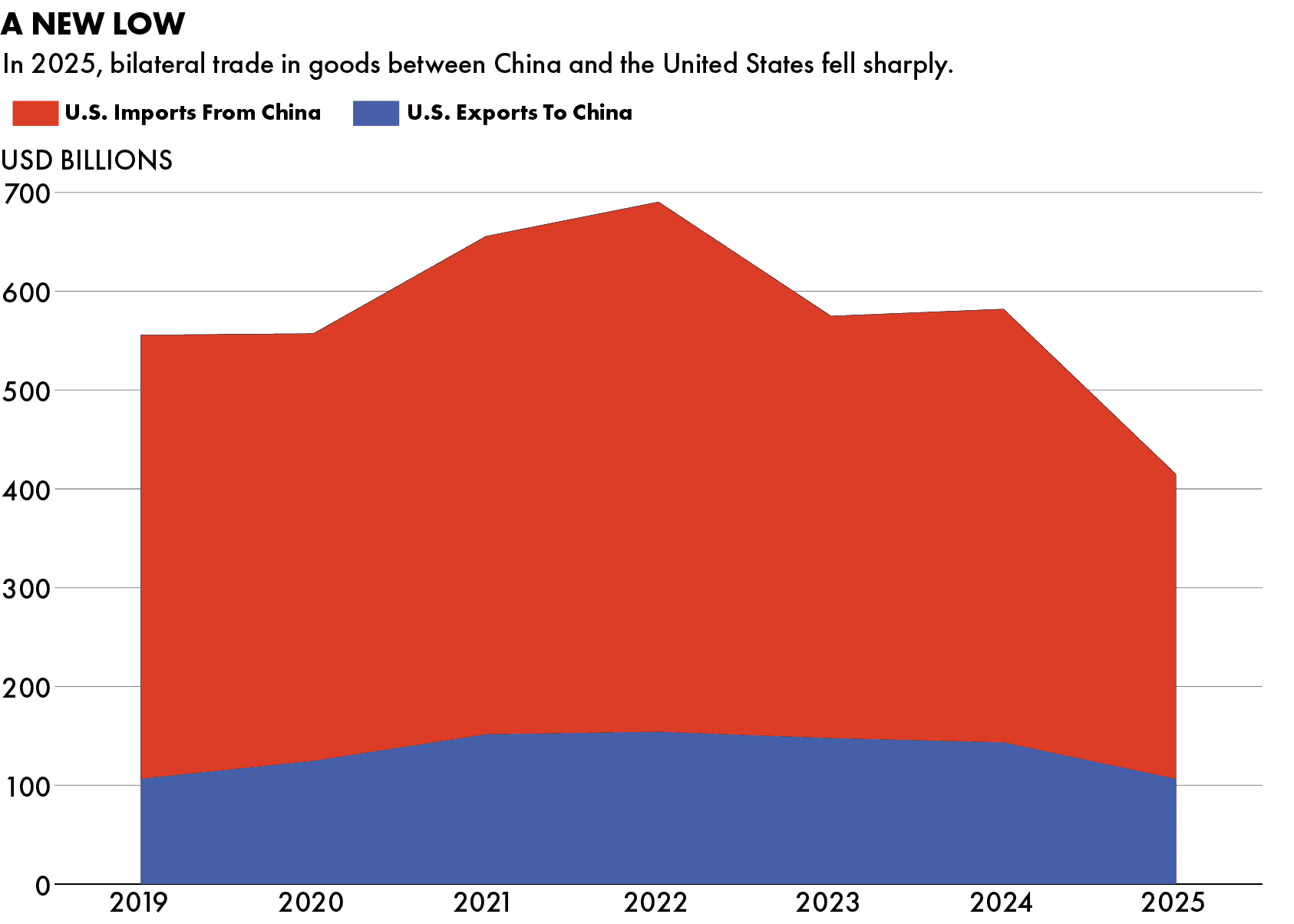

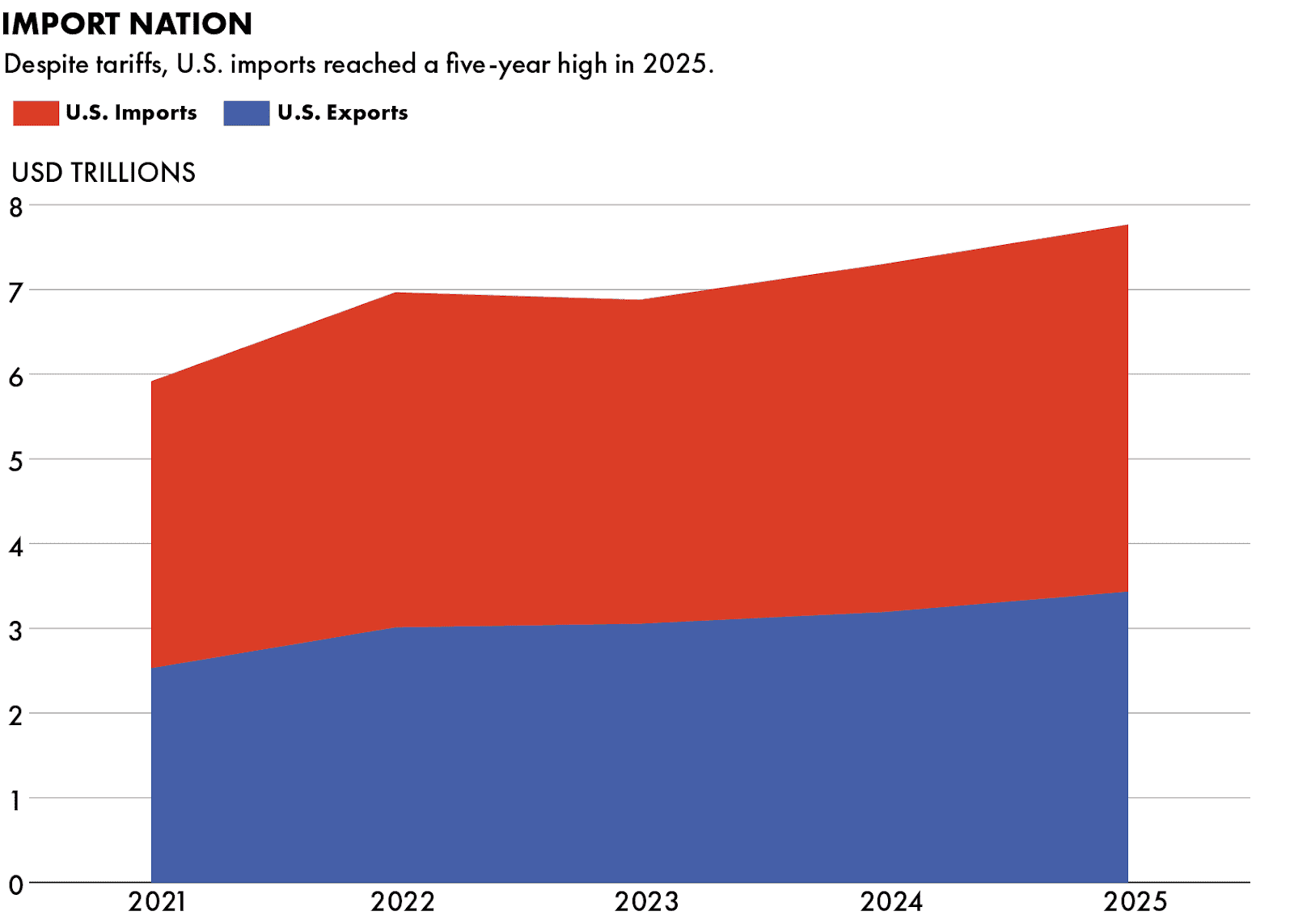

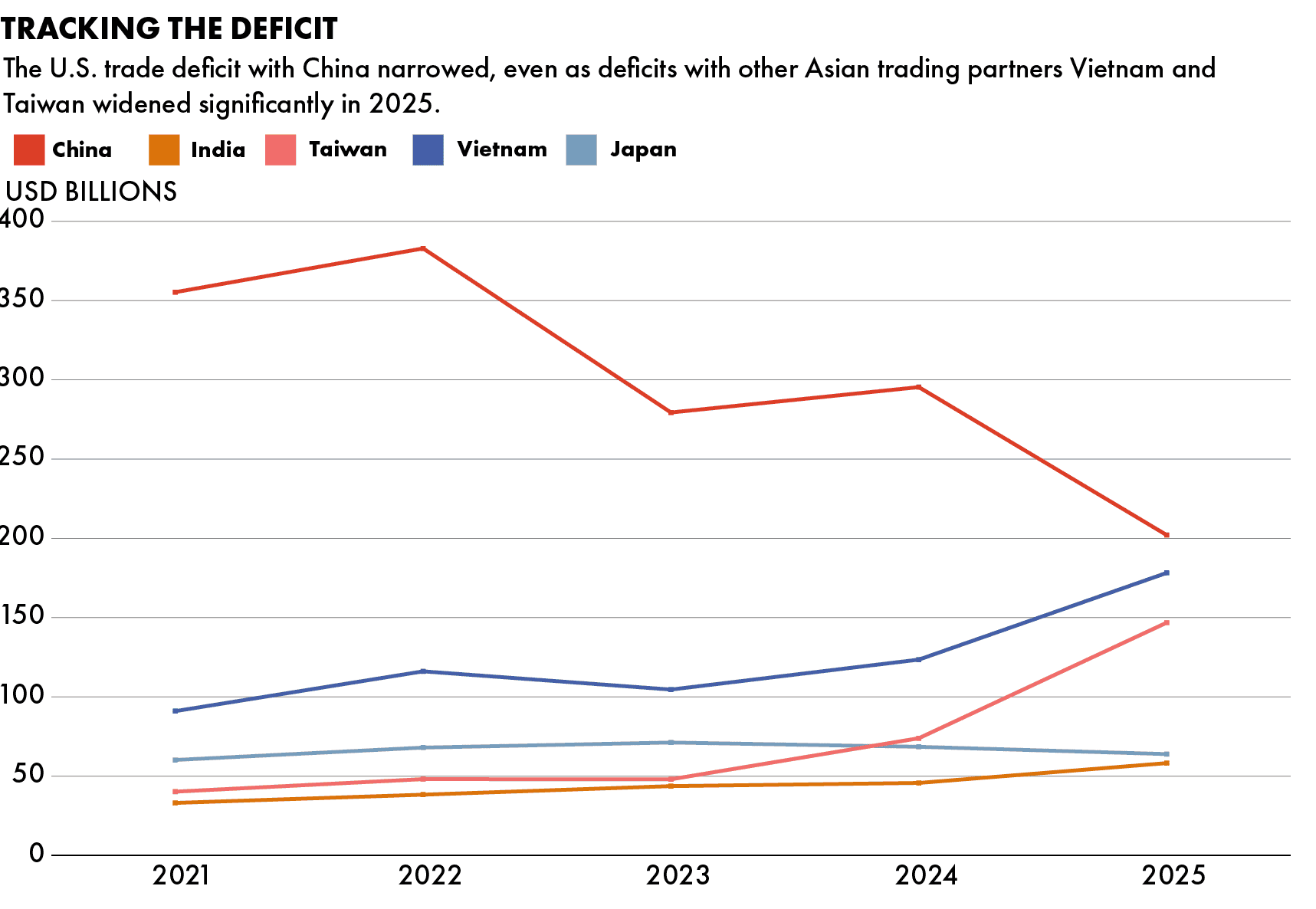

On the surface, the Trump tariffs have achieved one of their apparent goals. The U.S.’s bilateral trade with China had been steadily narrowing since 2022, but trade flows dropped to their lowest level in six years in 2025. The trade deficit with China — long a bugbear of Trump’s — narrowed by almost a third to $202.1 billion in 2025, according to data from the U.S. Bureau of Economic Analysis.

But as supply chains have shifted out of China to other countries, American buyers simply followed them. And the tariffs have done little to stop a growing amount of imports into the country.

China’s share of Asian imports to the U.S. has decreased as neighboring countries stepped into the gap. BEA data shows that between 2024 and 2025 the U.S. trade deficit with Taiwan widened to $146.8 billion from $73 billion, and to $178.2 billion from $123 billion with Vietnam.

But on other economic goals, including restoring U.S. manufacturing capability, tariffs have not moved the needle very far.

“Because U.S. manufacturing relies on foreign inputs that are subject to tariffs, there isn’t the benefit of a revival of manufacturing,” says Jack Zhang, founder of the Trade War Lab at the University of Kansas.

“Import competition is still the same whether it’s coming from a supply chain that is 70 percent based in China, or a supply chain that’s 50 percent based in China,” he says.

A WAY OUT?

“The United States has now unwound the supply chains that were easy to unwind, and the ones that are left are the ones that are really, really hard to break away from,” says Bown.

The remaining tariffs from Sections 232 and 301 imposed on high-tech goods and raw materials underscore sectors where China is still dominant. China has made huge strides in building tailored policy instruments to protect its strategic industries since 2018, says Zhang. “There is a greater degree of state involvement and definitely more subsidies for technological self-sufficiency that counterbalance more liberalizing tendencies.”

China’s chokehold on the critical minerals and rare earths that are key to products from high-tech consumer goods to weapons is particularly frustrating for the United States. China controls nearly 70 percent of their global production.

Beijing’s use of export controls on rare earths brought both countries to the negotiating table last fall, when both the U.S. and China agreed to lower some tariffs and delay implementation of the controls.

“The United States is desperately trying to import these things from China just because there’s no alternative source,” says Bown. “That in and of itself really is what slowed down the trade war last year.”

Washington is developing a playbook for crucial industries, including rare earths, by taking a page from Beijing’s playbook: acquiring stakes in private companies that could enable the government to direct their activities more in line with national priorities.

In addition to rare earths, Washington is also investing in companies working on chips, nuclear energy and semiconductors.The chart below details the government’s major interventions in private companies over the last year, according to a report by the Center for Strategic and International Studies

Federal Investment in Key Industries

| Sector | Company | Government Financial Agreement | Cost |

|---|---|---|---|

| Minerals | USA Rare Earth | 10 percent stake | $1.3 billion loan from CHIPS Act plus $277 million |

| Vulcan Elements | $50 million equity stake | $620 million loan and $50 million equity stake | |

| MP Materials | 15 percent stake | $400 million | |

| Korea Zinc | 40 percent stake in a joint venture, 10 percent stake of the company | $1.9 billion plus $210 million in CHIPS Act subsidies | |

| Lithium Americas | 5 percent stake in the company, 5 percent stake in a joint venture | $182 million in deferred debt service | |

| ReElement Technologies | Warrants to purchase future stock | $80 million by DOD “matched by private capital” | |

| Trilogy Metals | 10 percent stake, plus right to an additional 7.5 percent stake | $35.6 million | |

| Nuclear Energy | Westinghouse Electric Company | Option to take an 8 percent stake, entitled to receive 20 percent of certain cash distributions | $80 billion project involving the company and the U.S. government; U.S. investment not finalized |

| Semiconductors | Intel | 9.9 percent stake | $8.9 billion |

| xLight | $150 million equity | $150 million | |

| Nvidia | 15-25 percent of revenue from certain chips sold to China | N/A | |

| AMD | 15 percent of revenue from MI308 chip sales to China | N/A | |

| Steel | U.S. Steel | “Golden share” granting special governance rights to the U.S. president | N/A |

Source: CSIS

This evolution in U.S. industrial policy is one potential solution to the problem tariffs could not solve — building a China-free supply chain in critical areas, not just phones or shoes.

Unlike China, the U.S. does not have a long history of government involvement in private industry. Bown is skeptical that it will go smoothly.

“If we’re going to make this work, I do think the U.S. government really has to think hard about how to create the right incentives for itself and for these companies for them to ultimately be successful,” he says.

Savannah Billman is a Staff Writer for The Wire China based in NYC. She previously worked at the National Committee on U.S.-China Relations.