The CCP’s annual Central Economic Work Conference (CEWC) took place just over a week ago, concluding just before a press conference at which senior International Monetary Fund officials answered questions about their soon-to-be-published annual Article IV report on the state of China’s economy. Both events shed light on the 2026 outlook. The topics were identical, then — the views not so much.

The CEWC mostly echoed the content of the Fourth Plenum in October and the December Politburo meeting, serving as a bridge between the 14th and 15th Five Year Plans. The government’s normal enthusiastic rhetoric confirmed that it is ‘on the correct path’, but, having acknowledged a range of persistent, specific problems, it nevertheless set out multiple prescriptive policy measures designed to address them yet again, or anew. These problems include imbalances between ‘strong domestic supply and weak demand’, a ‘complex external environment’, continuing concerns about real estate and financial stability, involution or disorderly competition, and price deflation. Indeed China’s GDP deflator, the broadest measure of inflation, has been declining for 10 consecutive quarters since early 2023, pushing nominal growth down to a lowly 3.5-3.75 per cent per year.

Against the backdrop of exceptionally weak November retail sales — a record low rise of 1.3 per cent — and the first annual fall in investment since 1998, monetary policy will be eased further in the coming year, joined by additional consumer- and property-friendly policies. Fiscal policy, though, will be asked to do the heavy lifting in 2026. Even so, because of growing debt and debt capacity problems, especially at the local government level, the central government remains cautious, advocating for more judicious and effective allocation of spending, rather than major stimulus.

While the tasks for 2026 include the enhancement of high quality development, boosting rural incomes, promoting green policies, and doing ‘more practical things for the masses’, the top two goals are to strengthen domestic demand, and to persist with innovation-driven development and the exploitation of ‘new productive forces’ in advanced manufacturing and technology.

This is all very familiar, but the shift in tone with regard to domestic demand, especially consumption, is notable. New initiatives might include extending the consumer goods trade-in scheme, additional social spending for the elderly, childcare and healthcare, and support for consumption-oriented lending programmes. Some measures may fall on the central government’s balance sheet, rather than on those of cash-strapped local governments.

The problem, though, is that it’s not possible to shift to a more consumption-centric economy without extensive liberal economic and political reforms. Since these are certainly not on the agenda, it is likely that the main stimulus in 2026 will again focus on investment in preferred manufacturing industries, and infrastructure, even at the cost of exacerbating China’s imbalances.

In any event, while the property market remains a major drag on household wealth, and confidence, households will remain cautious. Former Finance Minister Lou Jiwei has stated that the property slump could hinder growth for another five years. The liquidity crunch at property giant China Vanke and its possible default have thrown new uncertainties over the financial markets, banks and trusts, and local government finances.

To stabilize the property sector in 2026, the government could establish new mortgage subsidies, raise tax rebates on property sales, and lower transaction fees. None of these are likely to shift chronic oversupply much – ranging from 17 months’ worth of housing stock in Tier 1 cities to over 40 months in Tiers 3 and 4 – or halt the inexorable decline in prices, until there is a credible programme to reduce the number of unsold homes. The IMF estimates this could cost at least 5 per cent of GDP, which Beijing seems not to want, and which local governments cannot afford.

There was little discussion in the CEWC read-out about the other elephant in the room, trade. It acknowledges, as did the Politburo meeting, that China must ‘better coordinate domestic economic work with international economic and trade struggles’. Yet there was little to suggest China will try to reduce its $1 trillion trade surplus in goods – or $2 trillion in annual manufactured goods. Pushback by the United States and EU may be par for the course, but with emerging and middle income nations lining up too to complain about excessive Chinese supply, China has good reason to take note of why this is happening and its consequences.

If little changes, there will be rising commercial tensions between China and a growing number of nations over the consequences of Beijing’s industrial and mercantilist trade policies.

George Magnus

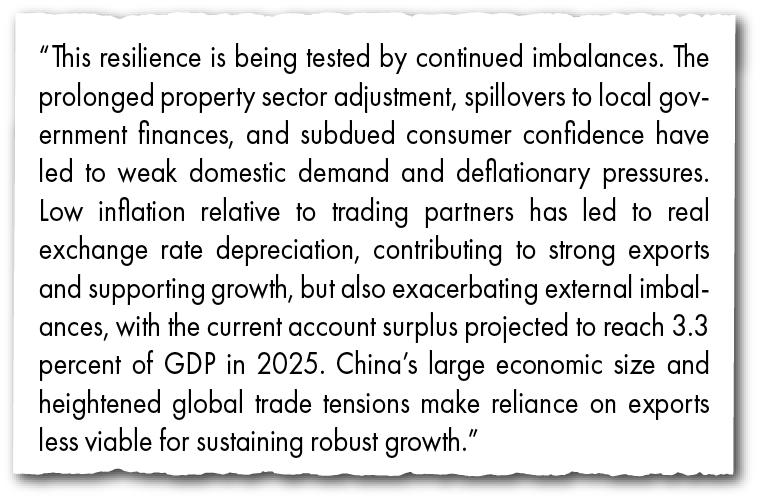

The IMF is at least doing so, finally. At its Article IV mission press conference, officials referred to persistently weak Chinese domestic demand, arising from weakness in property and deflationary pressures. It also emphasised an array of drags on growth, including slowing productivity, high levels of debt and limits to debt capacity, a decline in investment returns, and demographic factors, as well as the unsustainability of China’s outsized net export contribution to GDP.

The Fund’s staff want to see more emphasis on rebalancing the economy towards consumption, more expansionary policy stimulus, stronger fiscal support for social protection, and regulatory, skills and services initiatives to bolster the economy over the medium-term. Pointedly, it seems to think China’s industrial policy is now a growth inhibitor, with one official stating ‘we have concluded that industrial policies in China need to be scaled down’, citing productivity losses and misallocation of resources. Beijing’s view in the Article IV report will doubtless differ.

The IMF’s patience with China’s trade position may also be wearing thin. It attributes the soaring trade surplus both to weak consumption and imports, and to policy and price developments that have lowered the yuan’s real effective rate by about 20 per cent since 2022. While the IMF said ‘we would like to see China with an exchange rate that is flexible’, and that China should not provoke protectionism by partner countries, the CEWC’s discussion on this matter was in-passing, and spoke only about ‘basic stability’ regarding the yuan.

It is clear that a range of contradictions is set to intensify in 2026. The government’s own assessment of the economic and industrial outlook is conflicted. There are important differences emerging between how China and the IMF view the economy, and industrial and trade policies. And if little changes, there will be rising commercial tensions between China and a growing number of nations over the consequences of Beijing’s industrial and mercantilist trade policies.

George Magnus is a research associate at Oxford University’s China Center and at SOAS, and the author of Red Flags: Why Xi’s China is in Jeopardy. He is the former Chief Economist of UBS.