Nobody expected China’s automakers to wage war for so long.

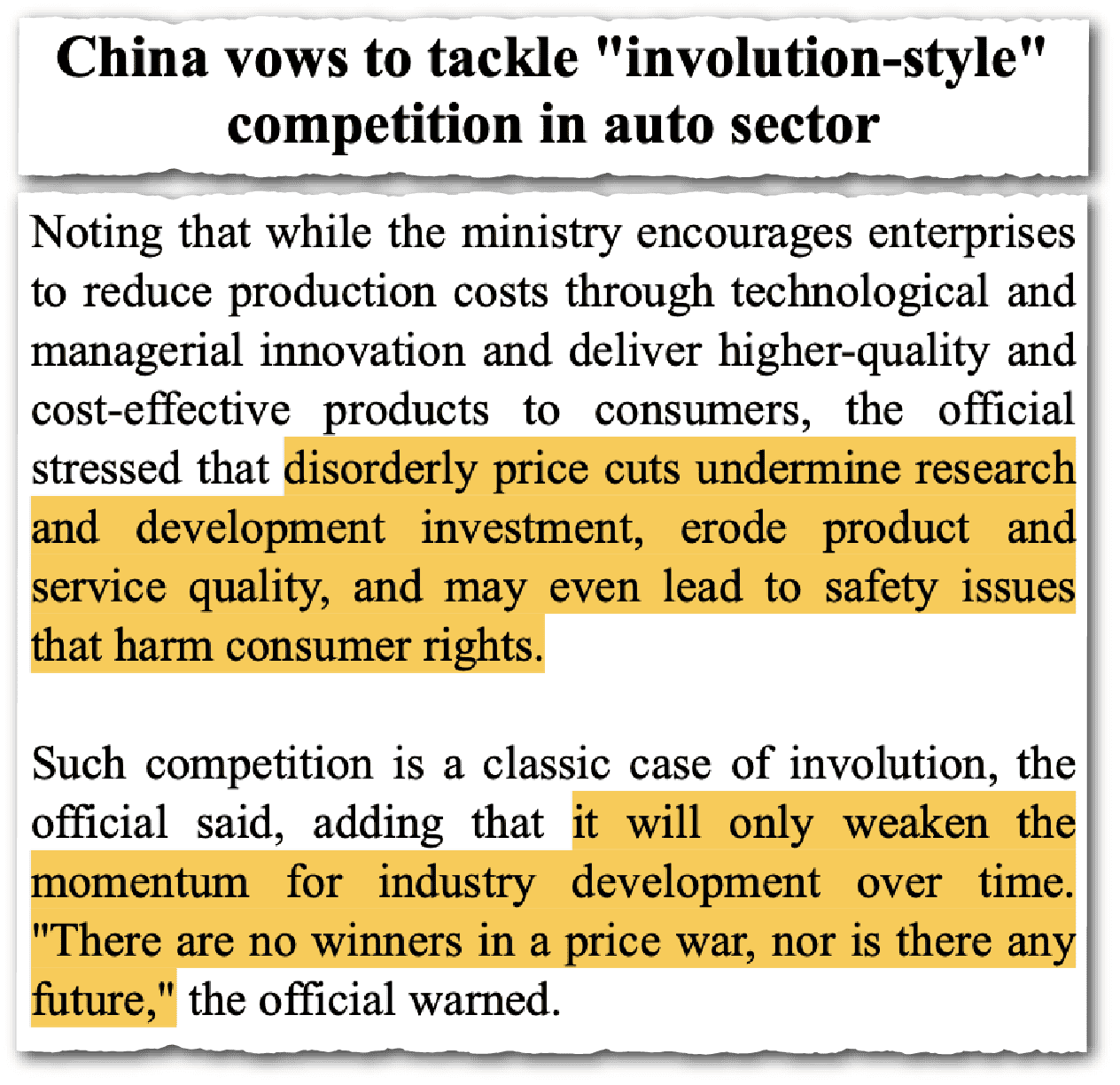

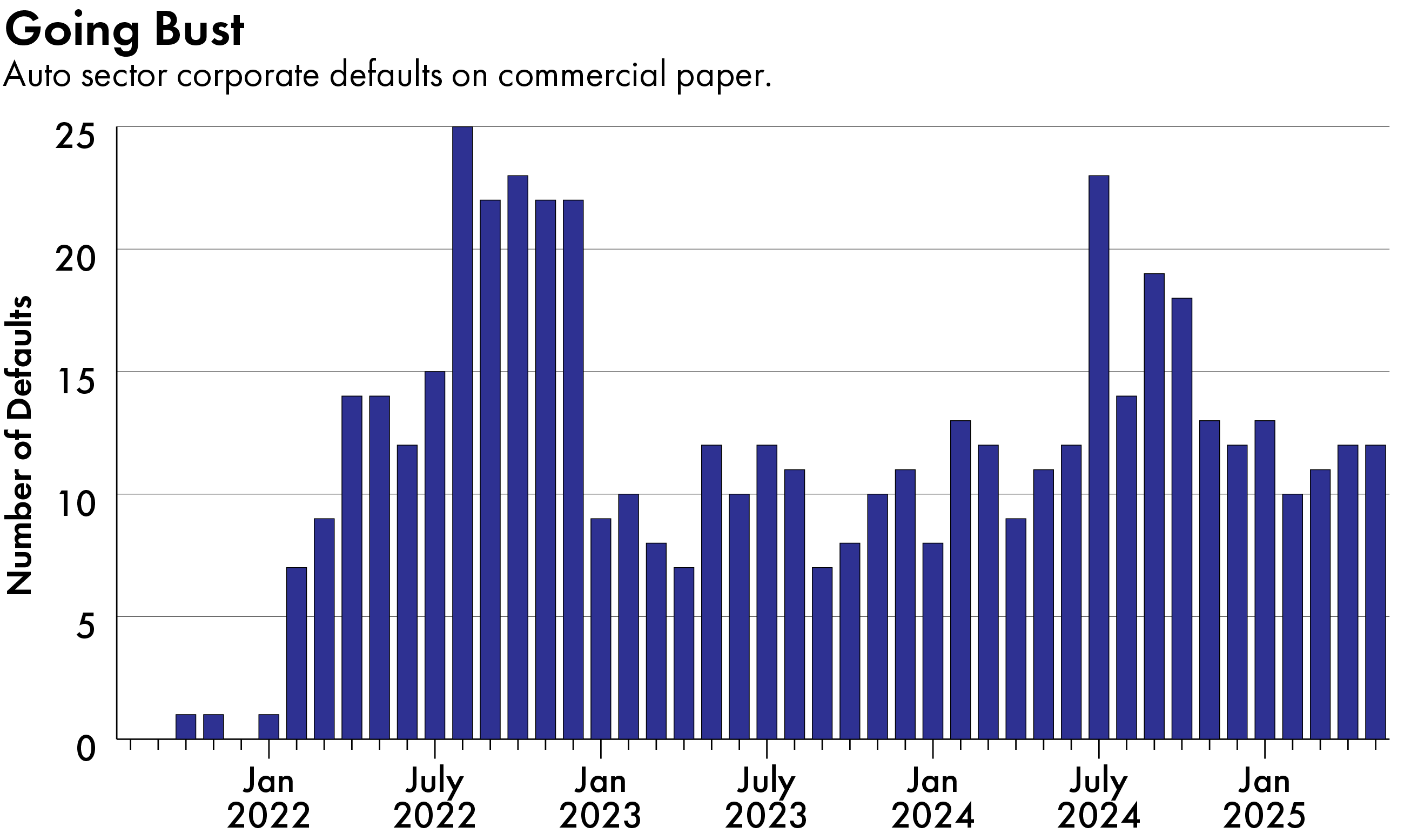

Since the start of 2023, a vicious battle between China’s incumbent and up-and-coming automakers has sent the price of passenger vehicles into a downward spiral. Best-selling cars are on average a fifth cheaper today than they were two years ago. To pay for their war, automakers have deferred paying their bills, squeezing suppliers to the extent that many are teetering on the brink of going bust.

Earlier this month, Beijing stepped in. It summoned major automaker heads in early June, extracting a pledge from them to pay their bills within no later than 60 days. The promise, they hoped, would provide respite for suppliers and perhaps a truce in the price war.

But any truce won’t solve the Chinese auto industry’s deeper problems. Generous subsidies over the last decade planted the seeds that have allowed dozens of upstart carmakers to grow, sparking China’s electric vehicle (EV) revolution. Now, the country is producing too many cars, and even domestic observers say a consolidation and remaking of the industry is long overdue.

“Talking about it as a price war doesn’t really describe the totality of what’s been happening,” says Bill Russo, founder and chief executive of Automobility, a Shanghai based automotive consultancy. “This is a new industrial revolution, and with it comes a changing of the guard. It’s a race to dominance, and if you have to race to the bottom to be dominant, that’s something that Chinese companies are willing to do.”

At stake is the fate of a sector hailed by President Xi Jinping as a pillar of China’s economic future. Xi has spent the last five years trying to reorient the economy away from legacy growth drivers like real estate and towards “new productive forces” such as auto manufacturing and clean energy. Shoring up the financial health of the industry would help to solidify China’s position as a global automotive powerhouse.

The problem is that a web of conflicting interests inside China is getting in the way of a healthy consolidation.

“There’s this fundamental conflict: the central government wants healthy companies, but because automotive employs so many people, the incentives [for consolidation] aren’t aligned at the provincial level,” says Tu Le, managing director at Sino Auto Insights.

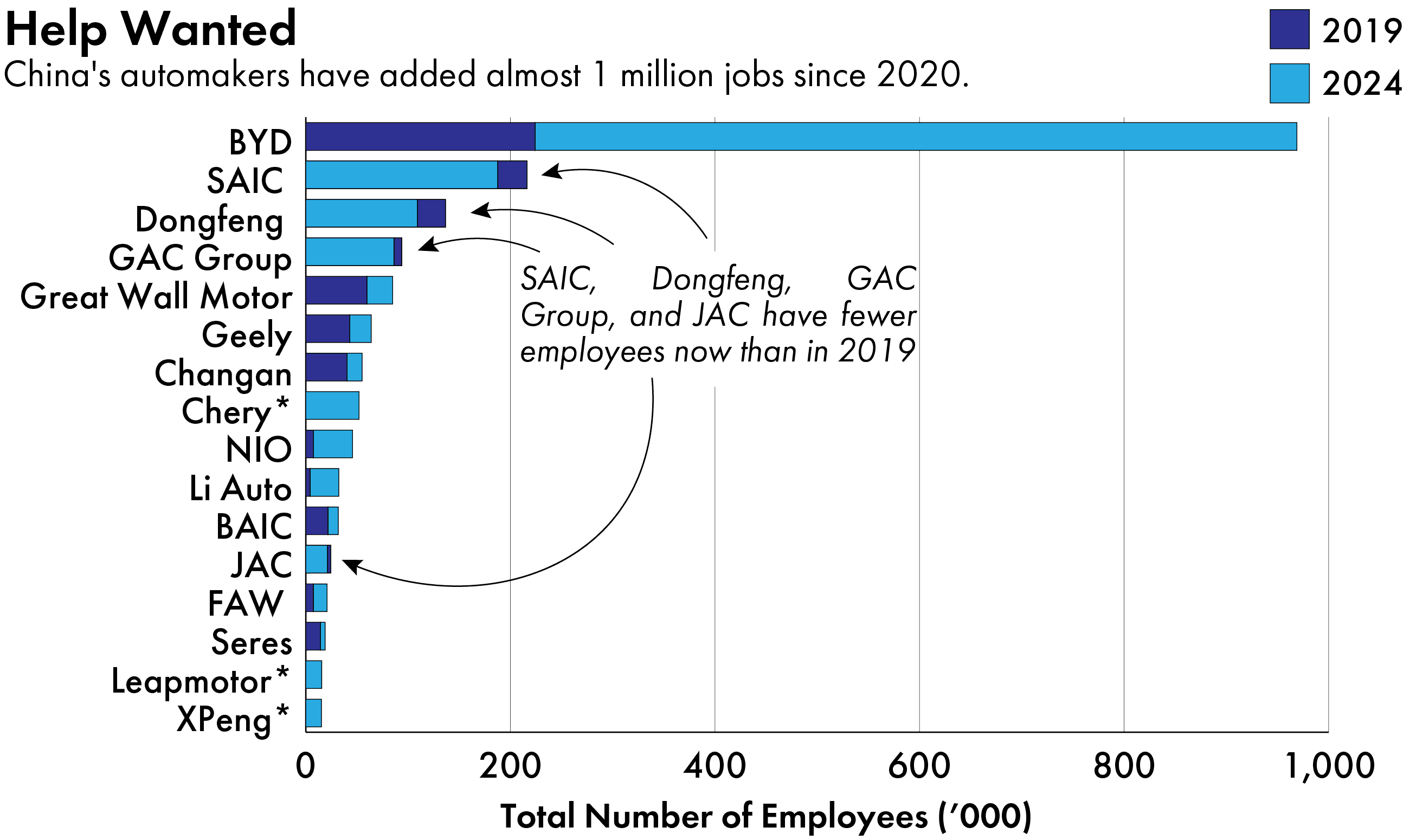

Since 2020, China’s automakers have created close to a million jobs, a review of company annual reports by The Wire found. At a time when China’s economy is slowing, consolidation could force tens of thousands out of employment, a politically costly outcome that local governments desperately want to avoid.

But neither is the status quo sustainable. The average utilization rate of Chinese auto factories was less than 50 percent in 2024, according to Gasgoo Automotive Research Institute, a Shanghai-based think tank. Even then, inventory of new passenger vehicles is stacking up: authorities in Beijing have expressed particular concern over the phenomenon of “zero mileage” vehicles — cars cropping up on the second-hand market with zero miles on their odometers — a sign that automakers are artificially inflating their sales figures.

I think the consolidation would happen faster if there weren’t political sensitivities around the idea of just letting all these guys bleed on the streets.

Leland Miller, chief executive of China Beige Book

Driving the price war has been Shenzhen-based BYD. In late May, it kicked off a fresh round of price cuts after it slashed the price of 22 models by a third. Currently, the price of a BYD Seagull, an entry-level hatchback, starts at just $7,750 within China. The same vehicle is being sold in Europe for more than three times that amount — $26,000.

Observers say that the willingness of BYD — already China’s dominant EV producer with more than a third of the market — to continue to slash prices while embarking on a debt-fuelled expansion is squeezing competitors and its own suppliers alike. In a thinly-veiled shot at BYD this month, Wei Jianjun, chairman of Great Wall Motors, a state-owned competitor, warned that an “Evergrande-style implosion” is on the horizon if the price war continues. Wei was referring to the collapse of China’s largest real estate company in 2024.

“I’m not concerned about BYD being too debt laden,” says Sino Auto Insights’ Le. “It’s that they’re pushing suppliers so hard, that a handful of them waving the white flag has cascading effects.”

Le says that the collapse of a key supplier could ripple across the supply chain, creating unpredictable disruptions that could affect many more producers. He is skeptical that the automakers’ vows of timely payments will last. “The moment an [automaker] or supplier hears an EV company pushed off payments, they’ll do the same thing.”

Analysts say that the only way out of this standoff is for the weakest players in the market to fail. In April, Zhu Xichan, a professor at Tongji University in Shanghai, estimated in widely shared comments that to survive, Chinese automakers must sell at least 2 million units per year.

Currently, only five players in the market fit that criteria: BYD, Geely, SAIC, Changan, and Chery: All of them are legacy brands that were established years, if not decades, before China’s EV boom. Zhu went on to call on China’s newest automotive startups, such as NIO, Xpeng and Li Auto, to “merge, restructure, and cooperate as soon as possible.”

But it is unlikely that China’s EV startups, which have placed heavy emphasis on branding themselves as much as software and technology companies as automakers, will be willing to marry themselves to China’s legacy automakers.

“The tension in China’s system is that the really dynamic, innovative developments in the economy are often driven by more market-driven companies,” says Ilaria Mazzocco, a senior fellow at the Center for Strategic International Studies’ Chinese business and economics program. “The challenge for Beijing is if they went in and started mandating marriages of convenience, they’d risk curtailing that innovation.”

A more likely eventual scenario, Automobility’s Russo says, would see China’s automotive sector divide along two lanes — a “commodity” lane comprised of automakers that focus on high volume, low cost production and aggressive pricing; and a second group of “digital native” automakers such as Xiaomi, Huawei, NIO, Xpeng, Li Auto and others that differentiate themselves based on technology offerings like self-driving and in-car entertainment features.

Left: Xiaomi’s self-driving technology. Right: Xpeng’s automatic remote summons. Credit: Xiaomi, XPENG

“The pyramid will likely consist of a lot of people shopping on price, and a small group at the top shopping on tech,” he says.

Less clear is what will happen to the companies that fail to make it inside that pyramid, given the reluctance from local governments to let struggling automakers fail — as a recent example shows.

The only way you create a healthy automotive space is to take capacity out of the system. That also means the losers need to lose and admit defeat.

Tu Le, managing director at Sino Auto Insights

In April, two of China’s biggest state-owned automakers, Chongqing-based Changan Automobile and Hubei-based Dongfeng Motor, announced they were in advanced talks to merge. By June, however, the two companies had scrapped the effort amid disagreements over where and how to trim their overcapacity.

“To me that’s the canary in the coal mine,” says Le. “Who closes their factories? The only way you create a healthy automotive space is to take capacity out of the system. That also means the losers need to lose and admit defeat.”

State automakers are edging in that direction.

“Before 2023, a lot of the automakers going bust were smaller; but the ones going bust in 2024 and 2025 have been better capitalized,” says Endeavour Tian, a research analyst at Rhodium Group. Recent closures include FAW Jilin and Hycan, two automakers with mixed private and public ownerships, including stakes by state-owned giants FAW Group and GAC Group.

Amid a rise in defaults, Tian estimates that the auto sector has become a net negative contributor (minus 0.1 percent) to China’s GDP growth this year to date. She predicts closures of mixed ownership automakers will continue this year, but it is “hard to imagine any of the SOEs going anywhere,” she says. “It will really depend on how hard Beijing wants to facilitate consolidation, and so far I’m not seeing many of its efforts paying off.”

Or, as Leland Miller, chief executive of China Beige Book, puts it: “I think the consolidation would happen faster if there weren’t political sensitivities around the idea of just letting all these guys bleed on the streets.”

Rachel Cheung contributed reporting.

Eliot Chen is a former staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen