President Trump’s State of the Union demand that Congress repeal the CHIPS Act — which allocated over $50 billion to support the U.S. semiconductor industry — has reignited a familiar lament in Washington: if only the U.S. could match Beijing’s long-term commitment to industrial policy. But this view overlooks a crucial reality. China, too, struggles to craft and implement coherent national strategies for its critical industries.

Conventional wisdom paints China as a Communist monolith that has mastered industrial policy. The popular narrative goes like this: Beijing identifies a strategic sector, mobilizes vast capital, issues top-down mandates, and watches as state-owned enterprises and local governments fall into line. This is the story often told to explain China’s stunning rise in electric vehicles. With generous subsidies, coordinated infrastructure investments, and aggressive procurement policies, the state orchestrated a transformation that vaulted domestic champions like BYD and CATL to global leadership.

Compared to the United States — where political priorities shift with each election, funding faces constant threats, and states set economic policies fully independently of Washington — China’s model may seem enviably effective.

This image is incomplete, however. Our research into China’s semiconductor sector shows how the very same industrial policy machine underperforms when its constituent parts don’t align.

Despite pouring tens of billions of yuan into the chip sector — especially through the National Integrated Circuit Industry Investment Fund, or “Big Fund” — China has struggled to make headway in the semiconductor manufacturing equipment (SME) sector upstream to chipmaking. Downstream chipmakers and designers like SMIC and Huawei have made progress to loud media acclaim, but China’s upstream capabilities remain heavily reliant on foreign chipmaking tools. This reliance is particularly problematic in light of Washington’s tightening export controls, which in 2022 and 2023 sharply curtailed China’s access to advanced lithography and other high-end equipment.

The usual explanations for China’s struggle to catch up in chipmaking equipment are familiar: semiconductors are uniquely complex and globalized, China is far behind, and U.S. restrictions have raised the bar China must reach. These factors, however, don’t fully explain the country’s persistent underperformance.

True technological leadership demands more than ambition and capital. It requires coordination between national and local governments, synergy between the public and private sectors, and strategic patience to translate policy into tangible results.

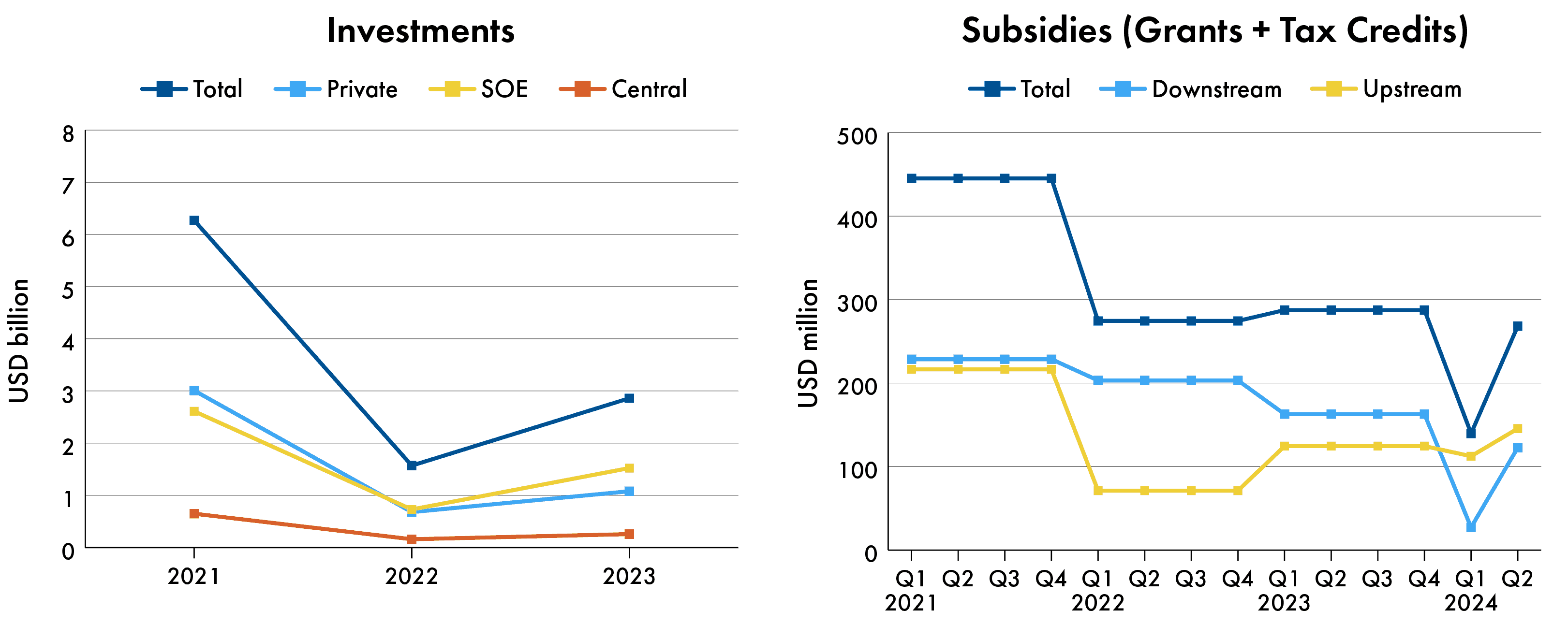

We compiled and analyzed Chinese semiconductor companies’ financial disclosures to estimate, for the first time, the total governmental investment and subsidies directed at China’s chip equipment sector. The data points to a deeper, structural issue: industrial policy works best when it catalyzes coordination — across central government, state-owned enterprises (SOEs), local authorities, and the private sector. In semiconductors, this alignment has been lacking.

Strikingly, our data suggests that U.S. export controls have influenced the central government’s decision to subsidize more than they have affected companies’ decisions to develop indigenous alternatives. Ultimately, it was the pandemic’s economic fallout and the resulting fiscal squeeze on local governments — not industrial policy per se — that has most shaped China’s semiconductor response to U.S. competition.

Here are five key stories the data tells:

Beijing has deep pockets, but local governments are running on empty

Investment in semiconductors dipped in 2022, coinciding with China’s final year of stringent zero-COVID policies.

Equity investments from the central government and state-owned enterprises into chipmaking equipment companies dropped from $3.2 billion in 2021 to $900 million in 2022. Government grants plunged to one-seventh of their 2021 levels, while tax credits shrank to two-thirds. This downturn was less about U.S. export controls and more about tightening fiscal conditions at home — local governments, burdened with mounting debt, simply had less to give.

Beijing’s megaphone doesn’t always echo: SOEs turn a deaf ear

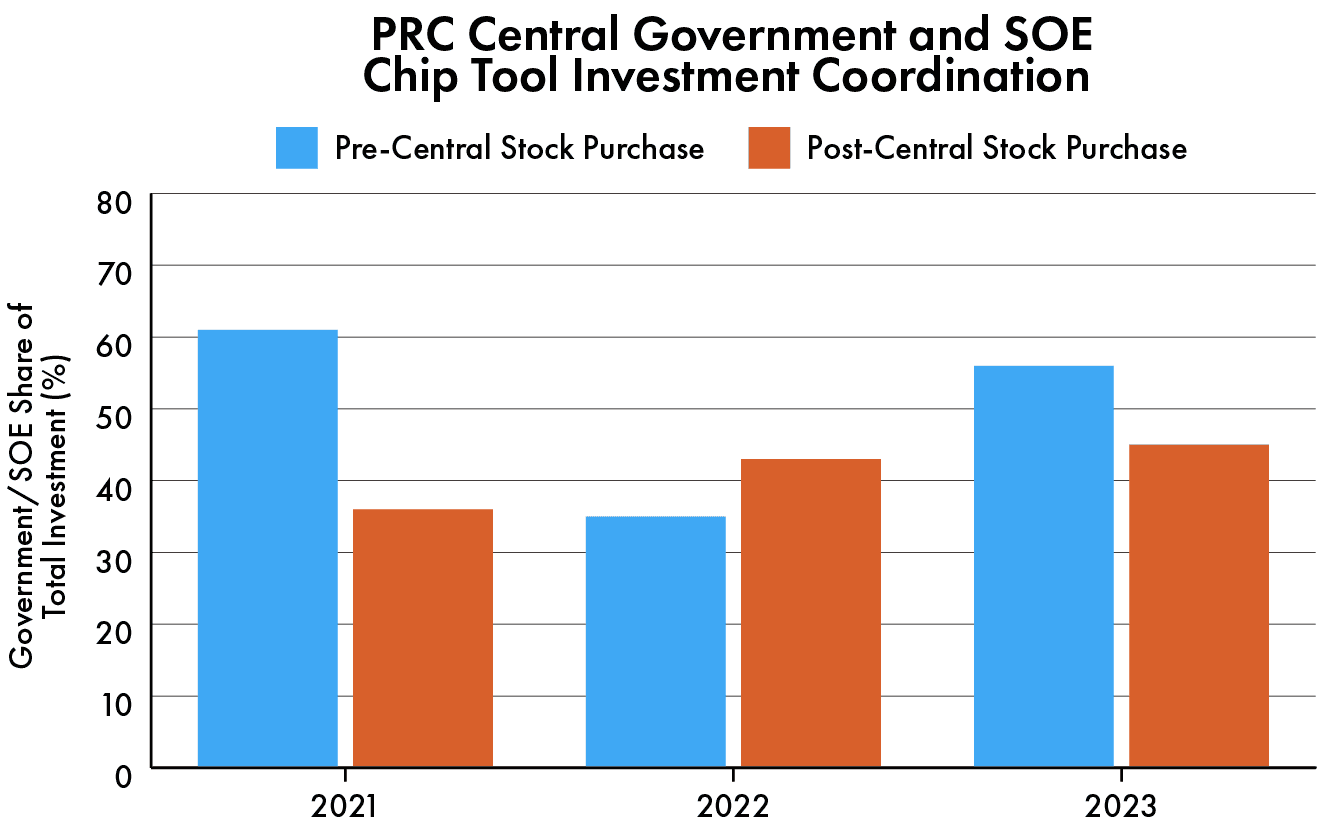

A striking feature of China’s semiconductor push is the disconnect between central government investments and the behavior of state-owned enterprises (SOEs). In past industrial campaigns, Beijing’s directives sparked synchronized investment at multiple levels of government and industry.

For example, in the EV industry, when the central government rolled out generous national purchase subsidies and R&D funding programs, local governments echoed these efforts by building out charging networks.

But in semiconductors, the response has been uneven. Analysis of three years of countrywide investments shows no correlation between the central government’s investment targets and where SOEs chose to invest.

This divergence underscores a broader trend: Beijing’s ambitions do not always translate into action on the ground. Local governments, often cash-strapped and focused on near-term economic stability and parochial employment concerns, have been hesitant to rally behind central directives. The semiconductor sector has been no exception.

The result? A semiconductor industry where investment decisions are shaped as much by provincial budget constraints as by national strategy.

Carrot over curiosity: External incentives, not internal drive, shape R&D

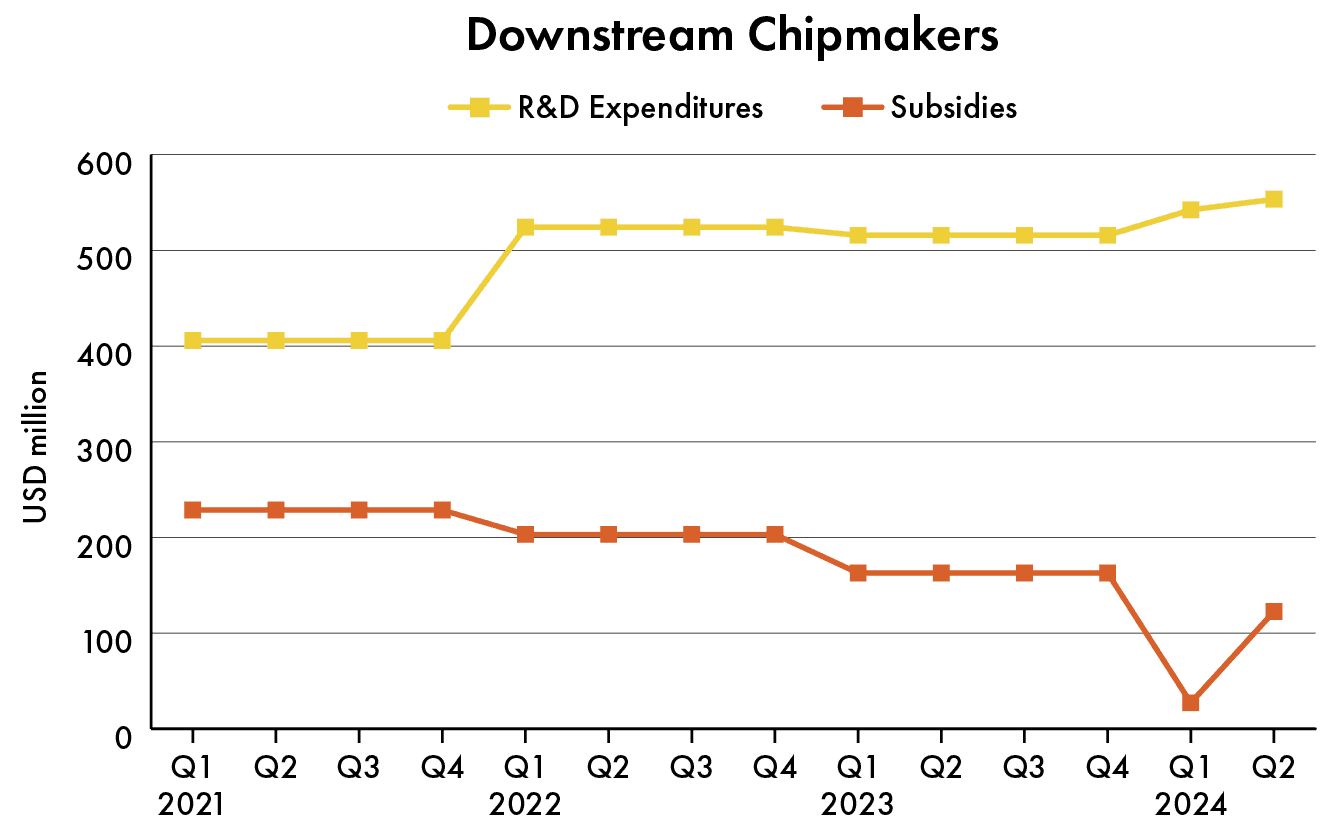

China’s semiconductor ecosystem has a clear divide: upstream semiconductor manufacturing equipment (SME) firms have more catching up to do, while downstream chipmakers are more globally competitive. But how firms respond to these challenges depends on incentives, not just the pressures of catching up with the U.S.

Upstream SME firms’ R&D expenditures closely follow government subsidies and investments. When funding dipped in 2022, so did their R&D. When subsidies partially rebounded in 2023, R&D spending followed. The takeaway? Chinese SME firms innovate when financially supported, not purely in an independent effort to replace Western toolmaking competitors.

By contrast, downstream chipmakers showed little response to either subsidies or U.S. restrictions. Their R&D spending rose in 2022 and then plateaued in 2023, suggesting that broader industry forces — rather than government incentives — shape their innovation strategies. If Washington expected its export controls to light a fire under China’s chip industry, the data suggests otherwise. Domestic policy, not foreign pressure, is steering the ship.

Playing to the home crowd

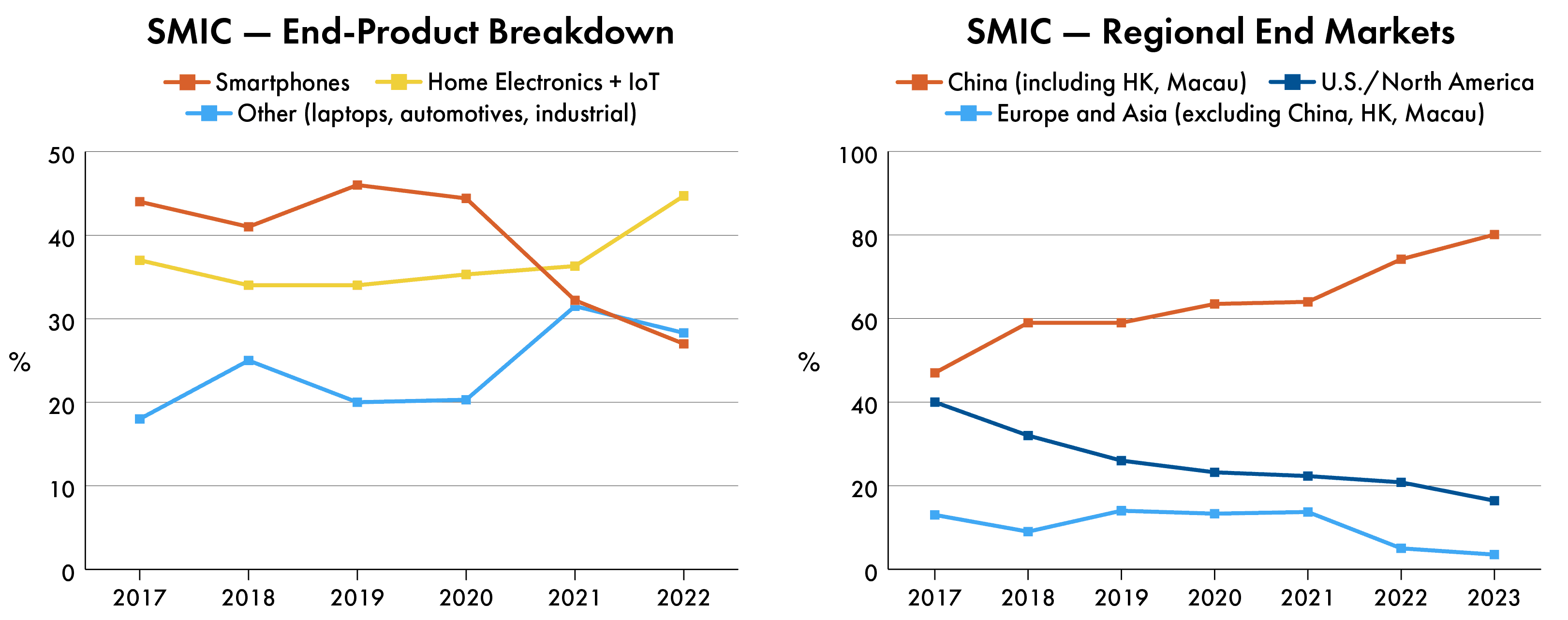

While upstream firms followed the money in R&D, downstream players pivoted their market and product strategies. Semiconductor Manufacturing International Corporation (SMIC), China’s largest foundry, saw its domestic sales share climb by a third over three years. Simultaneously, its product focus tilted further toward smartphones.

This shift is downstream of both U.S. export controls and Beijing’s industrial policies. Washington’s restrictions on chip sales to Huawei forced domestic firms to rethink supply chains, while Chinese government subsidies encouraged local sourcing. The result: a semiconductor market that is increasingly inward-looking, reinforcing self-reliance rather than accelerating technological breakthroughs.

Beijing’s semiconductor challenge — coordination, conditions, and constraints

China could accelerate its technological catch-up by fixing what’s broken at home — bridging central-local policy gaps and better incentivizing private-sector research. A top-down funding blitz might spur spending, but it takes more than money to engineer true breakthroughs.

Both the Trump administration and its detractors would do well to note this. Consistent federal signaling that America wants to remain a leader in chip technology is important. But writing a single $50 billion check with the CHIPS Act is not enough. True technological leadership — whether in Washington or Beijing — demands more than ambition and capital. It requires coordination between national and local governments, synergy between the public and private sectors, and strategic patience to translate policy into tangible results.

There are signs that Beijing policymakers may be starting to recognize the limits of their current approach. Early signals suggest that the next phase of China’s flagship chip investment vehicle — commonly referred to as Big Fund 3.0 — could focus less on simply injecting capital and more on improving coordination. State planners have hinted at new bureaucratic structures aimed at better aligning national goals with local execution, encouraging provincial governments to “adapt to local conditions.” There is also talk of repositioning SOEs from top-down executors to more flexible coordinators and enablers.

Recent policy documents further emphasize the importance of private enterprise in driving innovation, with the state potentially stepping in to fund basic research, support talent pipelines, and de-risk early-stage technologies that lack immediate commercial payoff.

If these signals point toward a correction of China’s semiconductor policy coordination problem, they could catalyze the Chinese chip industry’s catch-up. American policymakers should watch these trends both for the competition they portend and for the lessons on effective industrial policy they impart.

Lizzi C. Lee is a Fellow on Chinese Economy at the Asia Society Policy Institute’s (ASPI) Center for China Analysis (CCA). She is an economist turned journalist, and graduated from MIT’s Ph.D. program in Economics before joining the New York-based independent Chinese media outlet Wall St TV.

Arrian Ebrahimi is a JD candidate at Georgetown Law and the author of the Chip Capitols newsletter. He previously worked at the Semiconductor Industry Association and TSMC, and he studied in Beijing for two years as a Yenching Scholar.