China today confronts a whirlwind of economic and geopolitical challenges: slowing growth rates, looming demographic decline, mounting debt levels, and a post-Covid confidence funk. Just five years ago, many were proclaiming the inevitable ascent of China. Today’s tune is different, with analysts asking: has China “peaked?”, and predicting Beijing seeks to reclaim Taiwan before its window of opportunity slams shut.

This view is increasingly dominant in policy and military circles — but it’s wrong. While China’s prospects have dimmed over the past few years, it is still closing the relative power gap with the U.S., albeit less quickly. A China that last year grew twice as rapidly as the United States will continue to see greater marginal gains in economic and, subsequently, military capacity.

Far from facing a window of opportunity within the decade, Xi Jinping benefits from biding his time. The danger is that U.S. policymakers, mistakenly believing that Xi is a man in a hurry, may adopt an emergency posture that provokes the very war they hope to deter.

Possible Peaks

Claiming China has serious problems is obvious and uncontroversial. But the relevant question is comparative: Are the challenges protracted enough to cost China its chance of passing the U.S.? This depends on what is meant by a country’s “peak.”

To say an economy has peaked has three possible meanings. The first is an “absolute peak.” Political scientists Hal Brands and Michael Beckley speak of a China that has “stalled or turned around entirely,” which brings to mind a car race with one participant stuck in the mud. In such a race, this absolute peak would mean the lagging car — China’s — had not only slowed relative to its competitor but stopped advancing altogether.

The second is a “relative” peak, which would show both cars still moving forward on the road, but with the gap between them widening, as the car once on track to overtake the leader now slips further behind.

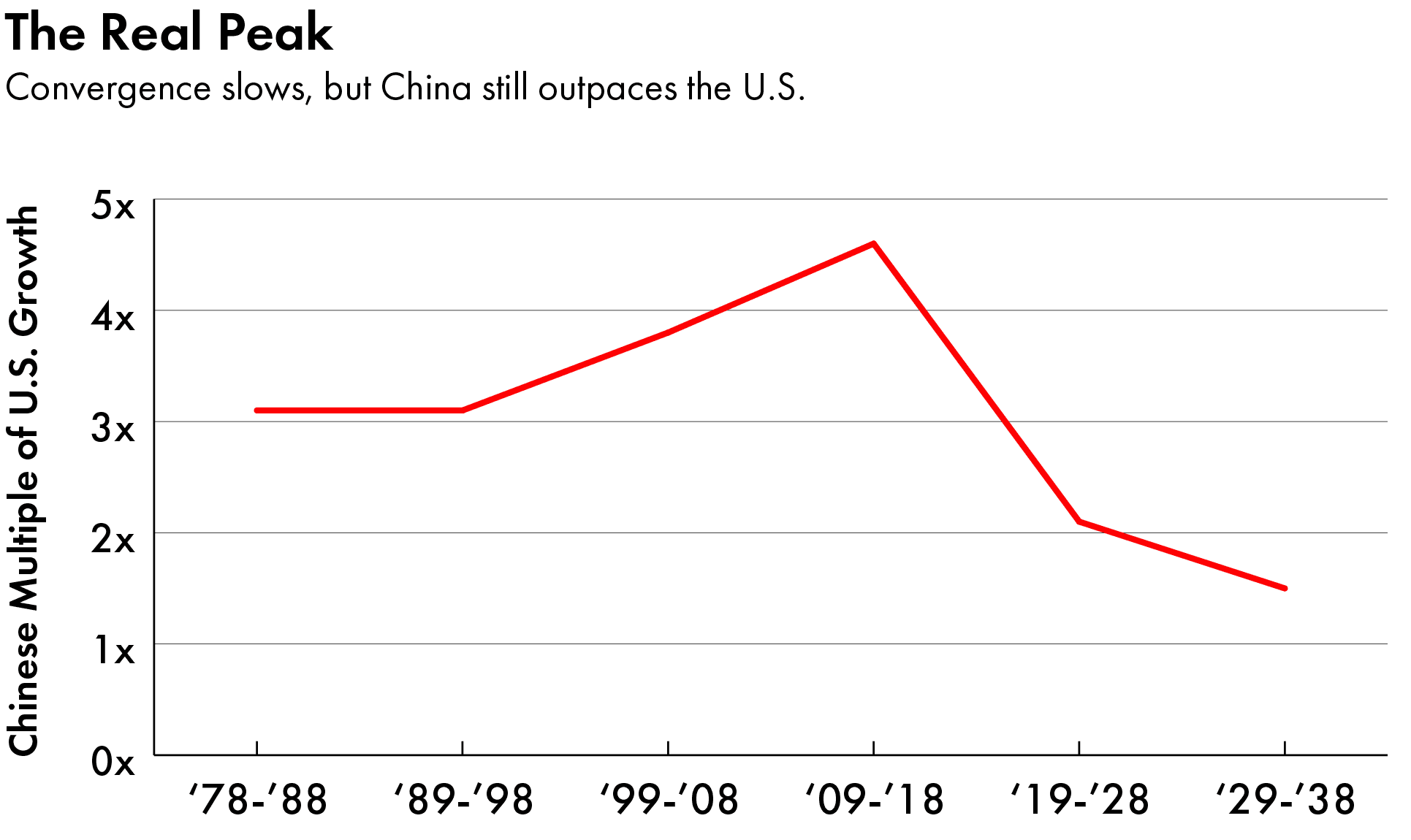

A third possibility is that the Chinese car is still gaining on the U.S. car — but at a slower clip than before. This distinction carries significant implications for the future of the rivalry. Unlike an absolute or relative peak, the second-place car is still slated to overtake its competitor, just over a longer time horizon. This last concept, which we call a “peak in the rate of convergence,” most closely describes the U.S.-China relationship today.

Slower, But Still Faster

China’s rate of convergence with the U.S. reached its highest point in the 2010s, when its double-digit growth was almost five times faster than its American rival. Now, China is only growing twice as fast and is projected to slow further to only 1.5 times the rate of the U.S. in the 2030s. This means that China has “peaked” in one sense — its rate of convergence has declined markedly and will continue to decline — but that this actually occurred over a decade ago.

Yet even a slower pace of Chinese convergence will still narrow the gap with the U.S., which is expected to see its own growth decline to 1.5 percent in the 2030s. China’s 2023 growth rate of around 5 percent is indeed a far cry from a decade ago, but the last time the U.S. managed back-to-back years of 5 percent growth, the Vietnam War was still in full swing.

China continues to benefit from the catch-up growth opportunities of a developing economy. Its likely trajectory — growing over 50 percent faster than the U.S. for the next 15 years — would hardly constitute the “violent descent” Brands and Beckley describe. China’s problems are also not time bombs which will inevitably detonate within the decade and force panicked adventurism, but rather long-standing, chronic conditions that policymakers will try to offset.

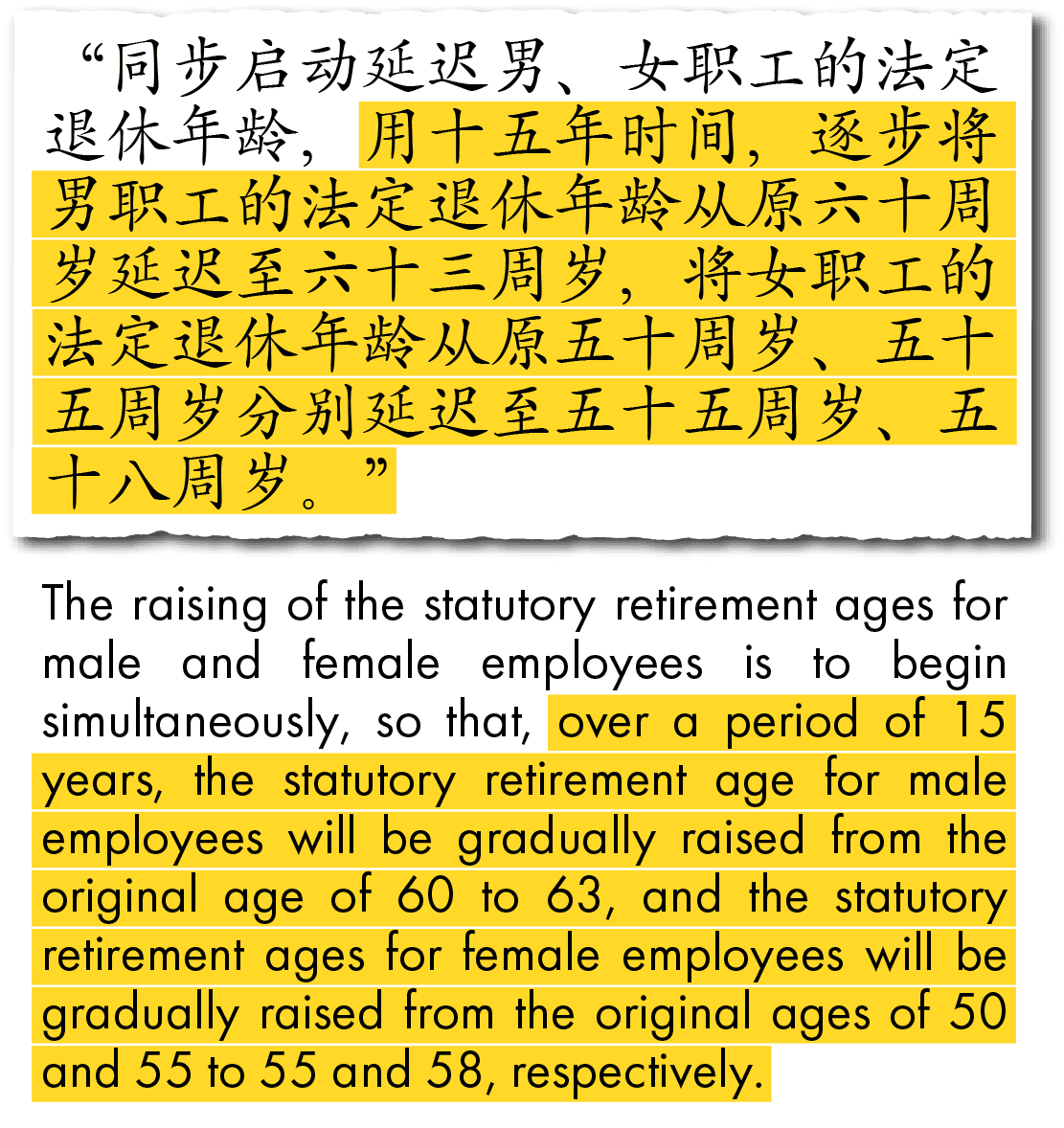

While the intensity of China’s slowdown has been jarring, the overall trend was foreseeable. In the early 2010s, China’s labor supply began to shrink, urbanization slowed, and its debt buildup kicked into high gear — classic ailments for developing economies transitioning into mature ones. Even so, China’s population still has a small bulge — children today aged five through fifteen — ensuring that in the near term, demographics remain a gentle headwind rather than a drastic drop-off; and one that Beijing could offset by loosening hukou restrictions or raising its unusually low retirement age of 55 for women and 60 for men, in step with recent policy announcements. Alarming youth unemployment levels require context meanwhile: China minted 10 percent more bachelor’s grads in 2022 than the year before, and 50 percent more than a decade ago, many of whom are STEM students — offering significant upside for a country pivoting to a technology-driven growth model.

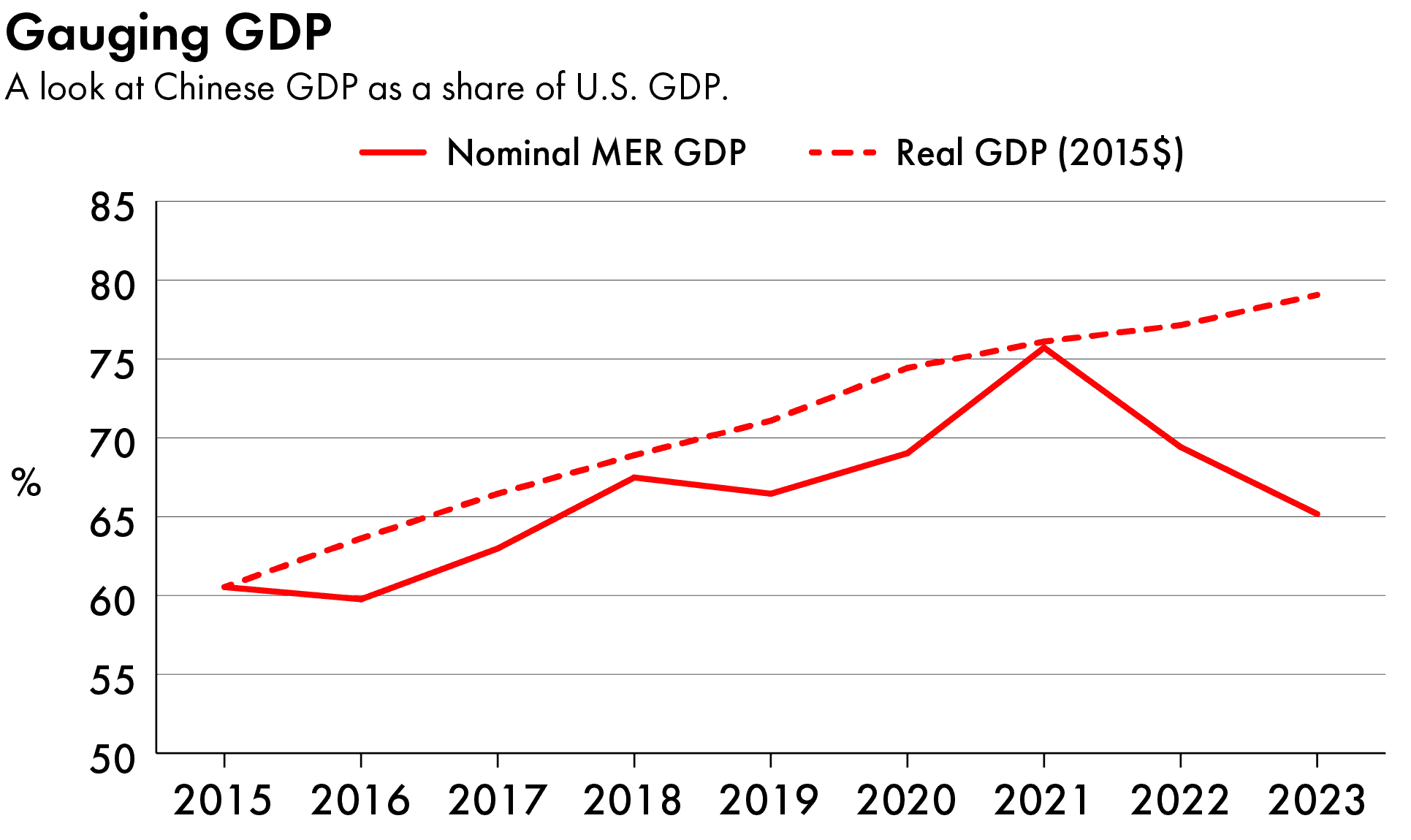

Some “Peak China” proponents also understate China’s recent growth and overstate the U.S.’s by relying solely on GDP at market exchange rates (MER), which is warped by big swings in currency value and unadjusted for inflation. This gives the misleading impression that since 2021, China’s nominal GDP has shrunk relative to the U.S.’s. In real terms, China’s economy is 20 percent larger than before Covid, and the U.S.’s only 9 percent larger.

One truth about Beijing’s less rosy future is worth conceding: China’s slowdown circumscribes an economic trajectory that had previously appeared limitless, relieving U.S. strategists of nightmares about facing down a rival with double the U.S.’s GDP. Contrarily, forecasts from leading institutions suggest China’s economy being somewhere between 20 percent bigger and 20 percent smaller than the U.S.’s in the 2030s and 2040s. Shifts in the relative power balance will instead be driven by how effectively each state converts comparable economic resources into technological or military advantage; who we crown the economic “number one” becomes mostly a matter of bragging rights.

An Ascendant Military

Economics are the superstructure for other elements of national power: a larger economy means a larger defense and R&D budget, and more latent industrial capacity that can be converted into military might. In the military realm there are structural reasons to think China is closing the gap with the U.S. even faster than GDP figures suggest.

[Xi] believes in his bones that China is destined to keep rising, and that its hand will continue improving, as it has for the past fifty years. It is up to American strategists to prove him wrong.

As the world’s sole superpower, the U.S. military is dispersed all over the world, with 750 military bases across 80 countries. In contrast, China’s military forces are concentrated in East Asia and postured for local scenarios, such as a war over Taiwan.

Such a fight would take place in China’s backyard, while the U.S. would be projecting force 7,000 miles from the American homeland. China has built the world’s greatest “anti-navy,” designed to keep the U.S. from getting close. In doing so, it gets more bang for its defense bucks, relying on thousand-dollar missiles to sink billion-dollar American carriers and destroyers.

And even if China’s economic contractions did become more serious, it has the means to avoid a peak in military power. As Oriana Skylar Mastro and Derek Scissors have argued, “flagging economic prospects take time to affect defense.” The planes, ships, and missiles bought now will serve for decades into the future, even if budgets decline. Consider that our Navy scours the ocean with submarines from the 1980s, the backbone of the U.S. strategic deterrent are ICBMs built in the 1970s, and our most prolific class of bombers took flight in the 1950s.

China’s industrial power, the backbone of military strength, is also trending positively. China produces 18 percent of the world’s GDP but accounts for 30 percent of manufacturing. Xi’s preference for the “real economy” impairs consumers, internet companies, and the financial sector, yet avoids a Western-style “hollowing out” of manufacturing capacity — the lifeblood of military ambition. The Department of Defense projects that China’s shipyards — with 200 times more capacity than America’s — will fuel a naval buildup widening China’s lead in battle force vessels from 44 ships to 150 ships. China also dominates military-adjacent hard technologies like drones and 5G that rely on cost-efficient production at scale.

Taiwan Troubles

Central to the “Peak China” contention is not just that China’s economic heyday is over, but that leaders will feel in a hurry. But more important than the assessments of American analysts is the view in Beijing. If Chinese policymakers do not perceive their power to have reached its apogee, they are unlikely to act as though they’re on a deadline.

Wang Huning at the 14th National Committee of the Chinese People’s Political Consultative Conference, March 11, 2023. Credit: CCTV

Clues suggest China is bullish on its relative prospects. Xi has consistently proclaimed that “time and momentum are on our side.” While he has incentives to project optimism, his more recent slogan, “the East is rising and the West is declining,” is rooted in China’s cultural belief that it is destined to rise relative to the West, recovering from the “Century of Humiliation” to regain its rightful pedestal. Xi’s sloganeering is done by Wang Huning, the CCP’s ideological architect, known for a book in the 1990s predicting that “the American system…[will lose] to systems based on collectivism.” His continued promotion suggests his views still hold currency.

A lack of urgency is deeply entrenched in CCP thought: as Mao Zedong told Henry Kissinger 75 years ago that “we don’t need them now. We can wait 100 years.” Provided that Xi sees that the door to reunification has not closed, he will not seek to instigate an invasion that wargames show would very possibly fail and existentially threaten his regime.

Preparing for China’s Future

The question of whether China has peaked is no mere definitional quibble, but fundamentally determines which strategies make sense for American policymakers.

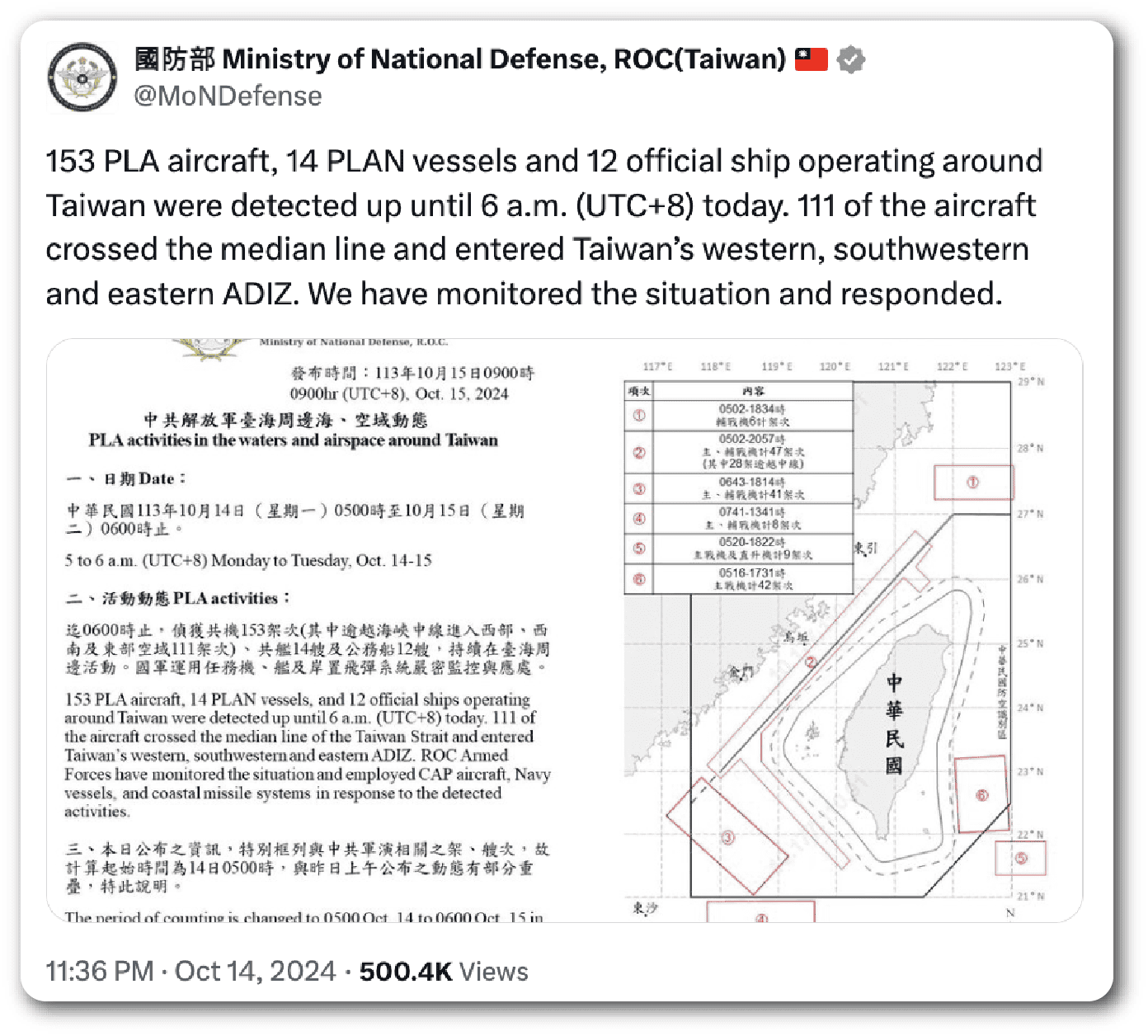

Credit: @MoNDefense via X

If Xi really had set his clock to attack Taiwan within the next five years, for American policymakers to not move heaven and earth to stop him would be gross malpractice. Yet, given China’s long runway and Xi’s patience on Taiwan, such policies may instead court disaster. Pulling Taiwan further into America’s orbit will confirm China’s worst fears: that maximalist U.S. support is less about peace in the Taiwan Strait than incrementally pursuing Taiwan independence. Xi may then feel forced to think seriously about an attack to arrest a rapidly deteriorating situation. The best way to ensure Beijing chooses violence is to convince it that non-violent means are off the table.

The real lesson from the Cold War is that great powers are slow to get knocked out of the ring. At its outset, the most prescient analysts were well aware of deep Soviet economic weaknesses Yet as George Kennan foresaw in 1947, even an economically enfeebled USSR would be capable of showing the “greatest outward brilliance at a moment when inner decay is in reality farthest advanced.” With China, whose economy is already nearly as large as America’s and still gaining, the prospects of a fast inflection point reflect wishful thinking.

Rather than worrying about sudden rises or precipitous falls, the U.S. should plan on China being here for the long haul. Xi sees no need to push in his chips for an “all-in” gamble. He believes in his bones that China is destined to keep rising, and that its hand will continue improving, as it has for the past fifty years. It is up to American strategists to prove him wrong.

Bailey Marsheck is a Non-resident Scholar at UC San Diego’s 21st Century China Center and MPP candidate at Yale University, where he focuses on international and development economics. He holds a master’s degree in China Studies from the Yenching Academy of Peking University and previously worked as a researcher at the Harvard Kennedy School’s Belfer Center.

Raphael Piliero has served as a researcher at the Harvard Kennedy School’s Belfer Center for Science and International Affairs, a Fulbright scholar to Taiwan, and a research assistant at the Atlantic Council. He holds a bachelor’s degree in government from Georgetown University.