One Friday evening last October, U.S. President Donald Trump reignited the trade war with China. In doing so, he also inadvertently triggered the largest meltdown in the history of the cryptocurrency industry.

Trump announced new 130 percent tariffs against China on October 10, in response to China’s plans to tighten restrictions on exports of critical rare earths. China responded that it was ready for a prolonged battle. “If you wish to fight, we shall fight to the end,” China’s commerce ministry said in a statement.

The end came quickly as Trump and Xi smoothed things over at a summit in Busan weeks later, but not quickly enough for crypto markets.

Within minutes of Trump’s post, Bitcoin fell 14%. The ensuing rout erased more than $500 billion in crypto markets, making it the largest wipeout in the industry’s history.

A continued sell-off roughly doubled those losses in the weeks that followed, and the crypto world still hasn’t recovered. Six months later, Bitcoin is trading at half its October highs. In crypto circles, the October wipeout is now known by its own shorthand, 10-10.

“A trillion dollars just vaporized. It was insane,” says Lee Reniers, a lecturing fellow in cryptocurrency policy at the Duke Financial Economics Center.

A crypto sell-off after Trump restarted the trade war with China was not necessarily surprising. What stunned traders was the size and speed of the fall.

Because Trump’s announcement was made outside traditional stock-market trading hours, the sell-off was concentrated in 24-7 crypto markets. Adding to the jitters was an ongoing U.S. government shutdown, said James Butterfill, head of research at digital asset manager CoinShares.

But Butterfill and other analysts pointed to a more important factor behind the crash: leverage.

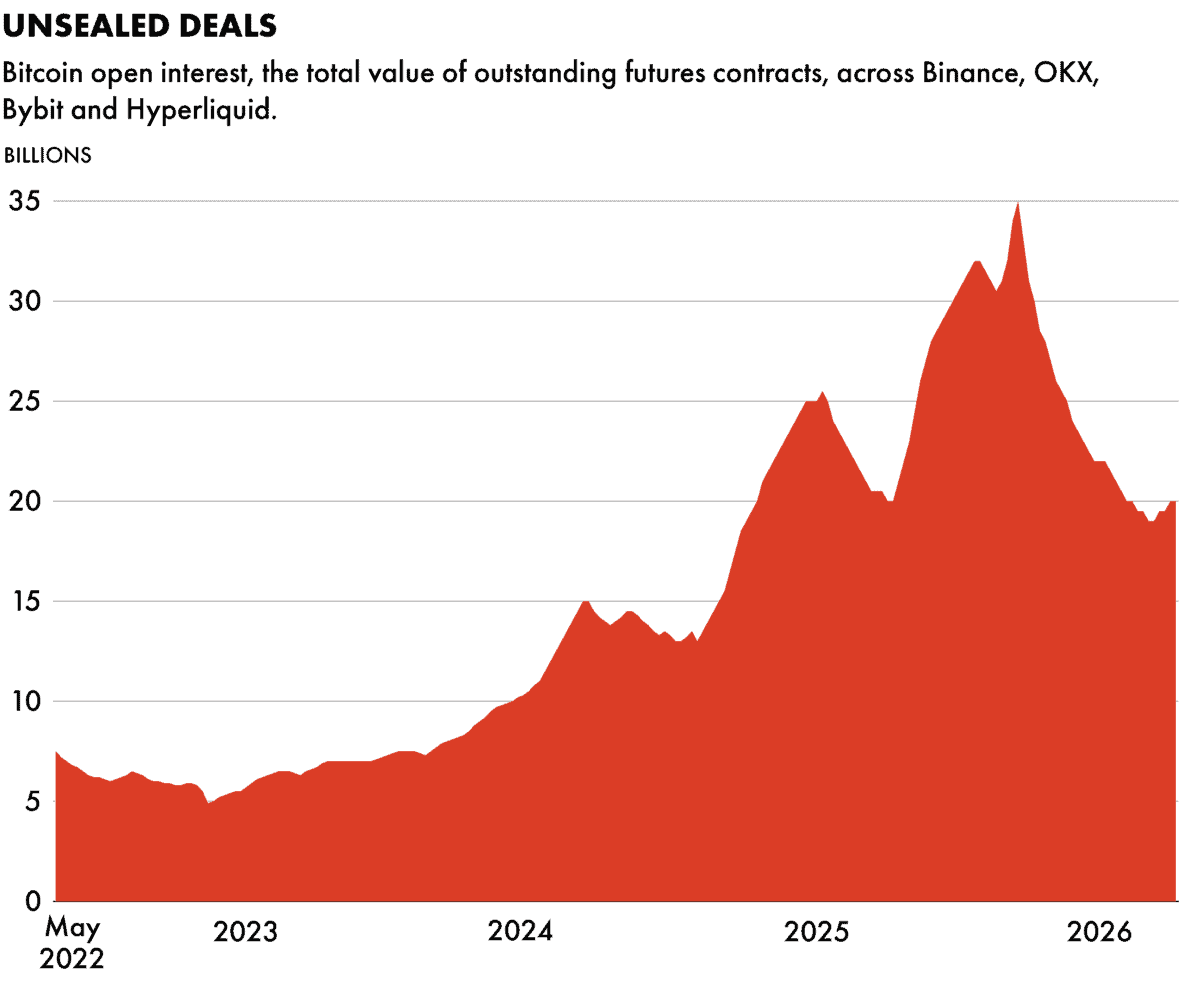

In the months before Trump’s post, borrowing by crypto investors had surged to record levels. One key gauge is Bitcoin open interest, which tracks the total value of outstanding derivatives bets on the token’s price. By early October 2025, Bitcoin open interest had climbed to nearly $120 billion, an all-time high and more than double its level a year earlier. In January 2024 it had stood at about $20 billion.

As crypto prices fell, liquidation thresholds were triggered. For example, a trader who went long on Bitcoin futures by borrowing up to 100 times his or her capital could have a position wiped out by even a small decrease in the price of Bitcoin, forcing the exchange to liquidate their holdings. Some exchanges offered investors leverage of up to 1,001 times.

Those forced sales pushed prices lower, triggering more liquidations in a feedback loop that cascaded through the market, says Emiliano Pagnotta, associate professor of finance at Singapore Management University. “The people who get liquidated first trigger further price movements. That creates escalation: the liquidation cascade. In combination with the thin liquidity you have for most [crypto tokens], that can create a disaster scenario.”

“IT PUTS YOU BACK IN 1929”

Chinese entrepreneurs played a central role in building and popularizing the highly leveraged crypto tools that now dominate global markets. They sold them to the world after the Chinese government decided they posed too much risk for its own citizens. As these tools become mainstream, the question now is what risks these leveraged crypto products pose to global financial markets. Are they, as some believe, a ticking time bomb in the global financial system?

In total, on 10-10 $19 billion in leveraged positions evaporated in under 24 hours – the largest such wipeout in the industry’s history. The slide caught major exchanges such as Binance, founded by Canada’s Changpeng Zhao, off-guard. Complaints flooded in from customers and competitors that the exchange did not allow users to withdraw funds during the downfall.

Binance said it experienced technical glitches during the crash and offered customers over $600 million in payouts in following weeks.

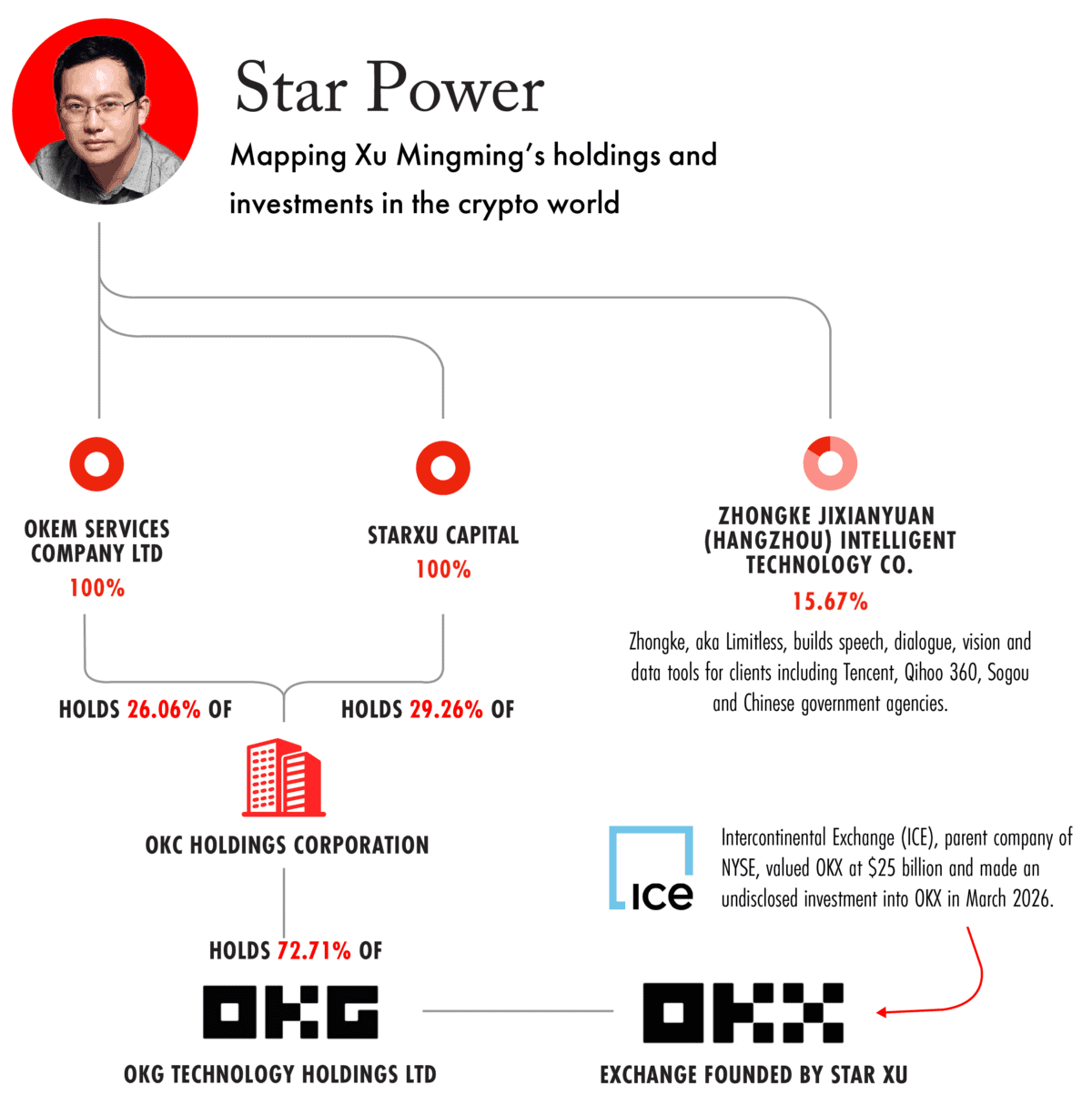

Star Xu, founder of Binance competitor OKX, later disputed Binance’s characterization of the event. In a January post, Xu wrote the crash was “no accident”. “10-10 was caused by irresponsible marketing campaigns by certain companies,” he said.

Xu said Binance marketed a new token, called USDe, that offered 12 percent annual yields and presented it as a safe, stablecoin-like asset but with more upside. In reality, Xu added, the token was tied to risky leveraged trading strategies. So when markets turned, Xu said, USDe’s value plummeted and contributed to a broader wipeout.

OKX and Binance both declined The Wire China’s requests for comment on this and other disagreements between Xu and Zhao, or to arrange interviews with them.

But to many in crypto, the episode was just another bout of volatility — albeit a particularly painful one — in already unstable markets. They say the crash usefully exposed irresponsible borrowing and will ultimately strengthen the industry.

“A lot of leverage was washed out. It’s a good thing,” says Adam Morgan McCarthy, senior analyst at crypto research firm Kaiko.

Crypto skeptics disagree and see the event as an important warning. They say it is fortunate that, for now, crypto is insulated enough from the traditional financial system that even its most violent crashes do not cause significant disruption elsewhere. But as the U.S. formalizes crypto regulation and large financial institutions enter the market, critics believe that future crypto crashes could put pensions at risk and ripple through the global economy.

“Before you’d have these crashes and maybe some spillover to normal financial markets, but once you mainstream [crypto], that spillover could be a lot more costly to everybody,” says Reniers.

The amount of leverage in crypto markets is especially concerning to scholars like Arthur Wilmarth, a law professor at George Washington University, who warns that the global financial system may be sleepwalking into a crypto bubble collapse on par with the 2008 global financial crisis or the stock market crash of 1929. Wilmarth refers to the former scenario as “Subprime 2.0”.

“There are many echoes between crypto and past financial crises: the leverage, the number of vehicles that are making the same bets on the same assets,” says Wilmarth. “Leverage is going through the roof … it basically puts you back pretty much in 1929.”

FROM THE MARGINS TO THE CENTER

In 2012 Star Xu, or Xu Mingxing, learned about Bitcoin while watching an episode of the legal drama The Good Wife, which featured a fictionalized court case pitting the creator of the then-nascent digital currency against the U.S. Treasury Department.

Xu, then 28, had worked at Yahoo China and served as chief technology officer at a document-sharing platform, DocIn.com. Xu began buying and trading Bitcoin when it was worth around $20, but was unsatisfied with the trading platforms available to him. In 2013, he founded OKcoin with a mission to provide better customer service, faster deposit and transaction speeds, and more liquidity.

Crucially, Xu followed the lead of competitor Huobi (now called HTX) in waiving transaction fees, a move that distinguished Huobi and OKcoin from most other crypto exchanges at the time. Xu attracted a large following of Chinese retail traders, who quickly came to dominate global retail trading. By March 2014 almost 80 percent of all crypto trades were transacted in renminbi.

Before founding Binance, Zhao was OKX’s chief technology officer. While at OKX in 2014 he told CoinDesk: “There is not much else one can invest in [in China]. This, combined with the increase in buying power — people naturally look to bitcoins.”

Following a dispute with Xu, Zhao left OKX the following year. In a feud that continues to this day, Zhao alleged that Xu used bots to boost trading volumes, while Xu accused Zhao of fabricating his credentials. Amid the release of Zhao’s new memoir, the pair have continued to trade allegations regarding Zhao’s time at OKX.

Xu soon discovered that Chinese traders had strong appetites for leverage. They gathered on WeChat and other platforms, egging one another on to make ever-riskier trades. By 2014, OKX was lending its users up to three times their initial investment for margin trading, magnifying both profits and losses. Such trades were not only popular with traders but padded the bottom lines of OKX and other exchanges, which charged fees on leveraged trades while waiving fees on other transactions.

OKX, HTX and other exchanges awarded users points based on their trading volumes. The more a trader bought and sold, the more the exchange allowed him or her to increase leverage. In 2014, OKX also became one of the first major exchanges to introduce a Bitcoin futures trading platform, allowing users to make leveraged bets on the future of the token’s price movements.

“The fintech space in China was a complete Wild West … There was very little regulatory oversight and a huge boom in adoption, in large part because there was both a love of speculation and a limited set of outlets in the domestic market for speculation,” says Martin Chorzempa, a senior fellow at the Peterson Institute for International Economics in Washington. “That led the user base to grow huge.”

As the exchanges grew, Chinese regulators began to worry about excessive speculation, and critics argued that margin trading amplified market swings and worsened crashes. OKX and its peers pushed back, arguing that the risks were exaggerated and more sophisticated financial products were necessary for the industry to mature.

After doing nothing for years, Chinese authorities moved decisively in January 2017, launching their first sweeping crackdown on crypto. Regulators inspected and raided major exchanges including OKX, HTX and Binance. Soon after, the platforms shut down their margin-trading businesses in China. The People’s Bank of China said margin trading had violated regulations by “causing abnormal market volatility.”

The Chinese government’s decision that September to ban initial coin offerings – a popular fundraising tool for launching new tokens – proved the final straw for the country’s top crypto players. Major platforms, including OKX, shut down their mainland operations and relocated to alternative hubs such as Hong Kong and Singapore.

China’s main concern at the time was capital flight, says Emily Jin, a senior associate with the China Practice at The Asia Group. Officials wanted to ensure that cryptocurrencies could not be used to funnel money abroad.

Xi Jinping was also emphasizing the need for finance to serve the real economy, while state-run media warned that margin trading and speculative activity in crypto markets risked social instability.

“It was obvious people were using crypto as a speculative asset, almost like gambling,” says Jin.

OKX, Binance and HTX had tried to expand internationally for years, then the Chinese crackdown made doing so necessary. They set up shop in friendlier jurisdictions including Singapore and Dubai. They also discovered a new leverage tool to attract investors: a derivative trading product called a “perp”.

IN PERPETUUM

The ‘perp’ contract, also known as perpetual swaps or perpetual futures, was invented by Arthur Hayes, an American entrepreneur.

Hayes was an equities trader at Citi Bank’s Hong Kong office. Laid off in 2014, he had time to explore crypto. Hayes noticed an arbitrage opportunity in buying crypto in Hong Kong and re-selling it in renminbi in China, where prices were higher.

Hayes wanted to use sophisticated financial derivatives for crypto but was unsatisfied with tools from ICBIT, a Russia-based exchange that pioneered Bitcoin derivatives in 2011. He aimed to develop his own crypto derivative tools. But by the time he founded a new platform, BitMEX, in 2014, OKX and HTX were dominating the derivatives market. In a blog post, Hayes said that in 2016 the Chinese exchanges controlled 95 percent of all futures and margin trades.

Hayes and BitMEX did not respond to The Wire China’s request for comment.

Hayes could not match OKX and HTX’s liquidity. His Chinese competitors had established markets with thousands of active derivative traders. But he believed he could beat them on simplicity, and by doing so extend the market for crypto derivative products beyond professional traders.

The result was the perp. A perp is essentially a futures contract without an expiration date, a concept originally proposed in 1992 by Nobel Prize winning economist Robert Shiller. In traditional futures, positions are settled at a fixed point in time.

Perps never expire. Instead of settling on a fixed date, they require regular payments, typically every eight hours, in which traders on one side of the market pay those on the other. These payments are designed to keep the contract’s price closely tied to the spot price of the underlying asset.

When BitMEX unveiled perps, it offered traders leverage of up to 100 times their initial investment.

Hayes has credited Chinese exchanges, including OKX and HTX, with pioneering risk-management tools such as socialized losses, which re-direct the profits of winning traders to cover liquidation losses, and auto-deleverage systems, which automatically close a trader’s winning positions to cover other trades that are below water. Such tools were designed to prevent exchanges from collapsing during extreme market volatility.

Chinese platforms that had recently moved offshore, insulating them from Beijing’s restrictions on leverage, embraced perps. OKX rolled out its own perpetual contracts in 2018, accompanied by a warning to users: “We would like to remind our users that due to [perps’ high leverage], implementing risk control strategies are equally crucial in trading,” said Lennix Lai, then OKX’s financial market director.

The warnings did little to dampen investor enthusiasm for borrowing, and perps quickly became central to the growth strategy of companies including OKX, HTX and Binance.

“BitMEX pioneered perpetual futures, but they were aggressively scaled by Binance and OKX,” says Butterfill. “It fits with the aggressive trading mentality of Chinese [investors]. They had very simple platforms that made complex derivatives quite accessible to retail users.”

Because they were so popular, perps became a key area of competition among exchanges. Platforms raced to attract users by adding more and more tokens that traders could make leveraged bets on.

“Exchanges like Binance and OKX started listing tokens at a very rapid pace because people just wanted access to these futures products and to trade them as fast as possible,” says Fraussen.

Monthly trading volumes in perpetual futures have surged from about $35 billion in 2018 to $6.4 trillion by 2025. A crypto market boom fueled by the rise of Bitcoin exchange-traded funds (ETFs), and President Trump’s 2024 election victory, has been accompanied by a rush into derivatives.

Perpetual futures now account for roughly 68 percent of all crypto trading, according to Kaiko, with originally Chinese platforms dominating activity. Nearly three-quarters of all Bitcoin perps are traded on OKX, Binance and ByBit, which was founded in Shanghai in 2018 before relocating to Singapore.

“The product became leverage,” says Aryan Sheikhalian, head of research at venture capital firm CMT Digital. “It was about how much leverage a particular platform could offer, because they are catering to the speculative user base.”

“WHAT’S UNDERLYING THESE CRYPTO BETS? NOTHING.”

Crypto backers and skeptics largely agree that the October 10 crash was driven by a buildup of leverage across crypto markets. What they disagree about is the nature of that leverage — a divide that largely comes down to confidence in the underlying assets.

Critics warn that increasingly leveraged crypto markets, built on assets they argue have little or no intrinsic value, could pose broader risks to the global financial system.

“At least with subprime mortgages you had houses. But what’s underlying these crypto bets? Nothing,” says Wilmarth.

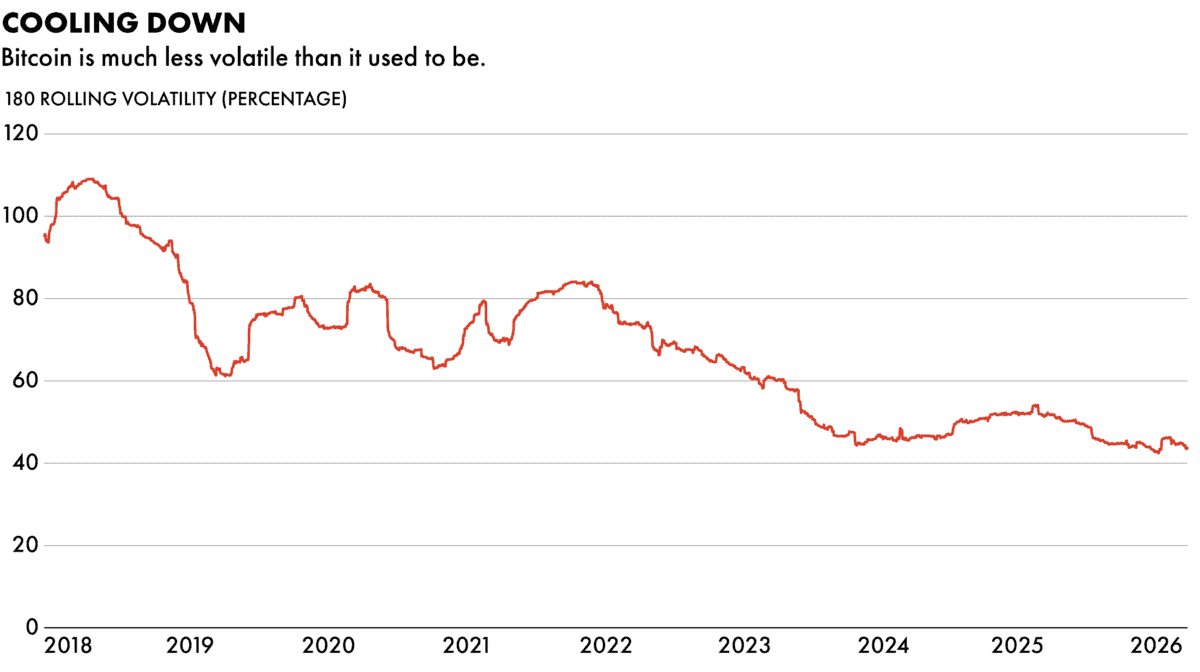

Supporters believe that the risk is overstated, arguing that Bitcoin is “digital gold” whose value will rise as more investors flock to it. In their view, growing leverage reflects a maturing market that increasingly resembles traditional equities, and they point to data showing that Bitcoin’s volatility has declined even as leverage has increased.

“I understand the panic around these markets being leveraged,” says Laurens Fraussen, a crypto market analyst at Kaiko. “But crypto tokens [have attracted trillions in investment], so even if derivatives markets are leveraged, a lot of the price moves will still come from real demand.”

President Joe Biden’s administration was wary of these products. Exchanges like OKX and Binance could not offer their services in the U.S.

In 2023, the Commodities Futures Trading Commission charged Binance with operating an illegal derivatives exchange in the U.S. It alleged that Americans conducted trillions of dollars of transactions on the platform, and that Binance advised customers on how to use VPNs to evade its own restrictions. That November, Binance pled guilty to those and other charges brought by the Department of Justice as part of a $4 billion settlement that included four months of jail time for Zhao.

In February 2025, OKX reached a $504 million settlement with the U.S. government after the CFTC alleged it had operated an illegal crypto exchange and processed over $1 trillion worth of transactions from Americans from 2018 to 2024.

But that was then. Binance and OKX — as well as Hayes and BitMEX — now enjoy the good graces of the crypto-friendly Trump administration. In March 2025 Hayes and two other co-founders of BitMEX, who had previously pled guilty to operating an illegal derivatives platform in the U.S., were pardoned by Trump. OKX received a license to legally operate a U.S. exchange last April, and President Trump granted Zhao a full pardon in October, though he later distanced himself from the decision. “I don’t know who he is,” Trump said on CBS’s 60 Minutes. “I heard it was a Biden witch hunt.”

In March the Intercontinental Exchange, the parent company of the New York Stock Exchange, announced a new strategic relationship and investment in OKX that values the company at $25 billion.

The softening regulatory stance towards crypto comes as the U.S., after years of allowing the industry to operate in a regulatory grey area, prepares to issue clearer parameters for it. Since passing the GENIUS Act governing stablecoins last year, Congress has been working on legislation that includes more all-encompassing regulations for the crypto industry.

But drafts of the new legislation mostly cover the spot market for crypto assets, rather than derivatives, and regulatory responsibilities for the SEC and CFTC.

Some observers, including Reniers at Duke’s Financial Economics Center, say the legislation does not sufficiently address the risks exposed by October’s crypto flash crash — or those inherent in highly leveraged markets generally.

“The October meltdown should have been viewed as an opportunity for policymakers in D.C. to hit pause on the market structure talks,” he said. “It’s important to understand what happened so you can try to prevent it from happening again.”

One sticking point in early drafts of the bill, which has drawn concerns from unlikely bedfellows Wall Street executives and Senator Elizabeth Warren alike, is a so-called ‘defi carveout.’ Defi, short for decentralized finance, refers to crypto trading and borrowing services that run through blockchain-based software and user networks rather than a traditional financial firm.

Unlike centralized exchanges, de-centralized exchanges, such as Binance-backed Aster, do not have a single company acting as a middleman for customer trades. Critics say that even if centralized exchanges were regulated, carving out defi platforms could give the crypto industry a way to sidestep tougher S.E.C. securities rules. Defi exchanges often offer higher leverage than centralized exchanges, and traders appear to be turning to them as they struggle to squeeze out profits on more regulated U.S. derivatives platforms such as the Chicago Mercantile Exchange, the world’s leading marketplace for derivatives.

Crypto traders are also expanding beyond crypto tokens into real-world assets, like company stocks and bonds. As part of its deal with the Intercontinental Exchange, OKX announced that it will partner with the NYSE to create tokenized equity markets tokens that track the price of equities. Indeed, crypto exchanges including Kraken and ByBit have already done so. Binance, which abandoned tokenized stock trading in 2021 amid regulatory scrutiny, recently began offering leveraged perpetual contracts tied to traditional assets including gold, oil and some stocks such as Tesla.

A Binance spokesperson told The Wire China that the company’s new ‘TradFi perps’ have already captured significant market share of global trading in assets such as gold. The product has been approved by regulators in Abu Dhabi, but it is not available in the U.S.

“The rapid and positive reception to TradFi perps … underscores perpetuals as the preferred tool for an always-on market for hedging and discovery,” a Binance spokesperson told The Wire China. Binance added that it informs users of the risks of leveraged trading and “continually monitors and adjusts the available leverage for risk control and user protection.”

Still, this is a prospect that alarms some crypto industry experts.

“It could be an existential risk to traditional markets,” says Carol Alexander, a finance professor at the University of Sussex. Even though traders may not own equities in the same way as traditional shareholders, Alexander says tokenized trading could still spill over into the supply and demand of the underlying assets. “You don’t want crypto exchanges getting their hands on Berkshire Hathaway’s stock and making it hugely volatile. As soon as it’s [available to professional traders] on a platform like Binance … it’s much, much more exciting than [just trading] Bitcoin all the time.”

More broadly, the concern is that leverage has become central to crypto just as the industry is increasingly woven into the global financial system.

“As crypto integrates into the broader financial system, the risk of a systemic crash increases,” says Hilary Allen, a law professor at American University. “The stakes are high for everyone.”

Grady McGregor is a freelance writer for The Wire China based in Washington, D.C. He was previously a staff writer at Fortune Magazine in Hong Kong, writing features on business, tech, and all things related to China. Before that, he had stints as a journalist and editor in Jordan, Lebanon, and North Dakota. @GradyMcGregor