On October 1, the opening morning of TOKEN 2049 at Singapore’s Marina Bay Sands resort complex, thousands of attendees filled the convention halls, trading rumors about which member of Donald Trump’s family might show up. Would it be Eric? Or Don Jr.? Or both?

When it came time for a panel on the Trump family’s World Liberty Financial crypto project that afternoon, the hall was buzzing.

Crypto was hotter than ever and the industry had, in very large part, Trump’s return to the White House to thank for it.

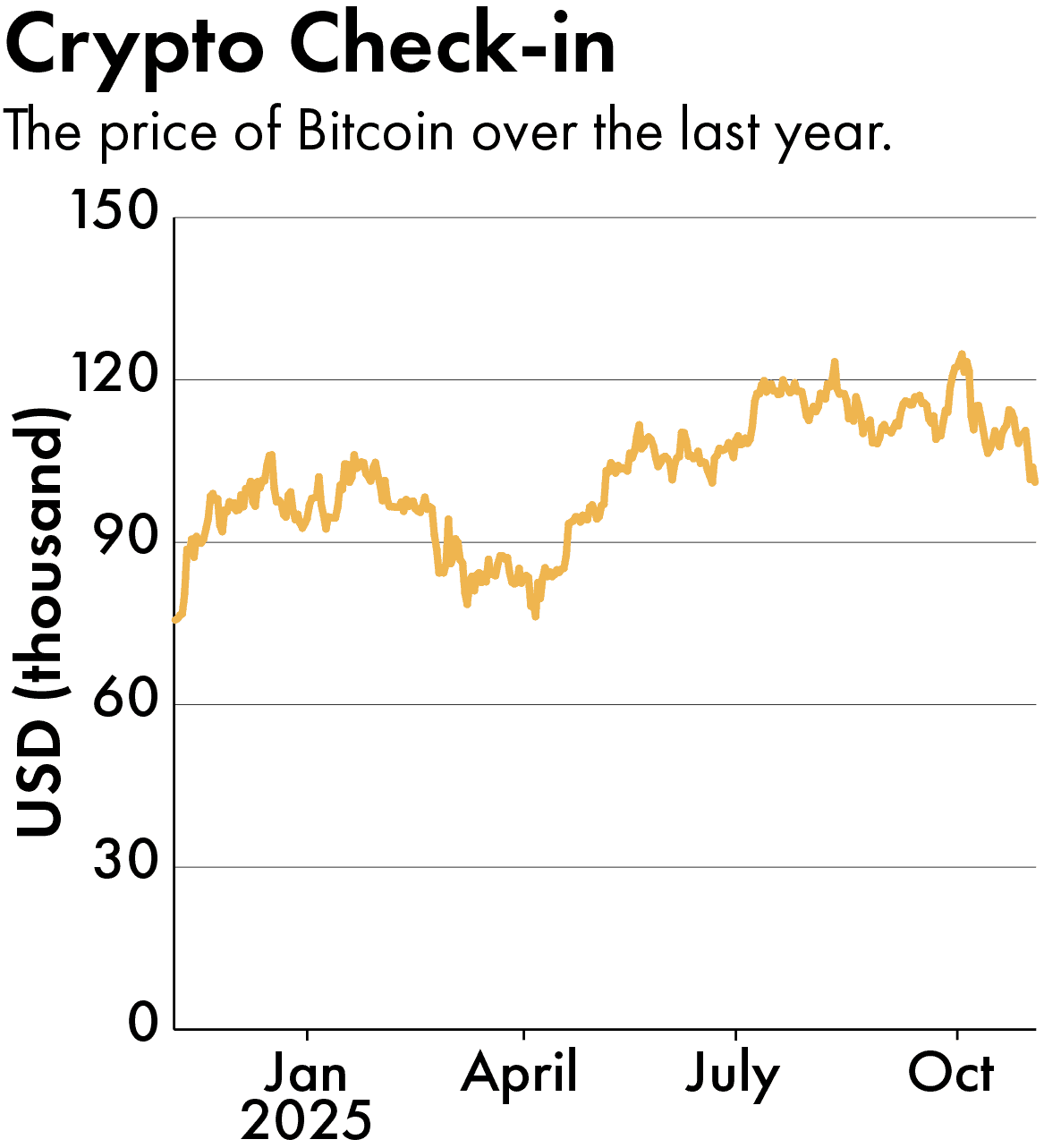

Bitcoin hit a record high of $126,270 during the week of the conference, a reflection of how the industry and its markets have rallied around Trump’s more crypto-friendly administration after years of grumbling over Biden-era regulation.

It was a fitting moment for the Trump family to take a victory lap — and to do so in China’s backyard no less. The Chinese Communist Party has long been wary of financial risk in all its forms, and crypto currencies in particular. The industry has been propelled forward by pioneering Chinese entrepreneurs who, not welcome back home or in Biden’s America, took refuge in places such as Singapore and Dubai.

A promotional video highlighting Donald Trump Jr. speaking during a panel session at TOKEN 2049, Singapore, October 1, 2025. Credit: TOKEN 2049

In the end it was Donald Trump Jr. — not Eric — who appeared in Singapore. He walked out beside Zach Witkoff, World Liberty’s co-founder. As they did so, hundreds of cheering fans rushed toward the stage with their phones held high. An Asia-based World Liberty Financial fan club unfurled banners bearing the company’s logo.

Trump Jr. and Witkoff, the son of President Trump’s special Middle East envoy Steve Witkoff, reveled in the reception. On Inauguration Day the Trump family had launched a meme coin that even enthusiasts for an industry built on hype and speculation viewed as at best a cash grab. Less than a year later, they were being feted.

“We truly believe this is the future of finance,” said Trump Jr. “These crypto guys understood that we were going to bat for the community, and they went to bat for us because of it. It’s a great symbiotic relationship.”

“They all sat up here and they called us a joke, they called us a meme coin, they said we would never amount to anything,” Witkoff said, pausing as cheers swelled. “How are we doing now, folks?”

Trump Jr. outlined his vision of a future in which stablecoins — and his family’s token in particular — would sit at the center of the global financial system. And wittingly or not, he had a message for China:

“Stablecoins are going to be the thing that backfills all of these countries that used to buy U.S. Treasuries,” he said. “We’re going to do that. That’s going to create and maintain the dollar hegemony that’s allowed Americans to lead, that’s allowed us to have the power over the world that has kept so many places safe, sound, and strong.”

Not too long ago Trump Jr.’s vision of using stablecoins, including his own USD1 coin, to preserve America’s financial dominance would have sounded far-fetched. But just under a year into his father’s second term, it’s a vision the crypto world has been forced to take seriously. And it’s one that has begun to draw the attention of the power with the most to lose if he is right: China.

At the conference, the bull market euphoria was on full display. Some 25,000 attendees filled up five floors of the convention center with booths featuring pickleball courts, zip lines and climbing walls. In buffet lines, attendees swapped stories about the dozens of side parties – some hosted on yachts – and which crypto companies had rented out Zouk or MARQUEE, Singapore’s premier nightclubs.

One attendee’s take on it summed up the vibe: “Everyone is extremely liquid right now,” he told The Wire China.

ONE COUNTRY MISSING

Walking through the 500-plus booths of Asia’s largest crypto conference, China was notable only in its absence — few, if any, exhibitors were targeting the world’s second largest economy.

In the early 2010s, Chinese entrepreneurs and traders were among the first to embrace cryptocurrencies. By the middle of the decade, more than half of all Bitcoin trades were conducted in yuan, and Chinese miners were producing as much as three-quarters of the world’s new Bitcoins.

China saw [crypto] as a threat to the financial sovereignty of the yuan. [Loosened capital controls] was a threat to China’s financial order, and that’s the most important financial goal of the Chinese government.

Alex He, a senior fellow at the Centre for International Governance Innovation

A series of crackdowns — beginning with restrictions on domestic trading platforms in 2017 and followed by a sweeping ban on trading, mining and other crypto activities in 2019 — has forced nearly all crypto activity in China to shut down or move offshore.

By contrast President Trump’s embrace of, and outsized influence over, the industry could not be more stark.

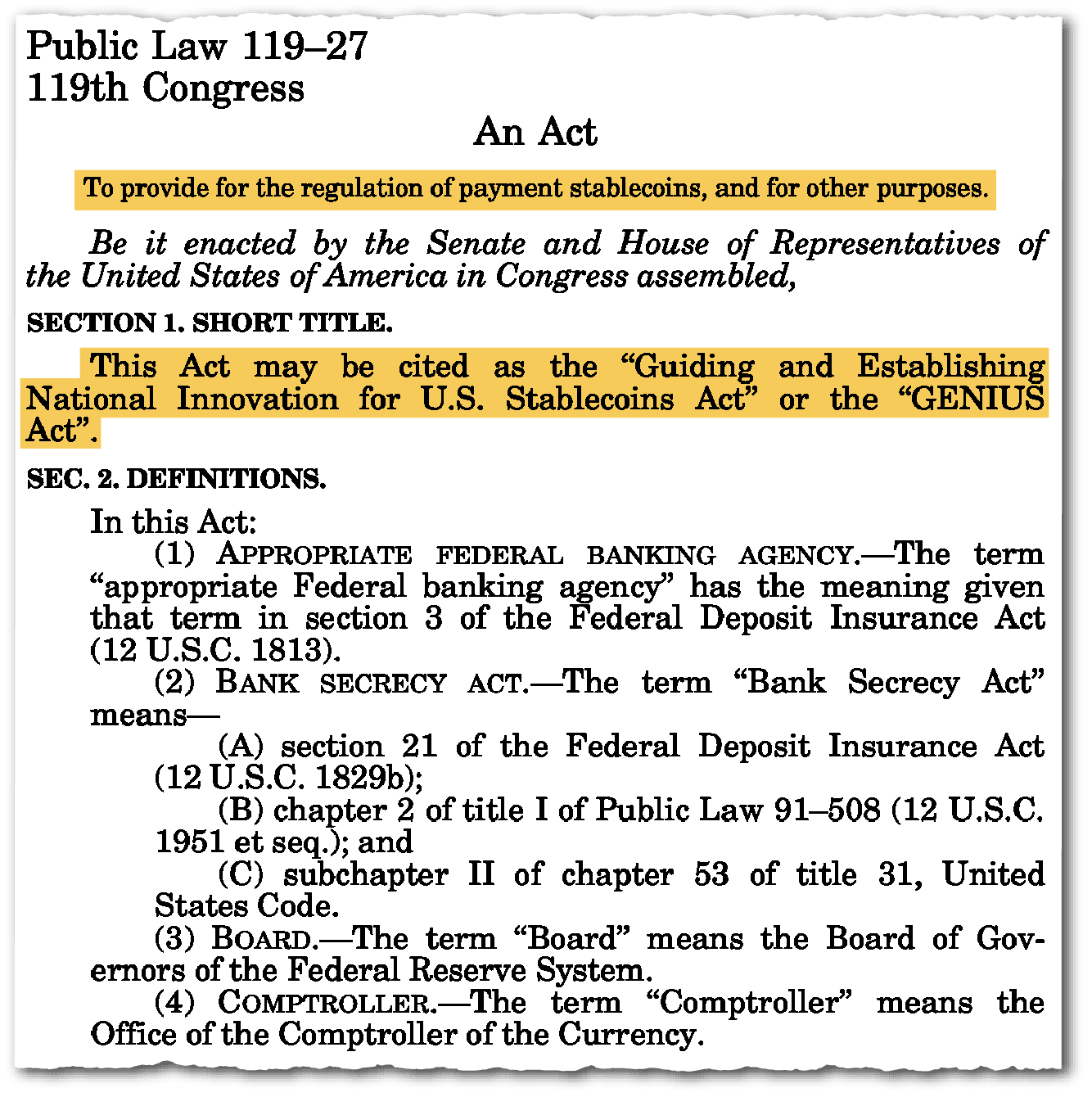

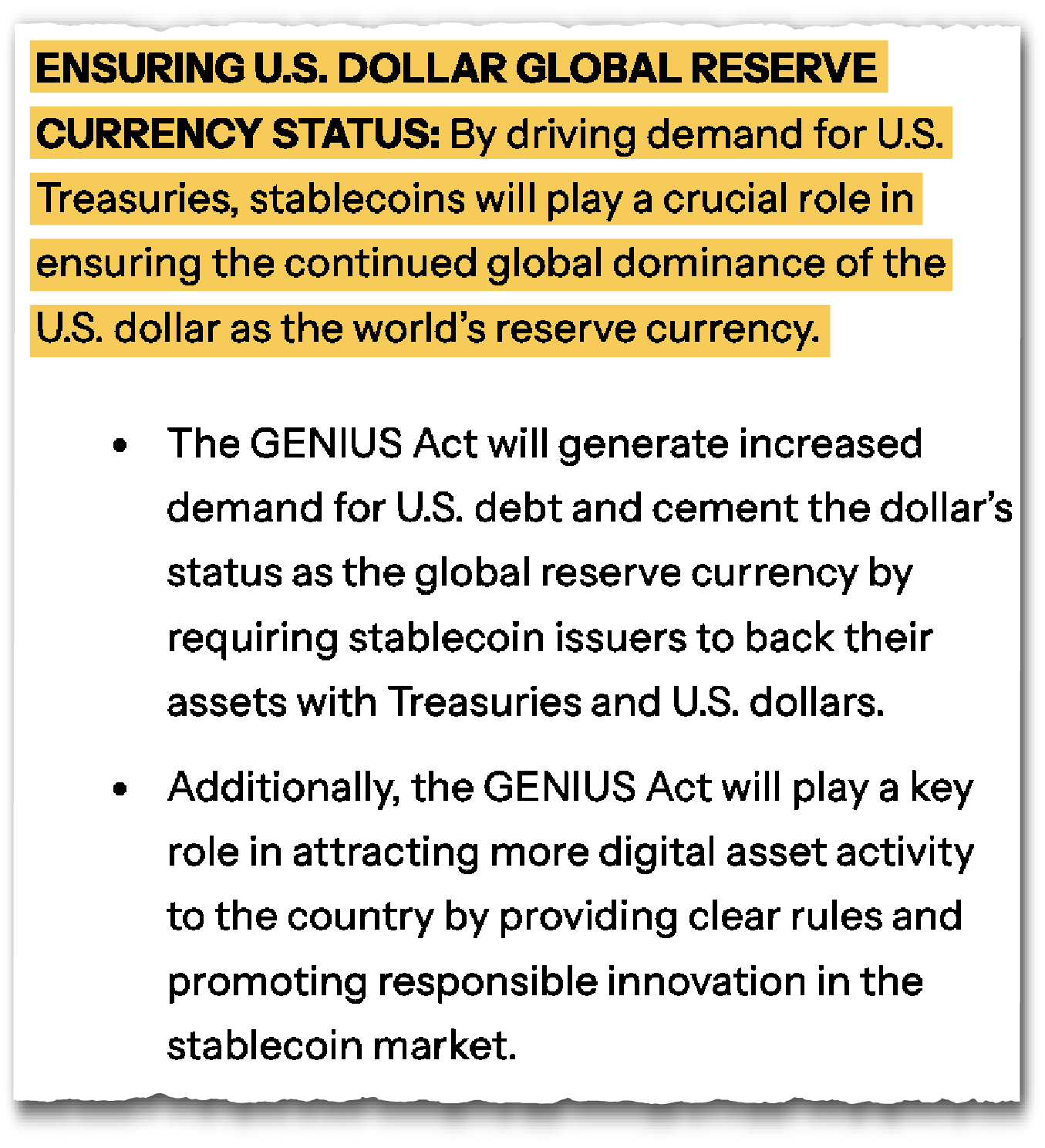

In July, the U.S. government passed the GENIUS Act — Trump’s signature piece of crypto legislation that sets up a regulatory framework for stablecoins — creating an explosion of interest for the digital tokens tied to real-world currencies. “The GENIUS Act… is setting the standard for the whole world,” said Charles Cascarilla, chief executive of the crypto platform PAXOS. “It’s the golden age for stablecoins.”

Trump Jr. and Witkoff were there to promote World Liberty Financial’s USD1 stablecoin. After launching in March, the USD1 token quickly became one of the world’s largest crypto tokens with a nearly $3 billion market cap. The company claims its dollar-backed digital currency allows users to settle cross-border payments faster than traditional banks, and will allow customers to do things like invest in Trump real estate projects.

Critics including Senator Elizabeth Warren of Massachusetts have said that the USD1 coin opens up “staggering” conflicts of interest. The New York Times reported earlier this year on links between a $2 billion investment the U.A.E. made using USD1 and the Trump administration’s decision to allow the U.A.E. to purchase some of Nvidia’s most advanced chips.

There were plenty of reminders at TOKEN2049 of the industry’s earlier ties to China, including the star treatment given to Justin Sun, the China-born crypto entrepreneur.

Trump Jr. and Witkoff delivered their sales pitch on the “OKX Main Stage,” named after the large crypto exchange that was one of the event’s title sponsors. OKX, now among the world’s largest crypto exchanges, was founded in Beijing by Chinese entrepreneur Star Xu. Then known as OKEx, the company decamped to Malta in 2018 after China’s crackdown on cryptocurrencies.

KuCoin, another exchange founded in China and now headquartered in the Seychelles, had professional golfer and global brand ambassador Adam Scott on hand — promoting the company while helping attendees perfect their swings on a golf simulator.

Other exchanges with Chinese roots that have since moved offshore — including Huobi, MEXC, BingX and Bitget — were also prominent at the conference.

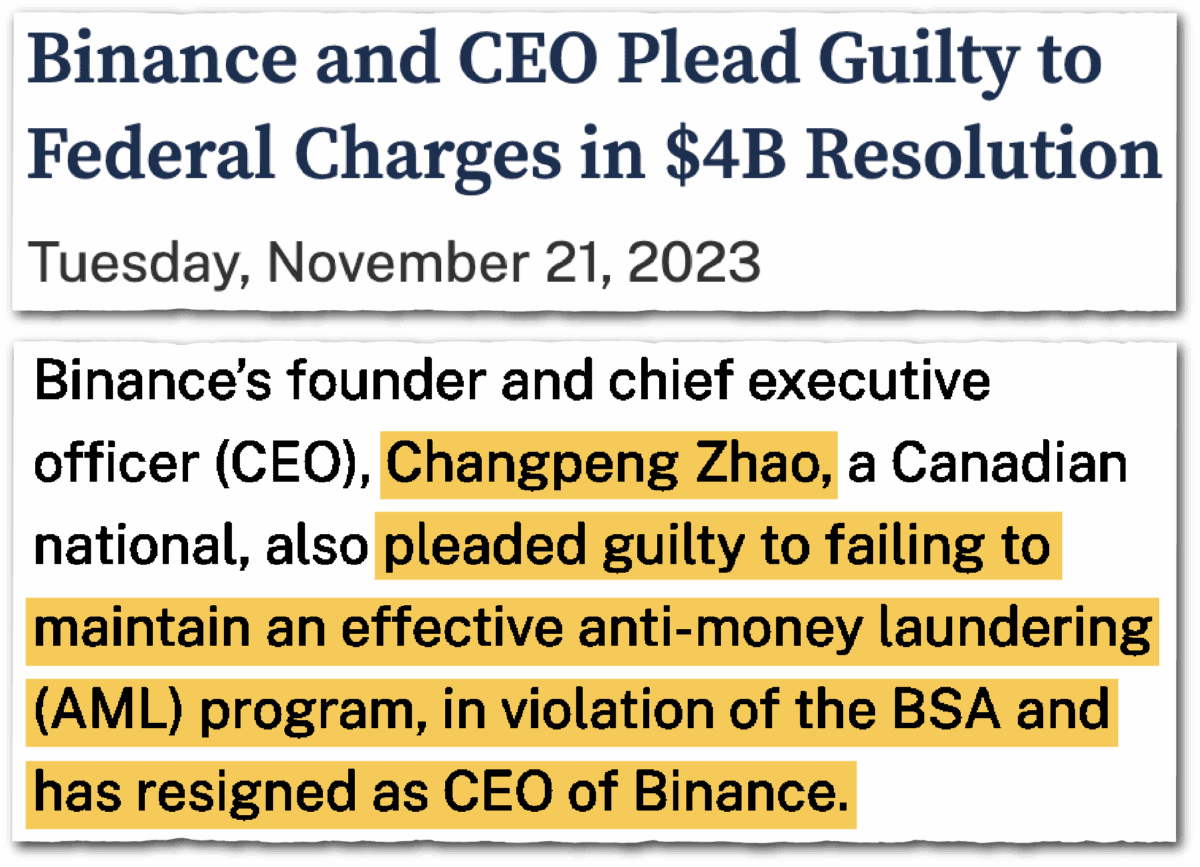

Binance, the world’s largest crypto exchange, founded in China by Changpeng Zhao, kept a relatively low profile at the conference. Weeks after the conference, President Trump pardoned Zhao, who had previously pled guilty to violating U.S. money-laundering laws.

“I have no idea who he is,” President Trump told CBS News on November 2. “I was told that he was a victim, just like I was and just like many other people, of a vicious, horrible group of people in the Biden administration.”

The Chinese government, however, is unlikely to regret the flight overseas of exchanges promoting speculative crypto trading and the channels they provided for money to flow out of China.

“China saw [crypto] as a threat to the financial sovereignty of the yuan,” said Alex He, a senior fellow at the Centre for International Governance Innovation. “[Loosened capital controls] was a threat to China’s financial order, and that’s the most important financial goal of the Chinese government.”

THE eCNY

In lieu of fostering the development of private-market crypto exchanges, the Chinese government has instead pursued blockchain technological development via an avenue it can control: the eCNY.

The eCNY, or digital yuan, is China’s version of a Central Bank Digital Currency (CBDC), a digital form of cash issued and backed by the People’s Bank of China. Unlike other crypto currencies, the e-CNY is fully controlled and regulated by the Chinese government, allowing it to track transactions in real time.

The Chinese government has been rolling out the e-CNY across the country since 2019, but uptake among the Chinese public has been slow. That’s because Alipay and WeChat Pay still dominate the digital payments market in China, offering more convenience and greater integration into the lives of Chinese consumers. Even as domestic adoption has lagged, China is still pushing the e-CNY for cross-border use, recently launching a Shanghai hub to promote its role in settling international transactions.

But after the U.S. passed the GENIUS Act in June, prominent voices within China’s government began to sound the alarm about the need for China to create its own yuan-backed stablecoins.

In July, Wang Yongli, formerly a senior executive at Bank of China, said the U.S. legislation and rapid development of dollar-backed stablecoins offered a “profound warning” to China. In his article, he argued stablecoins could eventually “supplant oil in strategic significance,” and echoed Trump Jr.’s proclamation that dollar-backed stablecoins would “reinforce the global dominance of the U.S. dollar.”

…if China does in fact cede ground to the U.S. in stablecoins, will it matter — or could it prove to be a case of never interrupting your enemy when he is making a mistake?

The Securities Times, part of the People’s Daily group, also argued that China would need to develop yuan-denominated stablecoins “sooner or later.”

Legislation that went into effect in August in Hong Kong seemed to indicate that China planned to use the semi-autonomous region as an experimental testing ground for its own stablecoin ambitions. Chinese tech giants like Alibaba’s Ant Group and JD.com eagerly jumped into the market, while also lobbying Beijing to allow them to use yuan-denominated stablecoins to settle foreign transactions.

Dr. Monique Taylor, a lecturer in World Politics in the Faculty of Social Sciences at the University of Helsinki, said a dual-pronged approach using both the e-CNY and stablecoins made sense for China.

“The e-CNY fulfils the central bank’s main objectives of modernising the payments system, strengthening oversight of transactions, and ensuring that digital forms of money remain under state supervision,” Dr. Taylor told The Wire China.

However, yuan-backed stablecoins offered a more practical solution for cross-border trade settlements and would also enhance the yuan’s global reach, she added. “The e-CNY cannot fully replicate the market functionality of stablecoins, particularly in areas driven by private innovation and decentralised infrastructure.”

In mid-October, Beijing appeared to have a change of heart. Chinese regulators put Hong Kong’s stablecoin experiment on hold, according to the Financial Times and the South China Morning Post.

In a speech on October 27, Pan Gongsheng, China’s central bank governor, appeared to justify a pause without confirming it explicitly.

“Stablecoins currently fail to effectively meet basic requirements for customer identification and anti-money laundering, exacerbate loopholes in global financial regulation, such as money laundering, illegal cross-border fund transfers, and terrorist financing,” Pan said.

MISSED OPPORTUNITY OR DISASTER WAITING TO HAPPEN?

Chinese firms in Singapore were nonetheless eager to demonstrate that they still have a major role to play in the industry.

Conflux, which participated in an Alibaba-hosted panel, recently launched the first-ever yuan-backed stablecoin in Kazakhstan. Another company, EBANX, told The Wire China that yuan-backed stablecoins could make digital payments more efficient for Chinese businesses and their overseas partners.

“While China builds an alternative to dollar-centric [payment systems], EBANX can offer Chinese merchants access to Latin American, African, and Southeast Asian markets,” Eduardo de Abreu, VP of Product at EBANX, said.

But without Beijing’s support, such projects are likely to remain small and peripheral, effectively letting the U.S. dominate the global stablecoin market.

“At the end of the day, the only stablecoin that really matters is the USD-based stablecoin,” Retno Widuri, head of crypto and global fintech at Unlimit, said.

But if China does in fact cede ground to the U.S. in stablecoins, will it matter — or could it prove to be a case of never interrupting your enemy when he is making a mistake?

[The sector] has an awful lot of proving to do before it develops any sort of significant momentum. The extent to which stablecoins really gain traction in the global economy depends a lot upon whether they move beyond just being the cash leg of a crypto trade into real world payments and transactions.

Ed Butchart, a private investor and former chief investment officer of Kepler Partners

To many crypto true-believers at TOKEN, the dangers of China being left behind in stablecoins were clear. To them, the increasing interest from major banks and tech firms in stablecoins signals that the institutional adoption of stablecoins is only a matter of time. And once stablecoins are more routinely used to settle foreign payments, they add, there will be increased demand for the Treasuries backing those stablecoins.

“I think stablecoins are going to replace FIAT currencies, fully,” Benjamin Grolimund, a senior executive at crypto firm Flipster, said on the sidelines of the conference. “That means that central banks down the line, and also private companies, are all going to issue digital tokens that are backed by the central bank.”

But a stablecoin-led future for global finance is far from certain. Beyond critiques about facilitating money-laundering and evading capital controls, skeptics argue that there is no guarantee that, as Trump Jr., U.S. Treasury Secretary Scott Bessent and others claim, that increasing the use of dollar stablecoins will automatically boost the dollar’s status as the global reserve currency.

“[The sector] has an awful lot of proving to do before it develops any sort of significant momentum,” said Ed Butchart, a private investor and former chief investment officer of Kepler Partners, a boutique asset management firm based in the UK. “The extent to which stablecoins really gain traction in the global economy depends a lot upon whether they move beyond just being the cash leg of a crypto trade into real world payments and transactions.”

DON’T DO AS JACK DID

On TOKEN’s final afternoon, hundreds of tired attendees packed into one of TOKEN’s main halls for the event’s final draw: a roast of Tron founder Justin Sun by T.J. Miller, the comedian and star of the Silicon Valley television show.

Sun, a Chinese national, is brash, attention-seeking and fond of challenging authority — precisely the kind of figure the Chinese Communist Party tends not to appreciate.

Sun launched a crypto project in China the day before the government’s 2017 crackdown; then he fled the country. Today, he runs a platform that the United Nations has described as a preferred channel for money laundering in Asia. (In response Tron said it does not “exercise direct control” over who uses its technology.) He also recently invested more than $90 million into Trump family crypto ventures. Soon after, the Securities and Exchange Commission paused its fraud investigation into him.

Wearing a black T-shirt emblazoned with his company’s Tron logo, Sun sat awkwardly in a large white chair at center stage as Miller teased him about spending $4.5 million for a dinner with Warren Buffett and $28 million for a seat on a space flight from Blue Origin, the company founded by Jeff Bezos.

At the end of the roast, Miller turned his attention to one power Sun hasn’t managed to cozy up to: the Chinese government.

“Justin, your protege Jack Ma taught you the secret to securing one’s wealth. Don’t criticize the Chinese government,” Miller said.

The joke drew some laughs, but it also underscored the divide between Sun’s generation of Chinese crypto entrepreneurs — who have flourished abroad — and the government back home that remains deeply wary of the industry they helped create.

The chaotic and freewheeling world of crypto and China’s strict financial order may never happily co-exist. But with the prospect of dollar stablecoins upending the global financial system, will Beijing need to engage more with the crypto world to compete in stablecoins? Can it really afford to keep the industry at arm’s length?

“I see the passion and craziness in people in cryptocurrency circles. They want to reshape the modern financial system,” says He at CIGI.

Those goals are completely at odds with a ruling party in China that prioritizes stability at all costs, He explained. “China views this as ‘[crypto] wants to overthrow our system — not a chance.’ They will be very, very cautious and conservative in stablecoins … But they also really worry about being left behind.”

Grady McGregor is a freelance writer for The Wire China based in Washington, D.C. He was previously a staff writer at Fortune Magazine in Hong Kong, writing features on business, tech, and all things related to China. Before that, he had stints as a journalist and editor in Jordan, Lebanon, and North Dakota. @GradyMcGregor