Meg Rithmire is the F. Warren MacFarlan associate professor of business administration at Harvard Business School. Her research focuses on China’s political economy, including real estate, outbound investment, and government discipline of business and entrepreneurs. She earned a B.A. from Emory University and an M.A. and Ph.D. from Harvard. Rithmire is the author of Land Bargains and Chinese Capitalism (2015), and a forthcoming book titled Precarious Ties: Business and the State in Authoritarian Asia, which compares state-business relations in China, Malaysia, and Indonesia. What follows is a lightly edited Q&A.

Illustration by Kate Copeland

Q: Let’s start with the real estate sector. Can you give an overview of what you have seen happen in the market in China over the past year or so?

A: Everyone has been asking, especially this time last fall: Is the real estate bubble about to burst? I was answering the same question in 2012, in 2011, and 2010. The current question has been: Is it finally about to pop? And then people have asked two analogy questions: is this China’s Lehman moment? Or, Is this the ‘Baburu’ moment? — referring to the Japanese property bubble [in the 1980s] that led to the so-called lost decades. The answer is that it’s really neither.

The reason is because the Chinese Communist Party (CCP) has more resources at its disposal to control supply and demand of major parts of the Chinese economy than were available to the American government or the Japanese government. That’s both the cause and the solution to the real estate problem, and also the cause of kicking the real estate problem down the road. When people see things like overcapacity in housing in China, they tend to think there’s no way that demand can be sustained for this level of housing and soon enough, the prices will plummet, and there will be a crisis.

Instead, what we’re seeing in China is a wrenching devaluation of prices in the real estate sector without an acute crisis. We’re also seeing a refusal to allow real estate companies to really go bankrupt in China, either local ones, or national ones. Instead, we’re seeing a use of what I call the state’s coercive apparatus. It’s a typical playbook in China — instead of letting a firm exit the market through bankruptcy, because it has had bad practices – they arrest the founders of the company and then slowly unwind its assets in a way that essentially nationalizes or takes the burden of a debt crisis onto the state. The CCP is, of course, unwilling to let prices unwind very quickly, because that will be a social stability problem; it will be a problem for the many Chinese households that have invested in housing, as well as local economies. If you look at recent data, prices are coming down a little bit in Shanghai, and they’re coming down a lot in other places. There’s still this unevenness to how painful it would be for there to be a rapid unwinding of prices.

What the state controls in China is different from other places. They control the supply and demand for land. They have an aggregate control over state owned land in China, and then distribute that through hierarchies. Every province gets so much land to develop each year and then negotiates with the provincial municipalities to figure out how much land they get to develop. The central state has the ability to increase or decrease that supply to adjust prices and to do it in a local context. The other tool that they have control over is demand, through the amount of people in any given city. Loosening Hukou [household registration] regulations in some places versus others is a tool that they can use to generate demand. We have to remember that China’s still under-urbanized for its level of industrialization. There is still under employed labor in the Chinese countryside. And so that’s a source of demand for housing supply that’s been there.

The other thing they have control over is the cost of capital through the banking system, which economists would describe as financial repression. You have a very high savings rate in China and it’s essentially captive as households cannot easily invest overseas, because there are capital controls. Also equity markets tend to be underdeveloped in China, and when they do develop a little bit, it becomes quite bubbly. So people tend to channel their savings into housing. For that reason, it’s a really delicate thing, because we’re not just talking about the prices of people’s homes, but how well off average families feel, because they’ve invested their savings for the next generation.

So what would it take to get to a place where there’s not someone asking me every 10 years about a housing crisis and a real estate bubble? It would be a lot easier for economic policy makers if they let prices unwind, according to a market logic, but that would have consequences for social stability, and, frankly, consequences for the solvency of local governments who depend on rising land prices to service their own debt obligations, which are very much based on land as collateral.

What would it take to change that? It seems pretty obvious from an economic standpoint, which is that fiscal reforms [are needed] that give local governments sources of revenue that are not tied to land sales. That would be something like a property tax, or a tax renegotiation between the central and local governments in China. And then it might also take financial reforms that would allow households to have sources of investment that weren’t real estate. And then there would have to be some sort of social security reform as well, which would allow Chinese households to feel less anxious about the future. The structure of the population and the kind of burden of familial obligations in China makes it such that everyone wants to secure several apartments, to make sure that their children or their parents are doing okay. And they’re relying on that housing as a means of appreciating their savings, and generating security for their family, instead of being able to rely on, for example, a stable pension or old age care system from the state.

Until there’s a suite of social welfare reforms, fiscal reforms, and financial reforms that remove all the incentives to push all of these private savings into housing, and push a bunch of public investment activity — whether it’s debt financed or otherwise — into developing more and more real estate, and more and more housing, we’ll see this same bubble pop up.

What are the specific barriers to enacting those policy reforms?

There are a lot of politics involved. Specifically, let’s take fiscal reforms. Even under Xi Jinping in the first few years, there was a desire to do something like a property tax. It was piloted in Chongqing; it was piloted in Shanghai, and you got resistance from a couple of directions. First of all, the wealthy people are the ones who own all the apartments, and they don’t particularly want to pay a lot of taxes on their property. But also, it requires knowing who owns all the apartments. And that’s pretty difficult to do, because a lot of people, particularly officials, don’t want to declare all of their assets. So you get resistance from both within the party state and from elements of society that tend to be pretty powerful and pretty vocal.

The financial part of it is also hard. Under Xi Jinping in 2014, there was a real push for capital to go into equity markets instead of into housing. You saw all these People’s Daily editorials saying the Chinese stock market can only go up, it won’t go down. It’s not a bubble, bubbles are for other places. We’ve got control over this.

To publish such editorials feels like an implicit guarantee that things will be fine: But it creates moral hazard. Investors start behaving badly, because they think basically there’s no downside risk, which leads to an asset bubble. Then the government says, it’s a market correction, prices should come down. As soon as everyone hears that, they withdraw their money from the stock market even faster. And then the government says, this is too quick of an unwinding, we won’t tolerate this, it’s too unstable. So then people say, now, my downside risk is covered once again.

So there’s this dual desire for some of the market mechanisms to work, whether in land or in financial markets, but then a refusal to tolerate the instability that’s inherent to markets working. If you want markets to determine prices, sometimes that happens in a way that’s relatively unstable or disorderly. We see it here in the United States, we see it everywhere. But it’s extra likely to happen when everyone’s incentives are to try to figure out what the government’s going to do, and to find arbitrage opportunities within that. It’s a pretty unhappy equilibrium that they have, because they have markets, but markets don’t allow firms to exit much, and they don’t really allow discipline to happen through markets.

In an ideal world, markets set prices and they facilitate firm entry and exit. They really do no such thing in China.

There’s a phrase that legal scholars use to talk about the rule of law in China: it’s rule by law. It’s the party state using law to rule the people, and not allowing law to constrain its own actions. It’s the same with the market. Instead of allowing markets to discipline actors in the financial system or discipline firms, especially state owned firms or connected firms, markets are used to discipline some people, or to uncover how people are going to behave. But it’s the state that does the disciplining, and so I call that rule by market.

You mentioned that the state uses its coercive apparatus to take down misbehaving companies. Why is that the approach and what impact does it have on the broader economy?

What it means is when you have companies like Evergrande, Tomorrow Group, Anbang, or HNA, you have entrepreneurs who behave pretty recklessly, who abuse their access to domestic political contacts to borrow a lot of money at preferential rates from Chinese banks, and then turn that money into personal wealth or misuse it and buy all kinds of things, such as soccer teams, hotels, real estate. Then you have a nationalization of those assets, and the state assumes the economic burden of unwinding it and dealing with it and arresting the founder.

What cost does it have? It means that it’s the men, women and children, the savers of China, who continue to pay for that misbehavior with their savings through the financial repression in China’s financial sector. These entrepreneurs think, worst case scenario, things could go really bad for me, and I could end up in prison. But the better case scenario is that either I’m way too big to fail — then nobody wants to put me in prison, and the state has to deal with me. Or I get away with what I can get away with. It messes up the incentives of market players. It’s really interesting if you think about what markets are supposed to do. In an ideal world, markets set prices and they facilitate firm entry and exit. They really do no such thing in China.

You recently wrote a paper about what you call ‘mafia-like business systems’ in China. The question you start out with is, why do some political and business elites regard each other as mutual threats and what does that mean for the state-business relationship? Can you answer that question?

What we see in China sometimes looks a lot like looting. Why would people found P2P platforms and then abscond with the money? Why do people found semiconductor fabs and then mortgage the equipment and disappear? Why does this seem to happen more in China than it does in the United States? You might say, well, we [in the U.S.] have rule of law, we have property rights protections and those kinds of things. But there are plenty of authoritarian regimes where you don’t have widespread fraud and you don’t have these kinds of activities. So the fundamental argument that I make is that the private sector doesn’t trust the CCP, and they haven’t ever really.

A CGTN video highlighting Pony Ma’s comments on Xi Jinping and the CCP’s committment to reform and opening up. Ma is the founder, CEO, and Chairman of Tencent.

All of our focus has been on the closeness of business ties, all of the cronies who are so close to the CCP. We have this generation of research saying now that we have a middle class, and we have entrepreneurs in China, shouldn’t they be demanding democracy? They don’t, why not? Most of the answer is, well, they’re happy enough with the CCP and they’re co-opted. I don’t dispute that. For a long time, they were happy with the CCP and it did seem like their interests were being served by the regime.

On the other hand, there is a learned distrust in China on the part of entrepreneurs. It goes back to the process of building socialism in China in the 1950s. It goes to the Cultural Revolution and what I call, over time, a pattern of accommodation and reprisal, which is the CCP first saying we need entrepreneurs, we need the private sector because we need growth or because we need stability or because we need managerial know-how; and then, once that becomes a threat to the party, or once the party gets what it wants, then it turns on those people. That’s a pattern that has come back basically since the founding of the PRC. It has to also do with the policy cycle in China, which is campaign driven. So now we’re focusing on developing equity markets, everyone should invest in equity markets; or now we’re developing semiconductors and quantum, everyone should invest in those things.

Chinese market participants are savvy, they hear those calls, they know that’s where the resources are, they know that’s where the policy protection is. So they go into those areas. But they also know that it won’t last for very long, and that there is a cycle of mobilizing resources to accomplish some goal and then recalibrating. The Belt and Road Initiative, Made in China 2025, all of these are campaigns. They’re driven by a desire to do something transformative quickly, which then generates a bunch of incentives for people to go along with it, but pursuing their own objectives. Then you find over commitment of resources, debt, all of these things; and then the state says, we have to pull the reins back on some of this. The goal, if you’re a participant, is to ride the wave as far as you can and not get caught up in the recalibration and the crackdown on the excessive mobilization activities. People are pretty savvy about figuring out how to do that.

Why did the government and business come to regard each other as enemies rather than as friends? They’ve always really regarded it as a relationship of convenience. It’s convenient for the state to have entrepreneurial resources going into a sector if it’s one it wants to develop. And it’s convenient for entrepreneurs to get state funding. But once it becomes more convenient for the state to appropriate the entrepreneur’s assets and nationalize them and control it itself, it’s going to do that. And once it becomes convenient for the entrepreneur to no longer go along with state policy and do what’s good for them, they are going to do that.

Our paper is about the rise of really huge domestic conglomerates, many of which started in real estate and had access to privatized state resources in the late 1990s and early 2000s. They end up getting really well connected, and they protect themselves by investing in relationships with all kinds of political elites. Not one faction over the other, but really investing in everybody in order to protect themselves. Then they get so entrenched, and they have such access to the state and state resources, that they start to do pretty dangerous things, like expatriating their assets, or having a lot of incriminating information on party state elites.

It’s not only that these big companies have used China’s financial system, but that they did it in partnership with political elites who also benefited a great deal.

Xiao Jianhua is a good example. The Tomorrow Group, which we talk about in the paper, had a pretty clear strategy of trying to hide its assets, abusing the stock market system to list certain vehicles and to collect a bunch of investment from public markets and then siphon it off into a private vehicle. It was also then able to borrow from the state in order to amplify its balance sheet, while its assets ended up going overseas.

A lot of what was going on with a lot of these big conglomerates looks like a big shell game. It’s politically destabilizing, as well as financially destabilizing. We saw a company like Anbang taking massive deposits from Chinese families for life insurance type products, and then turning those deposits into euro and dollar-denominated assets beyond the reach of the party state in New York or in Europe. That is financially destabilizing because the debt can cascade through Chinese society.

In 2016, Xi Jinping and others started talking about these ‘gray rhinos’, and the risk that these huge, highly indebted conglomerates could unwind really quickly, and be really financially destabilizing. It’s politically destabilizing too, because if they start revealing who helped them, and they start saying who’s invested in their companies, and who’s helped them get loans, then that can really challenge the legitimacy of the party state itself. It’s not only that these big companies have used China’s financial system, but that they did it in partnership with political elites who also benefited a great deal.

A lot of what Xi Jinping is trying to do is unwind that process in a way that’s not too rapid to be either politically or financially destabilizing. Look at someone like Xiao Jianhua, who was in state custody for four or five years before he was publicly tried and sentenced. What was he doing during that time? I don’t think he was quiet. And moreover, he left China long before they captured him and repatriated him back to Beijing. How did he know to leave? Why was he left there for so long? My view is Xi had to neutralize the people or figure out who would be felled by whatever information Xiao had to divulge before going after him. And so it’s a really delicate balance.

Can you talk about what these networks actually are, and how you went about tracking them?

We started looking into who was making overseas investments from China. The narrative for a long time was, it is state owned firms that are investing in the developing world where there are weak institutions and extractive resources. But if you actually look at it, especially after 2013, a lot of capital flows were going to the developed world, Europe and the United States. Some people were saying, ‘Oh, well, all of that is strategic asset acquisition, China buying high tech firms.’ No, in fact a lot of it was going into the leisure sectors, financial sectors, real estate, hotels, that kind of thing.

And so we started asking ourselves, who are these companies that are investing there? Now we have WireScreen, so we can do it very easily, but it used to be quite laborious. What we ended up finding is that it’s bimodal. Many Chinese companies are simple companies, they have one or two levels of ownership; others are heroically complex, they have so many levels of ownership, and then you have these founders with 800 different invested companies. Why would you find such a structure?

Then you start to look at some of the companies that I’ve named, like Anbang or Tomorrow Group. And you start to think, why would they need to have 39 financial services firms for what is essentially a high tech investment company? A lot of the structure comes about because they’re hiding their assets, and they’re doing something economists called tunneling: you have these huge pyramidal organizations which then get investment from some minority shareholders; then, essentially by stealth, you expropriate these minority shareholders by shifting assets to different parts of the group balance sheet that are beyond their reach.

And why do those structures not emerge in other parts of the world?

This is the central dilemma of what China is trying to do right now. A lot is made of how China has to advance from being an upper middle class country to a rich country, and how to do state-driven technology and innovation. That’s the obsession of a lot of people. What they’ve missed is that China’s tried to do something else too: develop a modern financial system without rule of law. It really is my view that you can’t do that.

A video from Alibaba Group documenting the company’s history from its founding in 1999 by Jack Ma and 17 other partners, to its IPO in 2014.

It’s one thing to say, how do you get economic growth without property rights and contract law? That was the question of the 80s and 90s. China has grown without any of the normal requisite institutions of growth, such as private property protections, an independent judiciary, and so on. And why? Entrepreneurs have felt like the institutions were [just about] good enough for them to invest and release some entrepreneurial energy, driven by what economists call marginal incentives. Entrepreneurs didn’t need absolute protection in all things, they had informal relationships that could protect their property, and that was fine for them. Those kinds of institutions, it turns out, may be good enough to get you some investment and growth, especially when you can insert yourself into global supply chains.

We expect there to be corruption, but then the question is, why do we see competitive economic growth in China. Part of the answer is that, ironically, entrepreneurs in China did not have access to the financial system. For a generation, economists have basically decried that, complaining that bloated state owned enterprises get all the access to the Chinese financial sector. But what does that mean? It means that entrepreneurs have had to get financing through foreign direct investment, or through investment of their own retained earnings, or through informal finance, all of which require discipline. If you can only invest based on your retained earnings, you have to earn something and retain it. What you ended up getting in the 80s and 90s was an extremely competitive industrial sector, especially among small and medium-sized enterprises, where companies were trying to insert themselves into global supply chains, to scale up really quickly, to get those contracts, and to turn a profit and reinvest it. There was a lot of discipline in that system.

It’s really hard to have a modern financial sector without rule of law, without transparency, and accountability, while you have a party that refuses to allow markets or law to discipline itself.

In the 2000s, when the financial sector started to open up, well-connected people could get loans, and local governments could help them get loans. That’s when you start to get a lot of companies that don’t earn anything; but because it was a lot easier to get financing from the Chinese government, then invest in real estate, borrow against that real estate, get more money, invest in more real estate, and you get this pyramid scheme.

A question that people are missing is, can you have a monopoly on political control and no rule of law, and a modern financial sector? The evidence so far is, no. It’s really hard to have a modern financial sector without rule of law, without transparency, and accountability, while you have a party that refuses to allow markets or law to discipline itself.

You have also written a lot about how party state capitalism interacts with global markets. Can you describe what you describe as the unintended consequences of that interaction?

Margaret Pearson, Kellee Tsai and I have a paper on this that came out recently. Our view is that, when the party state [perceives there to be a high level] of domestic and international sources of risk, it responds in a number of ways. For example, some of the laws I’ve already mentioned which give the state a wide legal purview to intervene in the actions of firms. Or Made in China 2025, which suffuses state capital well outside the traditional state-owned sector. If you look at almost any competitive firm in a frontier tech sector, and go back right through its ownership, you can find some state investment firms, some local governments. The really interesting thing that’s happened is this blurring of the boundaries between the private sector and the state. It used to be that we had this comfortable diet: there are state owned firms, there are private firms. Private firms are independent and autonomous, and they’re really competitive. But now, legally, financially and politically, there’s less daylight between those firms and the state. That doesn’t mean that they’re always doing the state’s bidding: In fact, a lot of the time they’re subverting the state’s interests.

The question that a government like the United States or any OECD country has to ask itself is, whether China is capable of using such firms as an asset for national security in a way that might compromise our national security? And the answer that most of them have come up with is yes. If I have a Chinese firm in a supply chain, then if the Chinese government wants to secure it, wants to commandeer its assets or wants to weaponize them against me, it could do that and it has the legal foundation to do that. We quote John Cornyn [Republican Senator from Texas], who says very clearly that for the purposes of U.S. government policymaking, there’s no difference between a private firm and the Chinese state. And if you see all Chinese firms as part of the state, then there are all kinds of potential weapons that could be mobilized, whether through choke points, or through intelligence gathering.

As a result, you’ve seen this massive reconfiguration of institutions from the developed world to screen investment, to amplify export controls, to try to figure out extra-institutional ways to go after some of these companies, like what we’ve tried to do to Huawei or the Department of Justice’s China initiative (which is, happily, over). And now we have industrial policy: 10 years ago when I went to DC, people would say, the problem with dealing with China is the two IPs: they don’t protect intellectual property, and they have industrial policy, and we don’t like either one of those things. Now no one talks about industrial policy being a bad thing; instead what they say is look, we’ve got to do these things. If China is doing this, we have to compete with China.

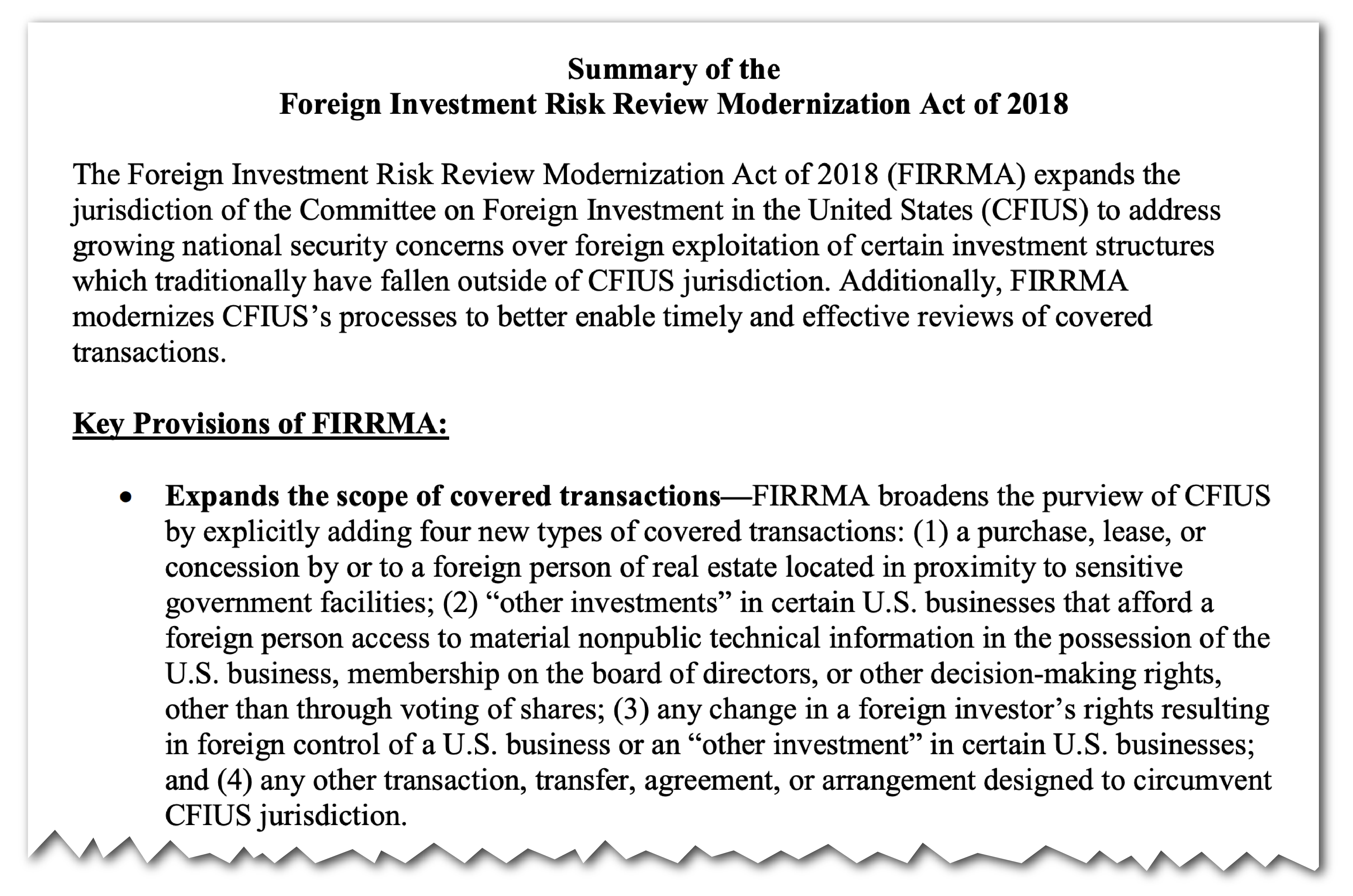

So now we have a really remarkable set of institutions, not all of which are wonderful, not all of which are bad, in the United States. It’s a remarkable thing that the original FIRRMA legislation [which reformed the government review process for foreign investment in the U.S.] in 2018 would have had the Committee on Foreign Investment in the United States review every outbound investment of an American business. That would have been a transformative change to American capitalism and global capitalism. It didn’t end up doing that. But we are going to get some kind of outbound screening mechanism, smaller in scope, in the next calendar year, I would say. What’s really interesting is that for a long period of time, the question people were asking was, how will China reshape the global order? How will they reshape global institutions? Actually China would prefer open institutions for trade and investment, for a variety of reasons. It’s actually the host countries and other trade partners that have erected barriers in response to China.

If you are a U.S. policy maker, should you be viewing SOEs and private firms in China differently?

From a security perspective, it’s hard to argue that the Cornyn perspective is wrong. We now think of everything as dual use. If you’re looking at a firm in quantum or AI or any of those sectors, from a risk management standpoint, it’s not appropriate for the United States to say, ‘Oh, it’s a private firm, it’s fine.’ China literally has the legal foundation to commandeer the assets of that firm to use in the service of national security, which it defines quite broadly. From that perspective, when you think about what could happen in the future, you have to think of those firms as potential extensions of the Chinese state.

Instead of thinking of every action of a firm or an individual as revealing some data point in some master plan, we should realize that it’s all pretty chaotic.

What the fallacy would be is to assume that every firm’s action reveals something about what the state wants to do. If we’re trying to learn about what China wants, how it behaves, how Chinese firms work, and then we say they’re all extensions of the state and acting as extensions of the state, we miss a lot of the story, which is the chaos of how China’s industrial policy works, the chaos of the financial sector, the ways in which private firms are subverting the interests of the Chinese state, and the kind of learning and experimentation that’s part of what China has always done in its economy and in other realms. Instead of thinking of every action of a firm or an individual as revealing some data point in some master plan, we should realize that it’s all pretty chaotic.

What is an example of a mistake that comes out of thinking that everything is a master plan?

One example is the idea of debt trap diplomacy. The idea that every time China’s renegotiating something with a country it’s lent money to means that China intended for it to happen that way. In fact, a lot of what’s happening is deeply unintentional and unexpected. In Sri Lanka, there was an extremely surprising presidential declaration. The guy who ran for president was surprised he won. And then he’s the one who renegotiates with China on the port and everyone just assumes what China really wanted was to get the port. Whereas that really was a chaotic unfolding of decisions that were made as part of a political economic and commercial calculus.

So at this point, there’s $600 billion dollars of Chinese lending out in the world, and we have no idea how that’s going to be unwound. I don’t really see it all being paid back in full. But that doesn’t mean that every time there’s an equity investment or renegotiation of that contract that’s the outcome China intended. Appreciating contingency and unintended consequences, and then learning as China’s learning, rather than feeling like we’re watching the revelation of a premeditated plan. That makes our foreign policy less appreciative of the ways in which China changes and learns than it could be.

Katrina Northrop is a journalist based in Washington D.C. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina

{kind=link}