Benn Steil is the director of international economics at the Council on Foreign Relations, where he has spent more than two decades writing about the intersection of money, markets, and geopolitics. He is the author of The Battle of Bretton Woods, The Marshall Plan: Dawn of the Cold War, and Money, Markets and Sovereignty. He is currently at work on a new book, One World, which examines competing visions of global order. In this lightly edited transcript of a recent conversation, he talks about the themes of that book, how the actions of the Trump administration are contributing to the breakdown of the post-World War II settlement — and why the ideas of a German political theorist who was a member of the Nazi party have become influential among some thinkers in China.

Illustration by Lauren Crow

Q: You’ve written recently about the demise of the WTO and the renewed relevance of the General Agreement on Tariffs and Trade (GATT). Was the WTO destined to fail? And why is the GATT the relevant model for thinking about what comes next?

A: The WTO really was the high point of American universalism after the end of the Cold War. It was created in 1995, and it took the GATT forward many steps. It expanded the scope of trade covered by international rules, but it also created a form of supranational government that we haven’t replicated in any other area. It’s not intergovernmental; it’s legitimately supranational. There’s a dispute settlement body that adjudicates trade disputes, and an appellate body that can hear appeals, and their decisions have been extremely consequential.

What destroyed it was the “China Shock” beginning in the late-2000s. When China joined the WTO in 2001, it had a very small economy compared to what it is today — today, it’s almost fifteen times larger. The distortions China was introducing into the world trading system were not that significant in 2001. But by the time we get into the 2010s, Chinese state capitalism really started to distort international trade. Rapid integration between the U.S. and Chinese economies decimated electorally important constituencies in places like Pennsylvania and Ohio, and the rest is history.

| BIO AT A GLANCE | |

|---|---|

| AGE | 62 |

| BIRTHPLACE | NY, NY, USA |

| CURRENT POSITION | Director of International Economics, Council on Foreign Relations |

The China Shock had very powerful political impacts, particularly in terms of fueling polarization and enabling the emergence of someone like Donald Trump, who could make a credible case to the American people that the interests of political elites were at odds with the general public’s. The deep economic integration that we began pursuing with China in the early 2000s led to the current situation in which the Madisonian system of checks and balances is breaking down. Tariff policy is now being set entirely by the executive, when the Constitution makes absolutely clear that those powers are reserved to Congress.

What we’ve learned is that the WTO is not able to discipline Chinese behavior. Massive government subsidies to build up strategically important industries did not technically violate WTO rules because they weren’t explicitly linked to export performance. But when the United States tried to protect itself through protectionist measures, the WTO found some of those objectionable.

| BOOK CORNER |

|---|

| Favorite book of all time: John Williams’ Stoner — the perfect novel. Favorite recent read: Ian McGilchrist’s The Master and His Emissary — a life-changing, mind-altering fusion of neuroscience, philosophy, and history. |

Under the Obama administration, we began to see the beginnings of a pushback against our own universalism. Obama refused to reappoint an American appellate judge for the dispute settlement mechanism. Under Trump’s first term, that got extended permanently — since then, not a single new appellate judge has been approved, and that body is now inquorate: it lacks the minimum number of judges necessary to make rulings. This supranational mechanism that we built in the mid-1990s is effectively dead.

The second thing that killed the WTO is that we abused the rules we created by declaring all protectionist measures to be motivated by “national security.” Our legal argument was that those could not be adjudicated by the WTO. And in short order, the world started following us. You had countries imposing protection for cocoa beans or door frames or alcoholic beverages and claiming it was about national security. Most favored nation status (MFN) — meaning if you make concessions to one WTO member, you have to extend them to all — is effectively dead. The dispute settlement mechanism is dead. It’s been a big failure of supranationalism.

| MISCELLANEA | |

|---|---|

| FAVORITE MUSIC | I directed a cappella groups in college and grad school |

| FAVORITE FILM | Memento — complex but utterly engrossing |

| MOST ADMIRED | Epictetus – the wisest and most insightful of the ancients |

So the original sin of the WTO was that it was rooted in the expectation of convergence: the idea that the global economy would become filled with democratic market economies, the [Francis] Fukuyama vision. But you believe the GATT was a more realistic trade order, and that’s why it worked.

The GATT was much less ambitious, but it was enormously successful because of its limited ambitions. It was created in 1947 with only twenty-three countries initially. Tariffs came down very dramatically over many decades. And the success of the GATT was what led us to try to expand it into the WTO.

Why was the GATT successful? The answer is pretty simple: we demanded systemic compatibility. We negotiated very differently with the Soviet Union in 1947 than we did with the Chinese going into their WTO accession in 2001. We insisted that Soviet international trade had to follow market principles and be transparent about the mechanisms used to conduct trade. The Soviets were unwilling to do this and so they were not permitted to join the GATT. That was perhaps the single most important reason the GATT was successful. Reciprocal tariff reduction only works when prices and production respond to market incentives.

…there are aspects of U.S.-China trade that need to be controlled or even eliminated… But there are also certain aspects of Chinese state capitalism that we should exploit… We need to be careful that we’re not closing the door to trade that actually benefits American industry.

We did go into the GATT creation process with ambitions similar to the WTO. It was going to be called the ITO, the International Trade Organization. Some of the early models included labor market regulation, stuff we only started reviving in the 1990s. But we figured out pretty quickly that this couldn’t be done without giving countries like the Soviet Union the opportunity to opt out of these rules, and we decided we weren’t going to do that.

In the case of China, it’s fascinating reading the comments of American politicians from the late 1990s. Bill Clinton argued that once China came in, it would inevitably be forced by these great historical winds to fulfil Fukuyama’s vision and turn not just into a market economy, but over time into a liberal, democratic nation. And of course, that turned out to be very wrong.

U.S. Trade Representative Jamieson Greer has proposed a U.S.-China Board of Trade to govern bilateral trade negotiations. You’ve written about a modernized, “plurilateral GATT-style arrangement.” Is this the same thing? What do you make of Greer’s proposal?

I would say it’s the opposite of the GATT. It’s not meant to liberalize trade. It’s meant to go in the other direction entirely and institutionalize state control of every aspect of trade.

You can make a case that with regard to China we have to have some forms of state control on our side, because the Chinese system is almost entirely directed by the state. But it’s somewhat Pollyannaish to believe that the confrontations we’re having with the Chinese will somehow be eliminated just by setting up a new institution through which we can talk through our mutual restrictions. These confrontations are not going to be quashed by an institution. They’re going to continue to be managed through both sides using offensive weapons when they feel they need to in order to defend their interests.

Greer has also claimed that the bilateral deals the administration is striking amount to a new “Turnberry system” — a reference to Trump’s golf course, where he met to negotiate with Ursula von der Leyen in July 2025 — i.e., a successor to Bretton Woods. He’s also invoked the scale of the Marshall Plan to describe recent foreign investment commitments into the United States. You wrote the book on both. How seriously should we take those comparisons?

We shouldn’t take them seriously at all.

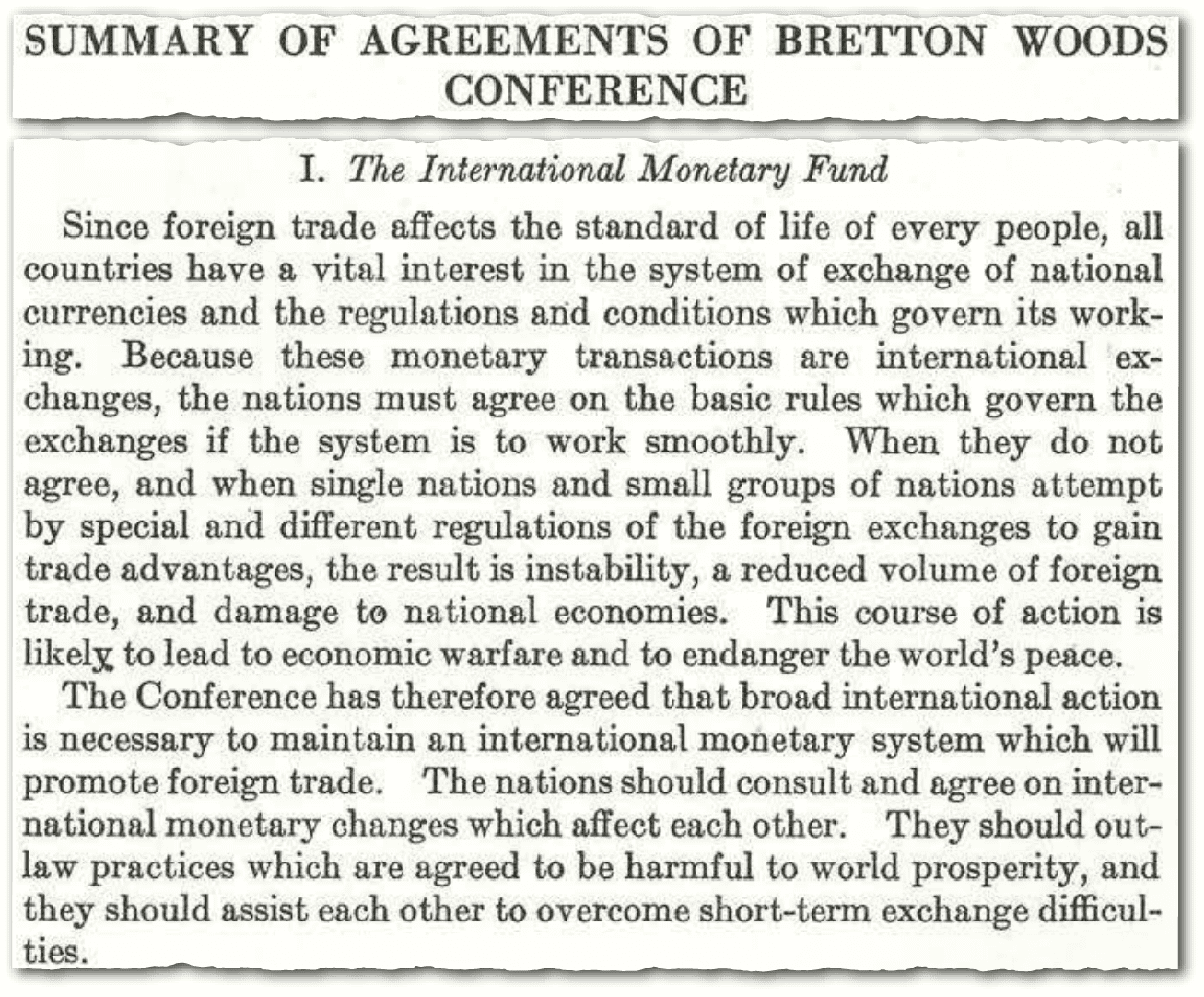

Bretton Woods, for all its flaws — and there were plenty — its ultimate aim was to underpin a new liberalized global trading regime. The entire architecture was designed so that countries could lower barriers to trade with confidence that exchange rates would remain stable and that balance-of-payments crises wouldn’t force them back into protectionism. It was not to institute a system of managed trade conducted on an ongoing bilateral basis.

To compare what this administration is doing to Bretton Woods is really ridiculous. The aims are entirely different. I don’t even think what the Trump administration is doing merits the term “system,” because there’s nothing systematic to it. The president is constantly rewriting the rules from week to week, often on grounds entirely separate from economic or security concerns, sometimes purely political, sometimes personal when he has a particular animus against a particular world leader.

With regard to the Marshall Plan, that’s comparing apples and oranges. The Marshall Plan was a grant-in-aid scheme — a massive one. We were providing enormous cash grants to Europe to allow them to rebuild their productive capacity at maximum speed after World War II. And it’s worth emphasizing that the Marshall Plan required the Europeans to cooperate with each other in deciding how to allocate the aid.

That cooperative framework was actually more important, in the long run, than the money itself, because it laid the groundwork for European integration. The so-called investment commitments that American trading partners are making today as part of trade deals with the Trump administration are, first of all, in many cases not even real. They’re just announcements, and then we don’t see them being fulfilled. In most cases, they’re just echoes of previous commitments.

They are also not gifts to the United States in the way that Marshall aid was for Europe. These are investments that the EU, Japan, Korea, and others are making in calculation of their own financial interest. They may or may not actually help us economically. In terms of the administration’s goal to reduce the U.S. current account deficit, they clearly push in the opposite direction. The current account and the capital account are mirror images of each other. If we increase the U.S. capital account surplus by having more investment coming into the United States, necessarily, as an accounting identity, we’re going to have lower net exports. There’s enormous confusion within the administration about what these investments are supposed to accomplish.

What do you make, in general, of the Trump administration’s use of tariffs? Aren’t tariffs the right tools for fighting Chinese protectionism?

Some of it is clearly defensible. For national security reasons, there are aspects of U.S.-China trade that need to be controlled or even eliminated. We don’t want to depend on China for certain forms of technology and things like rare earths; we obviously need to diversify our sources there.

But there are also certain aspects of Chinese state capitalism that we should exploit. About half of what we import from China are intermediate goods that our manufacturers need to be globally competitive. If China wants to subsidize steel production and have massive overcapacity in steel, U.S. industry benefits enormously from importing underpriced Chinese steel. American steel-using industries employ about fifty times as many American workers as American steel-producing industries. We need to be careful that we’re not closing the door to trade that actually benefits American industry.

Tariffs are a blunt instrument. They have trouble distinguishing between goods that pose genuine security risks and the inputs that American manufacturers need to compete globally. And the costs fall overwhelmingly on American consumers and businesses, not on Chinese exporters. When you impose a tariff, the American importer pays it, and most of that cost gets passed through to the end consumer. We’re taxing ourselves in order to punish China, and in some cases, we’re punishing the wrong American industries in the process.

What’s your baseline view of the Chinese economy in 2026?

I don’t know any credible economist, Chinese or Western, who would look at the Chinese economy and not say it needs significant reforms, in particular, to boost domestic demand. You hear that from Chinese economists all the time. This is not controversial. The big problem is not that Xi Jinping and his deputies don’t understand this. It’s just not their priority. They’re willing to sacrifice economic efficiency in order to dominate certain global sectors.

At one level, this is just pure mercantilism, but at another level, it’s warfare. It’s a way of saying: if we dominate certain industries, it makes it more likely that we will be able to dominate militarily in our region and eventually expand our ability to enforce our interests elsewhere in the globe. They are basically following what they see as the American model since the late nineteenth century. And there’s a historical logic to this that Americans should understand, because we did more or less the same thing. The United States was the most protectionist major economy in the world for decades in the late 1800s.

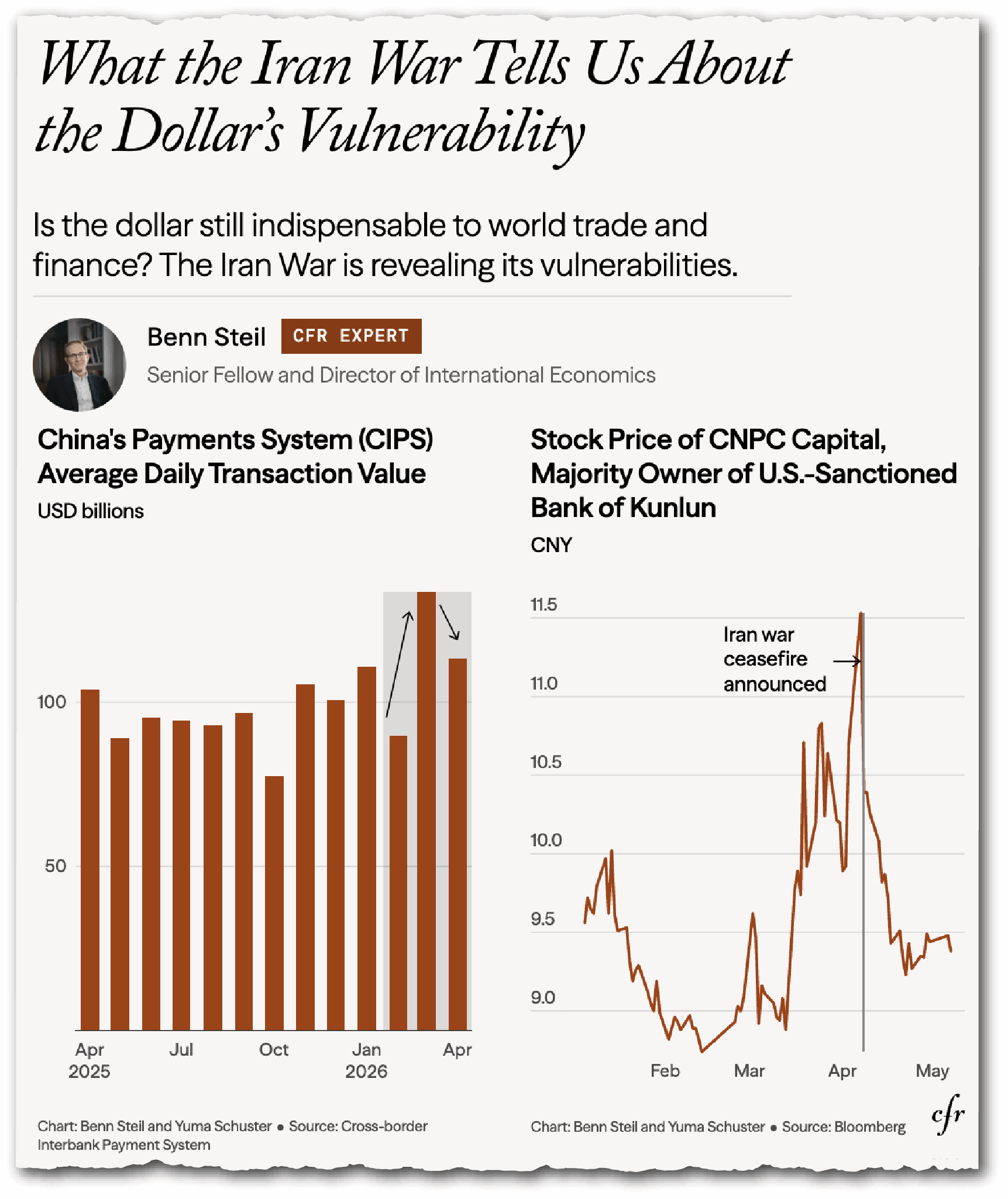

There’s a lot of discussion about threats to dollar dominance from the Chinese renminbi. How significant is that threat? And what does it mean for the effectiveness of sanctions as a tool of U.S. foreign policy?

The reason we love sanctions is that we can cause pain to our adversaries while causing relatively little pain to ourselves. But like an antibiotic that happens to be effective when used in a very limited way, once you start over-prescribing it you encourage bacteria to mutate and become resistant. We are basically encouraging the world to take steps to immunize themselves from American sanctions regimes.

What we’re seeing in international payments is twofold. First, a shift, not enormous yet, but clearly a shift, from the U.S. dollar to RMB. And second, that flow is not being processed through Western machinery, the SWIFT system. It’s moving to the new Chinese CIPS system. We’re still talking about a relatively small share of global transactions. The RMB is nowhere close to rivaling the dollar in volume; on SWIFT, it doesn’t even rank ahead of the Canadian dollar. But what matters is that China’s alternative plumbing is growing, and it’s plumbing we have little visibility into.

It’s not so much that [the Chinese] want to set monetary policy for the world… But they’re trying to convince the market that the RMB is, in fact, a stable alternative to the dollar, in the way that a dollar stablecoin might be in the cryptocurrency environment. It’s a very interesting strategy.

I argued in a recent blog post that this is being driven fundamentally by the world’s desire to immunize itself from U.S. sanctions, not by some desire to just move away from the dollar. The Iran conflict establishes this. The U.S. attacked Iran at the very end of February. What you see in early March is a sharp spike upward of RMB transactions on CIPS. Iran is insisting on payments for ships to move through the strait to be made in RMB or alternative currencies. The United States is threatening to sanction any countries that conduct trade with Iran or aid Iran. So the world is moving to RMB and CIPS payments to avoid the U.S. sanctions regime.

But is this a secular shift? No, because as soon as you see the U.S. ceasefire announcement, those volumes drop. The stock price of one major Chinese financial intermediary outside the U.S. clearing system had soared before the ceasefire and then plummeted afterwards. The market was saying: ceasefire, we’re headed back to normal, we can go back to dollar-based transactions. These shifts are clearly being motivated by sanctions avoidance, not a secular desire to move away from the dollar. China’s parallel financial infrastructure — CIPS, bilateral swap lines, commodity contracts in RMB — doesn’t add up to a serious secular challenge to the dollar system. These are tactical things, hedges that work at the margins.

The Chinese are using a very interesting strategy. It’s not so much that they want to set monetary policy for the world. How are they selling RMB usage to the rest of the world? By fixing its currency. It’s basically nailed to the U.S. dollar. It’s adjusted on a minor basis for political purposes. For example, it appreciated a bit recently in the run-up to Donald Trump’s state visit to Beijing. But they’re trying to convince the market that the RMB is, in fact, a stable alternative to the dollar, in the way that a dollar stablecoin might be in the cryptocurrency environment. It’s a very interesting strategy.

We’ve been talking about how the U.S. is reshaping the international trade and monetary order. But what does all of this mean for Europe?

Europe ideologically is devoted to multilateralism, because of course the EU was built on top of a framework that transcended national sovereignty. The idea of international rules is very important to the Europeans. And the so-called “liberal rules-based order” has functioned very nicely for Europe since World War II, in particular, our underwriting of their security, which enabled them to focus on economic and political integration.

But Europe has still really struggled to cohere as a political union. You’ve got 27 countries that can’t agree on fiscal policy, can’t agree on defense; and for decades they didn’t have to, because the Americans were handling the hard stuff. That’s the thing to remember: globalization depended on U.S. security guarantees, not the other way around. The liberal trading order didn’t produce peace; American security guarantees produced the conditions under which liberalized trade could flourish.

That framework is coming apart as the United States makes clear it’s really not interested in underwriting Europe’s security anymore. Europe has tried to defend the WTO and multilateralism, but in order to do these trade deals with the United States and avoid heavy U.S. tariffs, it’s been forced to move away from its dedication to the MFN regime. There’s a big dispute within the EU right now about whether they should make a formal proposal within the WTO to replace MFN with something else.

This dovetails with your recent interest in Carl Schmitt, the German jurist who has become a kind of prophet for explaining the fragility of liberal institutionalism. In Foreign Affairs, you wrote that when it comes to predicting the course of political history, Schmitt, not Fukuyama, is who we should pay attention to.

In the late 1980s, Fukuyama famously put forward his end-of-history thesis. It was this huge ideological project. It captured the public’s imagination in the 1990s, and it still does. And what we’ve heard continuously from U.S. foreign policy commentators and theorists — people like John Ikenberry — is that the Chinese really don’t have any alternative to the rules-based liberal world order. They’re just “spoilers,” or whatever, and they don’t have any vision.

I decided about a year ago to start digging into this. Is it really true that the Chinese don’t have a coherent alternative framework? And I was shocked to find that Carl Schmitt, the so-called “Crown Jurist of the Third Reich,” had become enormously influential in academic and policy-sensitive circles in China. References to him on Chinese scholarly databases soared after 2003.

You have Chinese scholars like Liu Xiaofeng who have made their careers mapping out what China’s vision for world order should be, informed explicitly by Schmitt’s thinking. They take Schmitt very seriously. And the reason Schmitt is becoming influential in Chinese political circles is that his ideas provide the government with a framework for justifying the path it’s on — perhaps ironically, one rooted in Western legal philosophy.

From what I’ve gathered, Schmitt has been drawn on by Chinese intellectuals to justify the total power of the state and to articulate dissatisfaction with, and alternatives to, Western liberalism.

Right. The Chinese argue, as Schmitt showed, that liberal democracy is very fragile. It doesn’t deal with crises well. It doesn’t deal with the realities of political power. It doesn’t deal with the importance of geography and the idea of regional order. Schmitt’s concept of Großraum — regional orders structured around dominant powers, each with its own political and legal character — maps remarkably well onto what China says it wants: a multipolar world in which great powers exercise predominance within their own spheres and no single power presumes to set universal rules for everyone else. And the fact that the United States is now reviving the Monroe Doctrine only reinforces for China the idea that they are headed in the right direction by aiming to dominate the Asia-Pacific.

The United States is abandoning its universalist commitments, walking away from the WTO, weaponizing the dollar, treating alliances as transactional. It’s vindicating Schmitt’s worldview in real time. We are becoming proof of his sense that liberal universalism was always a mask for great-power hegemony. Carl Schmitt wouldn’t be surprised by any of this.

Addis Goldman is a freelance writer and researcher based in Seattle, Washington. He previously worked at the Special Competitive Studies Project. His writing has appeared in Foreign Affairs, The Wall Street Journal, War on the Rocks, and elsewhere.