Bankers on Wall Street are champing at the bit to take the United States’ largest artificial intelligence firms public. Their counterparts in China are having more luck.

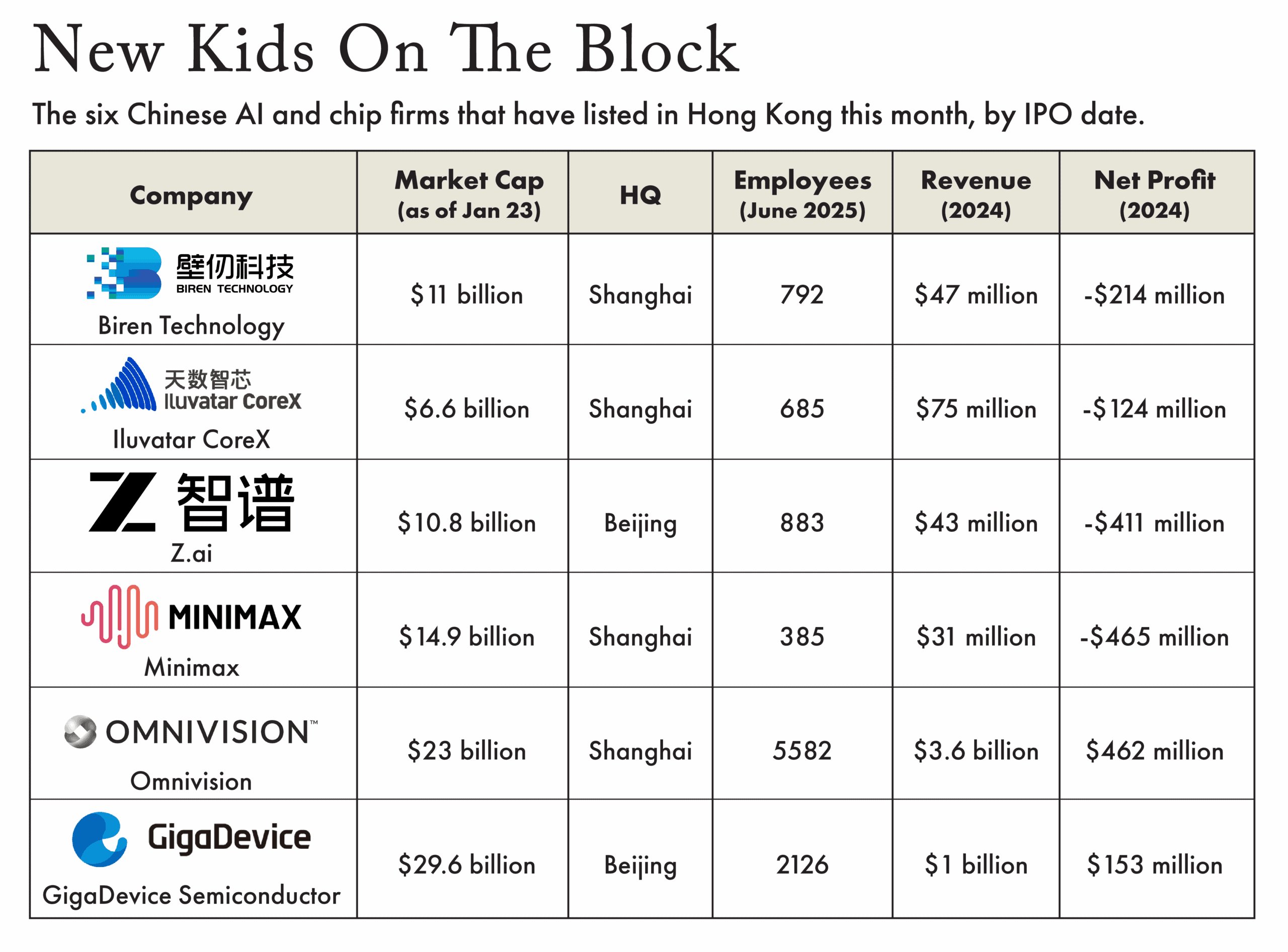

Six Chinese AI and chip companies have listed in Hong Kong already this month, making up more than half of the new firms to debut on the city’s exchange in 2026. These half-dozen listings have together raised $3.6 billion, almost 60 percent more than the amount raised by all Hong Kong initial public offerings during the first quarter last year.

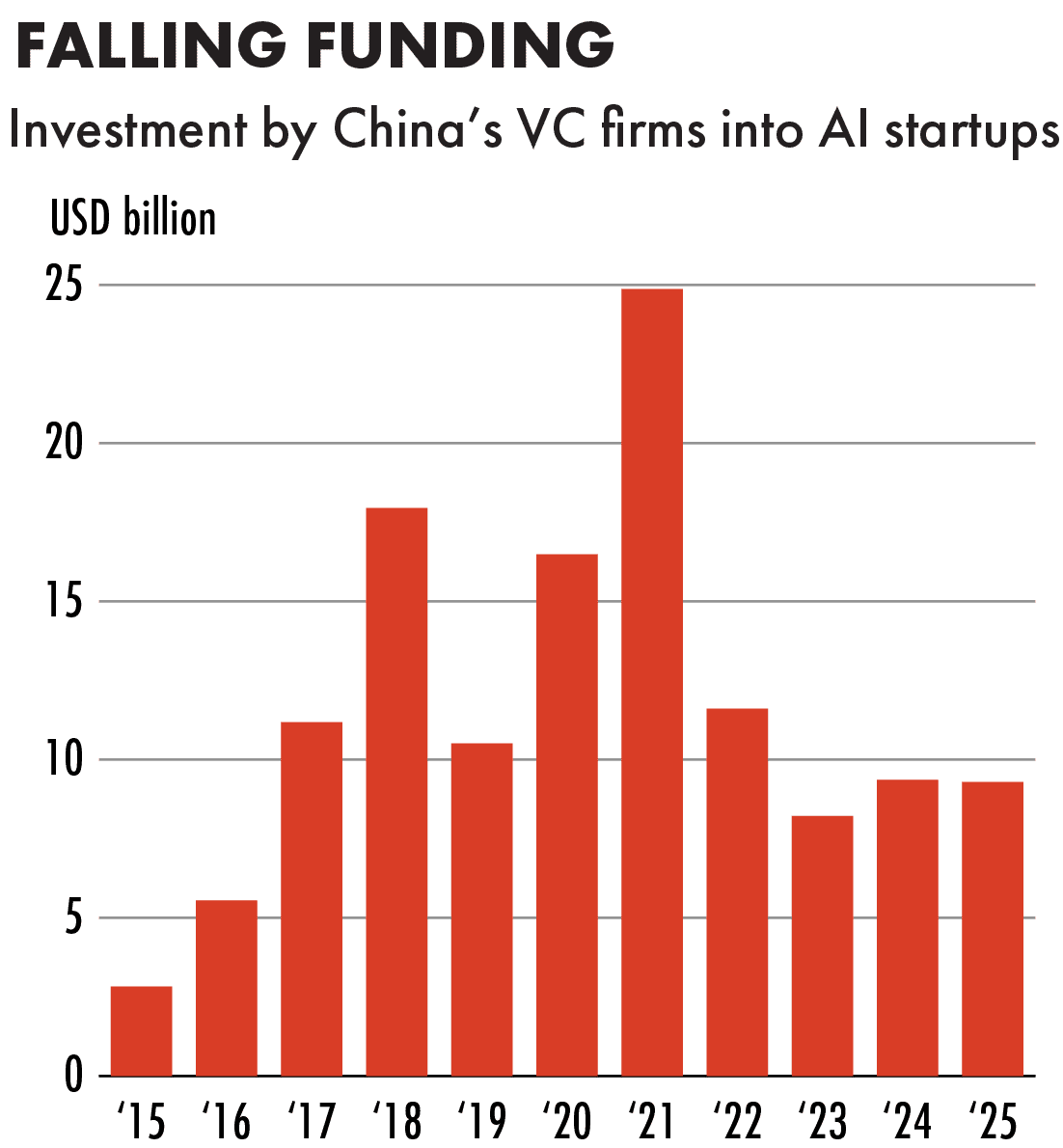

The turn to public markets is partly a result of venture capital funding drying up in China. China’s VC firms invested $9.3 billion in AI startups last year, down from a peak of $24.9 billion in 2021, according to data provider Pitchbook. The U.S. firm OpenAI, by contrast, says it raised $40 billion in private capital last year alone.

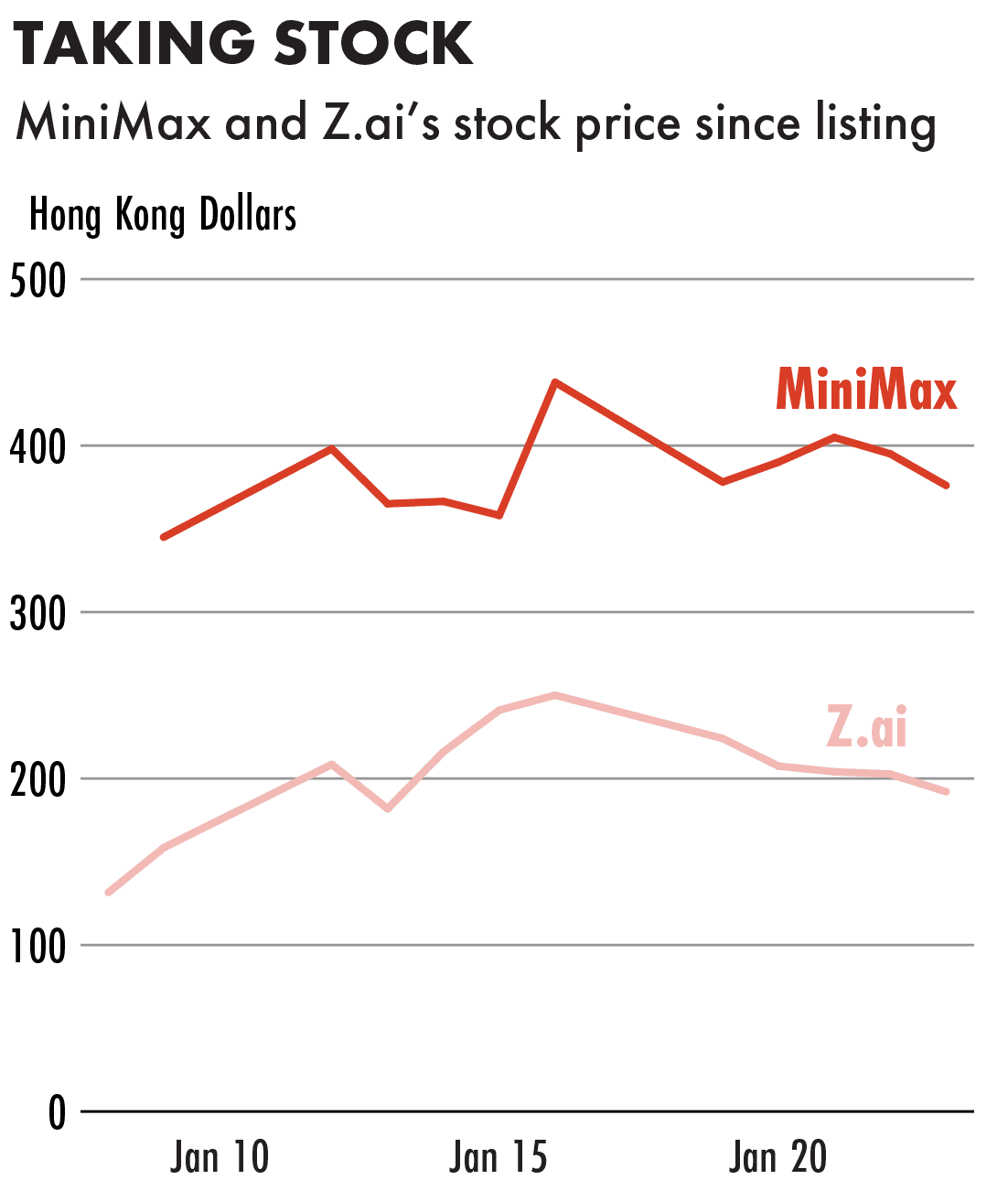

So far markets have rewarded Chinese AI and chip companies. Each of the six that listed this month has seen its stock climb from the IPO price on the back of hefty demand from institutional and retail investors. Shares in MiniMax and Z.ai, two developers of large language models, doubled from their opening price, though Z.ai’s share price has since tapered. Retail investors oversubscribed to both offerings by more than 1,000 times, according to securities filings.

The demand underscores how investors are responding to China’s pursuit of technological self-sufficiency by betting on rapid growth in its AI and chip firms — regardless of whether they make money and even though there is still a high level of uncertainty around which companies will emerge as the AI industry’s winners.

“In the public equity markets in China, you are always trying to invest with the tailwinds of policy supporting you,” says Eric Wong, chief investment officer of hedge fund Stillpoint Investments. “At the moment, it’s a world of enthusiasm.”

Under Xi Jinping, China has made domestic production of semiconductors and other advanced technologies a national priority, as U.S. export controls stifle sales of American chips to Chinese companies. Among the recommendations that the Central Committee of the Chinese Communist Party has made for the country’s upcoming 15th five-year plan are calls to “accelerate self-reliance in high-level science and technology” and “increase the proportion of private investment.”

They intend to list these high-valuation and high-uncertainty IPOs on the more mature Hong Kong stock market with a higher proportion of institutional investors, rather than on the retail-dominated A-share market, so as to prevent risks from triggering market volatility.

Shen Meng, director at Beijing-based investment bank Chanson & Co.

Stock exchanges in mainland China and Hong Kong have meanwhile created exceptions to listing requirements to make it easier for firms in priority sectors to go public — as long as they invest in R&D.

“The Chinese have been masters at signaling,” says Fritz Demopoulos, a tech entrepreneur and founder of VC firm Queen’s Road Capital in Hong Kong.

A decade ago, many of China’s top internet companies chose to list on the Nasdaq. Today China’s regulators are encouraging domestic AI and chip firms to list in Hong Kong rather than on mainland exchanges such as those in Shanghai and Shenzhen (known as A-share markets), to support their efforts to compete with American stock markets for tech IPOs, says Shen Meng, director at Beijing-based investment bank Chanson & Co.

“They intend to list these high-valuation and high-uncertainty IPOs on the more mature Hong Kong stock market with a higher proportion of institutional investors, rather than on the retail-dominated A-share market, so as to prevent risks from triggering market volatility,” Shen says.

Despite the drying up of VC funding in China, the current crop of listings are proving lucrative for a select group of firms on their previous investments. HongShan, formerly known as Sequoia Capital China, has backed three of the companies coming to market, while Qiming Venture Partners and IDG Capital have each invested in two, according to their prospectuses. At current market prices, IDG — which is backed by pension funds in U.S. states — has gained more than $300 million from its investment in MiniMax, according to Wire China calculations.

The meteoric performance of rapidly growing firms like MiniMax and Z.ai, neither of which has yet recorded an annual profit, has raised questions of whether the AI boom is sustainable. China’s market regulator is considering whether to tighten the criteria for mainland companies looking to list in Hong Kong, Bloomberg reported on Friday, due to concerns over deal quality.

“If this were the Nasdaq, or North America, it wouldn’t be normal,” says Zhang Jiang, a Beijing-based equity research analyst who formerly covered Chinese internet companies at UBS, of the skyrocketing share prices. “The fundamentals are okay,” he adds, but if companies cannot maintain triple-digit revenue growth “valuations are going to just collapse.”

Maintaining that level of growth will be a particularly daunting challenge in China, where companies across industries fiercely compete with one another. “Somebody’s going to come out and say, ‘I will offer you a lower price,’ just to get market share,” Zhang says. “And that just ruins the party for everybody else.”

There is also the risk that tech firms will lose political favor. The consequences of a sudden change in government policy can be severe: In 2020, regulators blocked financial firm Ant Group from completing what was set to be the world’s biggest ever IPO after co-founder Jack Ma criticized China’s banking rules. The next year, China published regulations clamping down on the then lucrative online tutoring sector. The move wiped out billions of dollars in market cap for such companies.

There is an incentive to allow these companies to be financed so that they can compete toe to toe, from a technology perspective, with the best businesses in the U.S.

Eric Wong, chief investment officer of hedge fund Stillpoint Investments

Tech founders may now be seeking to go public while they are in the government’s good graces. But observers say a crackdown on the sector is unlikely. For one, regulators are being more proactive than they were with the previous generation of tech giants. They have, for instance, already proposed rules that will prevent AI chatbots from generating content that damages a user’s mental health or “engages in illegal religious activities.”

Ten years ago, “the [Chinese] government was seeing the success of these [big tech firms] and just didn’t have the capacity to regulate,” says an executive who works in the Chinese tech sector and was not authorized to speak publicly. “It’s a completely new generation of regulators now. They may not be perfect. They may not get it right, but they certainly have a view on what it is they want to regulate.”

Perhaps more important is that Beijing’s interests are likely to remain aligned with its AI and chip firms. “There is an incentive to allow these companies to be financed so that they can compete toe to toe, from a technology perspective, with the best businesses in the U.S.,” says Wong, of Stillpoint.

Many investors expect 2026 to prove a banner year for tech IPOs. Firms including memory chip maker CXMT and Baidu’s semiconductor unit Kunlunxin have already filed paperwork to list. Each could raise more than $1 billion.

“When there’s a window of opportunity with attractive valuations, private companies will definitely want access to them,” says Ray Wong, founding partner of Asymmetry Capital in Hong Kong. “The momentum will continue.”

Whether stocks can continue to soar is another question. AI is still in its early stages, and no provider of large language models owned more than a tenth of the Chinese market as of 2024, according to Z.ai’s prospectus. At some point, investors may start to become more discerning about the relative merits of Chinese AI and chip companies looking to list.

“As with any IPO cycle, the best quality ones come to market first. That’s something that investors will be watching carefully,” says Eric Wong.

Chip firms meanwhile must compete not only with each other but also the behemoths Huawei and Nvidia — if Washington and Beijing allow it to sell its products to China.

“There’s some healthy skepticism,” says Demopoulos, of Queens Road Capital. But “one of them will be the next Tencent.”

Noah Berman is a staff writer for The Wire based in New York. He previously wrote about economics and technology at the Council on Foreign Relations. His work has appeared in the Boston Globe and PBS News. He graduated from Georgetown University.