China’s declining real estate market has been a defining feature of its economy during the last five years. Over that time, the sector has been transformed, with a total reshuffle of the country’s top property developers, collapsed sales and investments, and a glut of unsold property.

This week, the Wire takes a look at the transformation that has taken place, and whether there are any signs a turnaround is imminent.

TAKING STOCK

In 2020, as the world grappled with Covid, Chinese regulators set their sights on cutting the massive housing market down to size. The government introduced requirements known as the “three red lines” to deter excessive borrowing among property developers. The move triggered the property market’s slide, as it forced overstretched companies to restructure their finances, or fail.

The three red lines are now quietly fading away. On Thursday, Chinese media reported that regulators are dropping the requirements, with some property developers revealing they have not been reporting the three key metrics for months.

The news further boosted a month-long rally on the Hang Seng Properties Index, which consists of 28 mainland-listed property developers. A series of policy communications at the beginning of the year kicked off the surge in investor confidence: Qiushi, an official publication of the Central Committee of the CCP, called for improvements and stabilization in the real estate market on New Year’s Day. A few weeks before, China’s Minister for Housing Ni Hong identified stabilizing the real estate market as the top priority in the new year.

NEW KIDS IN TOWN

The shakeout instigated by the three red lines policy has led to a major reshuffle of China’s top property developers. Stricter financial regulations, combined with the economic downturn during Covid, have proved toxic for companies already on the edge.

Just under half of the top 100 property developers in China have dropped from the rankings since 2021, according to findings from China Index Holdings, a real estate data platform.

The top companies are also selling less. In 2021, 41 companies had annual sales exceeding 100 billion yuan compared to just 10 in 2025. Sales at Poly Developments, last year’s top developer in China, amounted to just 253 billion yuan ($36.2 billion) in 2025 compared to 543.9 billion yuan ($85.3 billion) in 2021.

The CIH data shows that four-fifths of the 30 developers that ranked in the top 100 for both sales and land acquisition are state-owned. Poly Developments is a subsidiary of China Poly Group, a state-owned military conglomerate, for example, while the number two-ranked company Greentown’s largest shareholder (23.7 percent) is China Communications Construction Group, a state-owned enterprise.

“Most private developers have either gone bankrupt or been taken over, and you have a more or less de facto nationalization of the property development sector,” says Nicholas Borst, Director of China Research at Seafarer Capital Partners. “You had a shakeout of private developers in favor of state firms that wasn’t entirely market-based or even fair.”

NO MONEY, MORE PROBLEMS

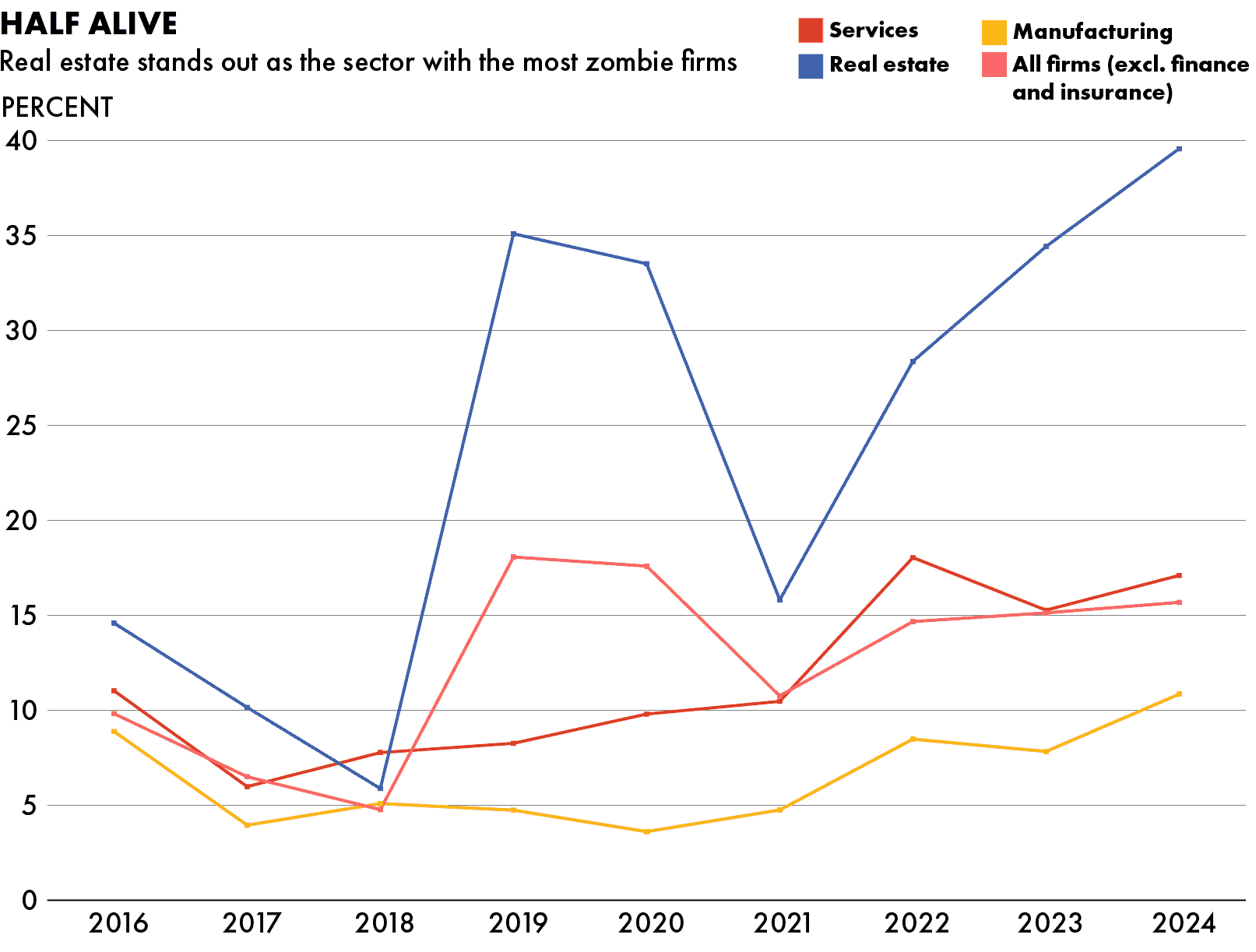

Despite the shakeout, China’s property sector is still awash with zombie firms — companies that do not earn enough to cover their interest expenses. Nearly two-fifths of real estate firms in China are zombies and would be insolvent if not for continued bank funding or other support, according to research from the Federal Reserve Bank of Dallas. Many have become perpetual money pits with no clear way out.

Take Vanke, once China’s largest developer. The company reported its first loss in two decades in 2024, and has continued to spiral since. It owes more than $50 billion in debt and is in an extended battle with its bondholders about extending the terms of their bonds. Vanke’s main shareholder is state-owned Shenzhen Metro, which manages subways. It has provided more than 29 billion yuan ($4.1 billion) to help Vanke repay its debt, according to S&P Global.

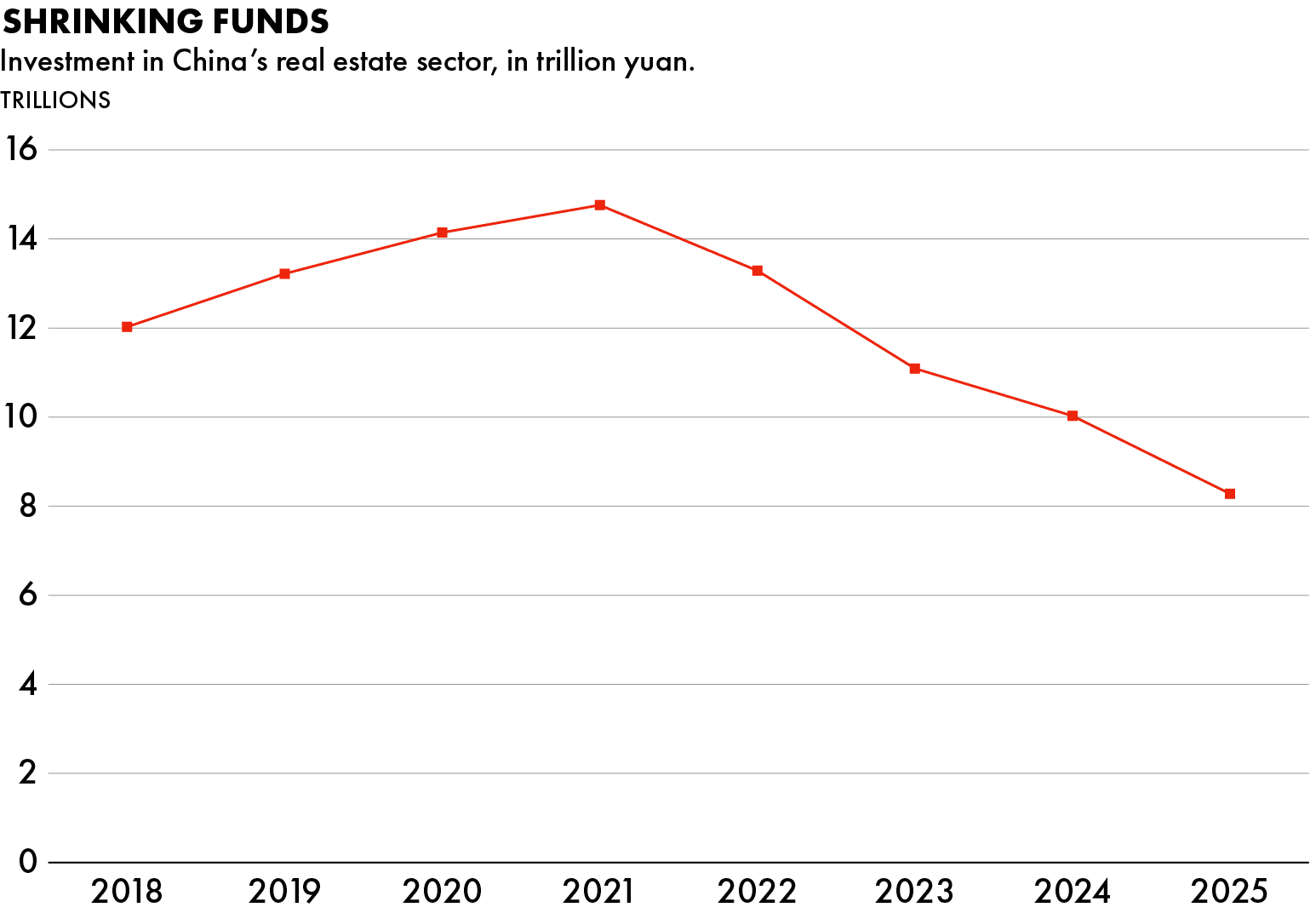

Overall investment in the real estate sector has contracted steadily since 2021, however. Data from the National Bureau of Statistics shows that investment in real estate development decreased 17.2 percent in 2025 to 8.28 trillion yuan ($1.19 trillion).

“You have this confluence of events where, at the same time, China is removing sources of financing for developers. It’s also gutting their demand,” says Borst. “In my opinion, that’s the one-two punch that really pushed a lot of developers off the cliff and into bankruptcy.”

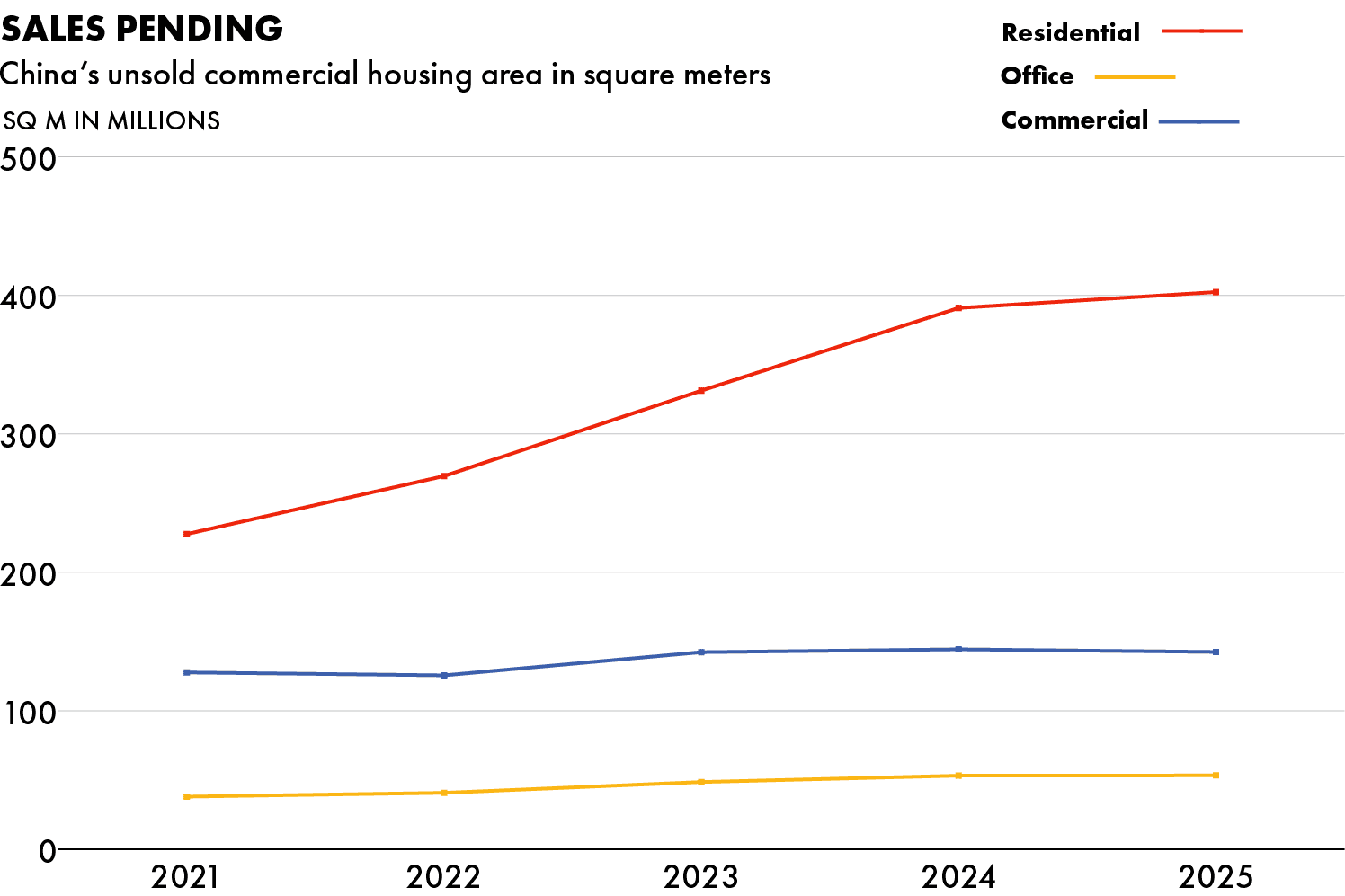

FLOODED WITH FLOOR SPACE

The property market’s woes illuminated the excess supply that existed at the time. As the market has slowed, the total area under construction in China has decreased by 2.7 billion square meters over the past five years, according to the NBS.

Curtailing construction has not been enough to save the sector from a ballooning stock of unsold property, particularly among residential developments, thanks to still-weak demand. Correcting this imbalance is a major focus for the Ministry of Housing and Urban–Rural Development in the new year, according to Chinese media reports.

One bright spot is the slowing rate at which unsold property has accumulated in 2025. Inventory of unsold residential property only increased 2.9 percent from the previous year in 2025, compared with an 18 percent increase between 2023 and 2024.

Despite there being more than enough residential property to go around, homebuyer confidence has not yet recovered. Before the crash, developers pre-sold homes that had not yet been completed or even begun, with consumers often investing in nothing more than a brochure. Restoring consumer confidence in purchasing new homes will be a tough sell for policymakers.

“In terms of the overall economy, China really hasn’t found something to fill the hole left by housing,” says Borst. “From one perspective, they prevented a more massive housing blow up. But at the same time, it’s very clear that they are still dealing with the fallout of the housing correction five years after it began.”

Savannah Billman is a Staff Writer for The Wire China based in NYC. She previously worked at the National Committee on U.S.-China Relations.