Jin Liqun has had a long career at the heart of China’s financial system, culminating in his appointment in 2016 as the president of the country’s first multilateral development bank, the Asian Infrastructure Investment Bank. After completing two five-year terms in that role, he is due to step down in January. Before joining the AIIB, Jin was chairman of one of China’s leading investment banks, CICC, and also had a senior role at China Investment Corp., the country’s main sovereign wealth fund — all after a two-decade long stint in China’s finance ministry, where he rose to become a vice minister. A lover of Shakespeare and opera, Jin has long been seen as one of China’s more internationally-minded financial leaders.

The following is an edited transcript of a recent interview during which Jin talked about the AIIB’s development and addressed accusations about the Chinese Communist Party’s influence over it. He also discussed the possibility that the bank could look to loan more outside Asia, and whether it would resume lending to Russia.

Illustration by Lauren Crow

Q: During your time in office, the AIIB has become one of the world’s largest multilateral banks by members. Has that growth met your expectations?

A: I have tried to work with my colleagues in the senior management team, with the support of the staff, to build a bank with a [strong] reputation. But for most of the people I hear from, whether they are bank staff or outsiders, what we have achieved over the last ten years transcends credulity — probably because expectations were set very low. Membership has grown from 57 founding members to 111 now. If the bank did not have a reputation as an apolitical, multilateral institution, we couldn’t have achieved so much. We didn’t push them to join us or induce them: they requested membership on their own.

Secondly, we have maintained our triple-A credit rating ever since the three major rating companies rated us as such for the first time, 17 months after we began operations — when the bank had no track record. Certainly, it was fully capitalized, with a top management team: It’s just like the soccer World Cup, you have all these players coming from clubs around the world. The team is a new team, but each and every player is experienced and good. They also looked at and approved of our decision making process and risk control.

When we got our triple-A rating, we still had only 30 or 40 staff. I held a reception to celebrate, but I warned the staff, this is not your PhD degree, where you earn it and it’s yours for the rest of your life: you have to earn it every year.

Being recognized by the international capital markets is the ultimate recognition for a financial institution like ours. Our most recent $2.5 billion bond issuance came in at a [very narrow] spread of just three or four pips [basis points] over the equivalent U.S. Treasury.

And in terms of your lending book, is that roughly where you expected it to be after the first decade?

Certainly, to have $66 billion worth of loans, with 345 projects covering 35 countries is something of an achievement. The credit is due to our board and management team and, of course the staff, all the way to the rank and file.

…we make decisions on the basis of consensus and collective wisdom. When you have this kind of structure, the nature of the institution is obvious. The best way you can convince the general public is through what you do, not what you say.

You manage a financial institution by making decisions on the basis of collective wisdom. I propose quite a number of ideas, but I never dictate. If my idea is not agreed upon by my senior management members, then I’m not going to push it. And sometimes the management’s ideas may not be well received by the board. We never resort to voting; we try to reach consensus. I often say, reaching consensus is not perfect. It may winnow out some good ideas. But that’s the price you have to pay.

Where do you think the AIIB now sits within the universe of global multilateral banks?

There’s been an evolution with regard to the role of MDBs. When we started to create the bank in 2014, we became aware of a very important issue. Over the last three or four decades, what set some countries apart from others is their infrastructure. The World Bank, the Asian Development Bank, and those kinds of institutions have focused on social infrastructure and poverty reduction — which is important. We needed to supplement the efforts of those institutions by focusing on infrastructure.

[Unlike the World Bank] we don’t do concessional funding [offering loans to countries at below market rates, typically to help in areas like poverty reduction], except with a limited amount of grants to support low-income countries in their efforts to improve their capacity. When we set up this bank, I was keenly aware of the importance of not competing for concessional funding. We decided to depend on non-concessional funding to promote basic infrastructure, which paves the path for sustainable, resilient growth.

If we had said this bank would be a copy of the World Bank or a clone of the ADB, that wouldn’t have been the right thing to do. It turns out that this was the right approach. We have a very good relationship with all the other development banks. We dovetail with each other’s mandates, and I’m very happy to see other institutions now also talking about infrastructure that deals with climate change.

Is the bank’s objective to make a profit, or do you judge success by other metrics?

For a financial institution, loss making definitely is not an option. But for a development bank, making money is neither the priority, nor an indicator suggesting that you are doing well.

The rational, reasonable profitability of a multilateral development institution has the advantage of helping sustain the bank in what it does, without it having to knock on the door of its shareholders, asking for money again and again. Secondly, when you are doing well, making some profit, it means the project you are financing is doing well, and so the country you support is doing well. Profit maximization is not part of our ethos. But without looking at the profitability how can you manage?

Aside from profitability, what are the key metrics by which you judge success?

We look at development impact: that’s the most important thing.

For instance, we financed a rural road in Ivory Coast, a non-Asian country, which will link the farmers in the country’s remote mountain areas with Asia. Their cashews, their coffee beans, can be shipped along the road, which has filled in the missing link with the country’s major road network and to the port at Abidjan, so that they can ship goods all the way to Asia. People who used to live in marginal lands are now part of the mainstream economy. And women there have better jobs, their livelihood is improving. So this is the development impact: We don’t look at how much money we made.

We also look at the environment and how much emissions we can reduce, and how we protect people from natural disasters such as flooding or drought. We have scorecards looking at women’s empowerment, development, environmental improvement, climate change mitigation, adaptation, all these kinds of things.

These days, there are parts of the political discourse that would describe some of that as quite ‘woke’. Where did the values of the bank that inform its operations come from?

I don’t think we should overestimate the achievements of this bank and the impact of this institution. We should remain humble. We should understand that the contribution of this bank, or any other multilateral bank, is limited, and that ultimately a country’s development depends on its government, their people and their dedication to development. We would like to give them advice, but we never want to impose any policies on them, because ultimately, development is the job of the government, the people and private sector of a particular country.

Blowing up your role as a development bank, in my view, is inappropriate. That’s why, given the same kind of support from multilateral development banks, the performance of clients varies from country to country, because the defining factors rest with the client country.

How do you allocate lending by country?

Our resource allocation has adjusted from the earliest years of the bank to now, when the bank is more or less mature. When we started to operate, we wanted to build up our lending program, to have high quality assets and to have higher loan income than our annual budget. We weren’t able to allocate resources based on so-called equitable allocation [between countries]. So early on, there was definitely concentration in terms of the countries we lent to, but there’s nothing you can do about it. Later on, you need to adjust. You need to give priority to those countries that are underserved.

So were there countries that were missing out in terms of funding from multilateral banks before the AIIB? And do you think you have filled that gap?

I don’t think that’s the right way to look at it. For instance, our bank can find it more difficult to help with some of the low income countries, because we don’t do concessional lending. Our institution sometimes takes care of more highly-rated countries so that we can generate a higher risk-adjusted return. By doing that, we can then afford to take higher risks when it comes to supporting more lowly rated countries. But I would even say it’s much more difficult for us to serve low income countries than it is for the World Bank or ADB, which can do concessional funding.

Asia cannot sustain itself without economic relations with the rest of the world, and people are becoming even clearer about the fact that Asia and the rest of the world need to work together to reverse the economic fragmentation we are experiencing today.

My job is to build up high-quality assets, by lending to those countries so that we can take higher risks to help those countries. For instance, when Sri Lanka was in deep trouble, for each and every dollar we put into Sri Lanka we had to prepare loan loss provisions. We had to have higher income countries’ assets to balance that.

Now, ten years later, it’s time for us to adjust, to make sure that we can serve more such countries better, because we can afford to do it.

You’ll be aware that when the bank was first set up, there was a lot of criticism from overseas that it was just going to be a tool of the Chinese state — which remains the AIIB’s biggest shareholder and biggest contributor of capital. Can you ever realistically expect to have a reputation of being independent from Beijing?

I think this kind of misconception or misunderstanding is inevitable. Our response is not to refute these arguments and misgivings [in words], but through what we do on the ground on a daily basis.

What is most important is the management team and decision-making process. Those two factors could convince those who are reasonable in their judgment that this bank is a neutral, apolitical, multilateral institution. I am the only Chinese national in the top management team. Our corporate secretary at first was British, then we had a German, and the next one [Sherard Cowper-Coles] will be British again. Our chief risk officer is French, the chief financial officer, who just left us, is from New Zealand. The chief internal auditor is a Singaporean lady, and chief ethics officer is a Thai lady with years of experience in Asian commercial banks.

So I am the only Chinese national, and we make decisions on the basis of consensus and collective wisdom. When you have this kind of structure, the nature of the institution is obvious. The best way you can convince the general public is through what you do, not what you say. That is why the rating companies feel comfortable, and why the capital markets are so keen to invest in our bonds.

Nevertheless, one of the big stories during your presidency was when your former communications director Bob Pickard quit and made several allegations about CCP influence within the bank. How do you respond to those accusations and the lingering fears about CCP influence?

We never overreacted. We allow the facts to speak for themselves.

So you refute his allegations?

I don’t think we should, as an institution, do something to show that we are sensitive. I don’t think it’s right to overreact. He has no evidence whatsoever to back up what he accused us of.

And so there aren’t party members within the bank’s organization?

I think we have Americans who are Republicans, and Americans who are Democrats. But we’re not involved in political activities in this institution. We do not have any countries’ party members carrying out activities in this institution.

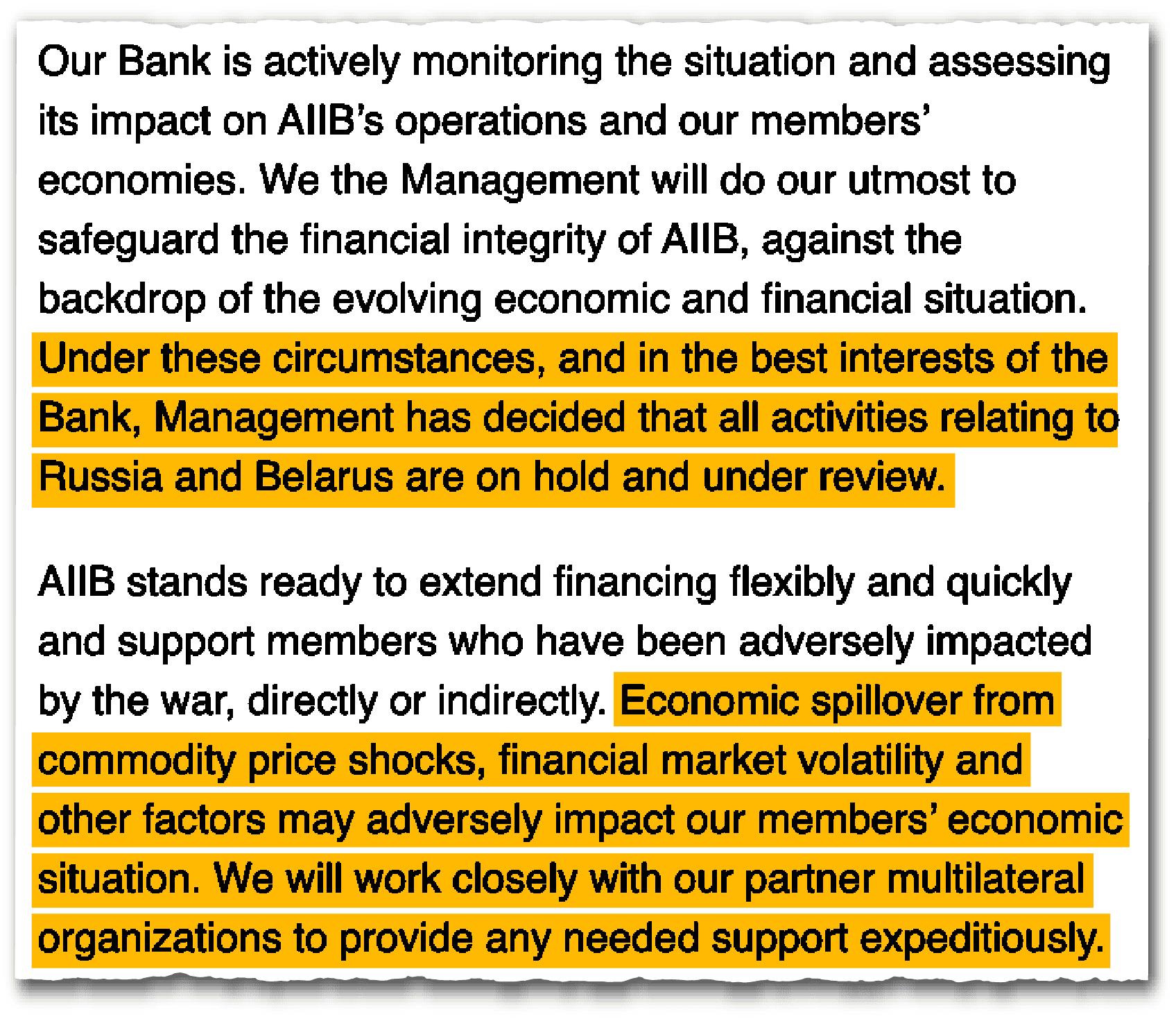

During your time, the bank stopped lending to Russia and Belarus after the invasion of Ukraine. How was that decision made, and is that a permanent state of affairs?

We make decisions on financing on the basis of economic and financial considerations. If anything happens in any of our member countries which leads to a reassessment of the country’s situation, and which would impact on the price at which we finance, it’s our fiduciary duty to make an assessment of the impact. The prudent and apolitical approach is to put on hold those projects in countries which could be questioned with regard to the effectiveness of those operations. And if, in any of these countries, the situation turns around, we can review it, and then decide when lending could be resumed. This is a normal approach for any development bank.

People ask me, how long do you think you’ll go on with the review? It stays in place for the moment.

And Ukraine itself?

Ukraine is not one of our members.

Do you have plans to spread the geographical range of countries that you lend to in the future?

The bank is inclusive. Membership is open to any country that is a member of the IMF and the World Bank. And any member is eligible for borrowing from this bank. We are different from other institutions in that we don’t have two groups of countries — members, donors, recipients.

Any country, even developed OECD countries, can borrow from us. If they choose not to borrow, it’s their decision, but policy-wise, we can lend to them. For non-Asian countries, we mainly focus on two kinds of projects. One, is those that involve connectivity with Asia. Secondly, those providing global public goods and public services. In today’s world, this is mostly climate financing.

| BIO AT A GLANCE | |

|---|---|

| AGE | 76 |

| BIRTHPLACE | Changshu, China |

| CURRENT POSITION | President, Asian Infrastructure Investment Bank |

The management and the board has worked out a program called the non-regional lending strategy, which sets a limit on our lending to non-Asian countries at 15 percent of our loans. But because of the strong demand from [non-Asian countries], we are finding that 15 percent may not be sufficient. We are currently discussing with the board how to adjust. Our strategy could certainly be adjusted, purely because of the need to respond to those countries.

So while the bank focuses on lending programs in Asia, we should not forget about non-Asian countries which are members. In terms of equity share, Asian countries account for 75 percent of the equity right now; non-Asians 25 percent.

China made it very clear from the very beginning, it was only going to borrow from the AIIB in very moderate sums, mostly for connectivity projects between China and others. China does not want to create any misconception that it created this bank to use as its ATM machine.

But what is most important is not the number, but what kind of development impact we can achieve, particularly in terms of connectivity with Asia. Asia cannot sustain itself without economic relations with the rest of the world, and people are becoming even clearer about the fact that Asia and the rest of the world need to work together to reverse the economic fragmentation we are experiencing today.

As countries like the U.S. and UK lower their aid spending, does the AIIB see an opportunity to plug the gap?

We operate on the basis of the AIIB’s principles, and we will stay the course. What we would like to do is to continue to work with other MDBs as a system. I don’t think there’s any change with regard to this sentiment.

Still, we live in a world which appears to be fracturing economically. Can multilateral banks continue to work together when they are all strongly linked to certain countries — the World Bank with the U.S., the ADB with Japan, the AIIB with China and so on?

Yes, we can still work together to promote growth, job creation, jobs for women and clean energy. We stay the course, because we have to respond to the requests of clients. This is the most important factor. Whatever changes in the geopolitical situation, we have to respond to the requests of our members, and as long as the requests are reasonable, and comply with our remit and mandate we should support them. I am not that pessimistic, frankly speaking.

To pick just one geopolitical hotspot, though, one of the biggest recipients of AIIB loans so far is India. It could get to the point one day where India and China have a major fallout. How would that affect the bank’s lending there?

You see, China is number one. India is number two. Both are developing countries. They have the right to borrow from the bank. China made it very clear from the very beginning, it was only going to borrow from the AIIB in very moderate sums, mostly for connectivity projects between China and others. China does not want to create any misconception that it created this bank to use as its ATM machine.

With regard to lending to India, we make decisions on the basis of economic and financial conditions. We should not make any kind of decisions like this because of the bilateral relationship with China, or bilateral relations with any of our members. Otherwise you deviate from the course of an apolitical institution. This is actually the litmus test [of a multilateral development bank].

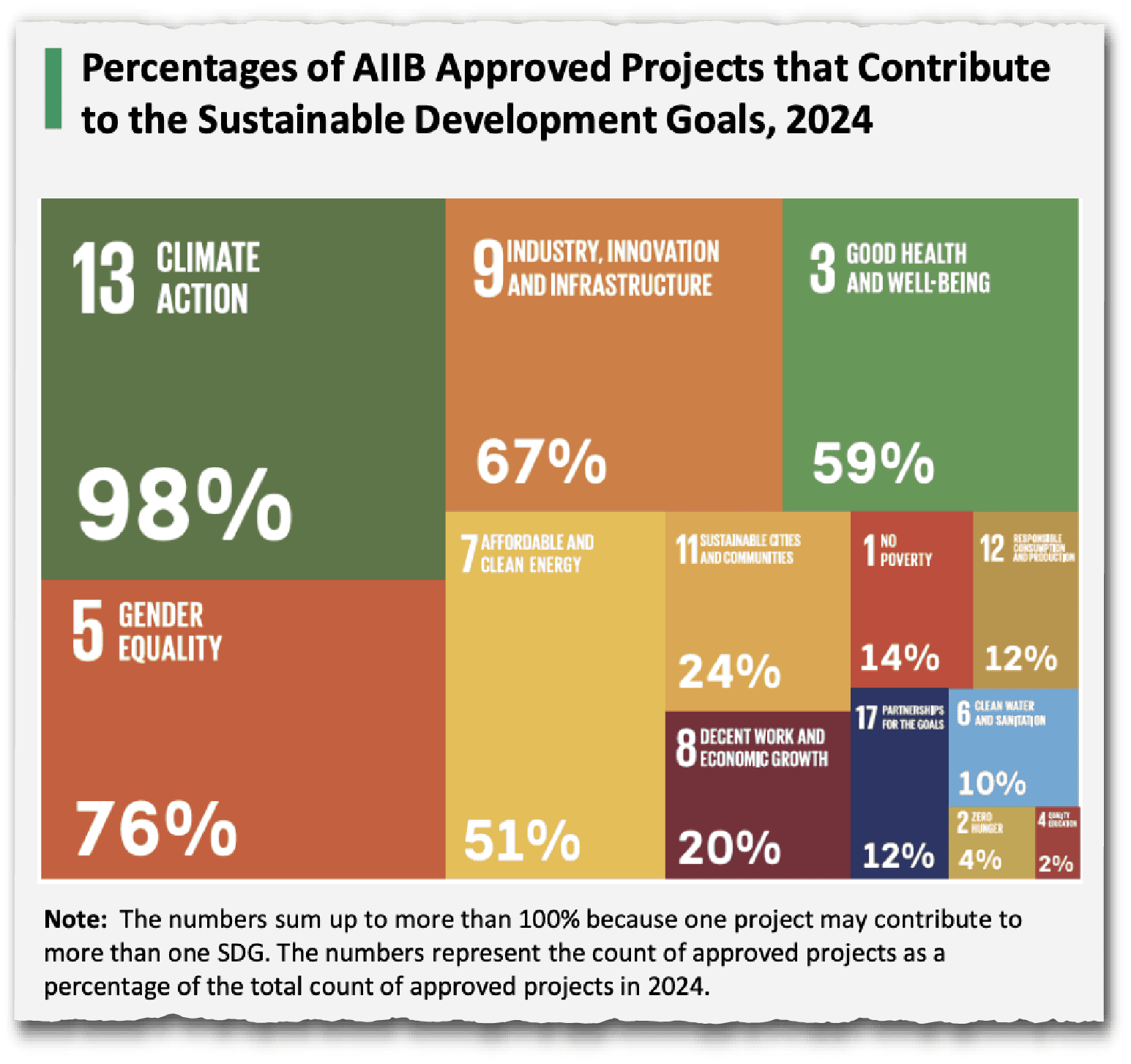

As you said, the bank has developed a reputation for leading in terms of climate finance. Why the focus on the climate impact of the lending that you do?

The bank was set up right after the Paris Agreement was entered into in October, 2015. It had so many signatories, and as the bank now has 111 members, we certainly need to take care of their concerns. And for me, to reduce emissions, to improve the environment, and not to deplete or accelerate the process of depleting natural resources is always positive.

Gas and oil will continue to be important natural resources, but if they’re not burned as fuel, they can go a long way. If we can minimize the exploitation of natural resources, we should try our very best to do that.

Looking at your portfolio, there’s a lot of lending to traditional infrastructure projects — roads, bridges, and so on. But you’ve also started lending to build data centers. Do you see that as a priority area for the bank now? And how can you square that with your environmental goals, given their high energy usage?

We define infrastructure in a liberal manner. It’s not narrowly defined as roads, railways. Digital infrastructure, social infrastructure such as health and education, are all included. We should understand that moving forward, those countries that invest in digital infrastructure could probably do better than those who are not doing the same thing.

In the future, there might be two categories of countries: AI-developed countries, and AI-developing countries. Investing in digital infrastructure in a balanced way, in my view, is important. I don’t mean we should focus most of our resources on digital — that’s not a balanced approach. Data centers are important, but we need to make sure that they are supported by reliable and clean electricity supply.

Do you see the bank as an institution that supports existing trends, or as one trying to lead in terms of where it prioritizes its lending?

We would like to be an active or even proactive player in the MDB family, doing what we can, doing what we should.

…by working within the MDB family, supporting each other is the most important thing. It’s too egotistical for us to say we want to be the leader. I am not that ambitious or arrogant. As long as we do our job properly, and we support each other, that’s great.

Early on, we talked to the World Bank: I said, we’re small, we’re new, and we want to work with you. Regardless of how much money we chip in, you are the conductor. Give me a seat in the orchestra: I will play violin or clarinet, I will just do what I’m good at, you’ll be the leader.

Later on, we started taking the lead in financing some projects. But we should understand that by working within the MDB family, supporting each other is the most important thing. It’s too egotistical for us to say we want to be the leader. I am not that ambitious or arrogant. As long as we do our job properly, and we support each other, that’s great.

The AIIB has been quite a lean organization to date, with a staff of around 800. Do you see it expanding in terms of footprint and offices around the world?

The definition of leanness is cost effectiveness. Being lean does not mean we will remain small, but there will be no redundancy. Each and every step position would have its contribution. The bank may grow to have 1,000 or 1,500 staff. That does not mean you are not lean, as long as you are effective.

We are not going to put on a lot of weight. But I fully understand that when an institution grows, it is very difficult to control. We have to be careful.

Are you worried at all about bad loans mounting up as some of the projects begun under your watch progress?

For any financial institution, non-performing loans (NPLs) are inevitable, but I think we have managed to control this. That’s why I put a lot of premium on the role of the chief risk officer. I have a saying: ‘No ‘No’ to No’, which means I will not say ‘No’ to any ‘No’ expressed by the chief risk officer. There’s one or two projects of ours which went south purely because of force majeure, like when the pandemic hit, but otherwise, we’re doing fine. I will not rule out the possibility of future NPLs, but they will be controlled.

You’re obviously a senior figure in the world of Chinese finance. What’s next for you?

Retire into my private study, and pick up the books I have not had time to read or reread. I may be invited to make a speech or something, which I would like to do. But I’m certainly not going back into a government role.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps